Introduction

Every formal import into the United States requires CBP Form 7501 — the Entry Summary. It's the document CBP uses to determine how your goods are classified, what duties you owe, and whether your shipment complies with U.S. trade regulations. Miss it, and your shipment doesn't move.

The stakes are real. Errors on Form 7501 — wrong HTS codes, understated values, misidentified countries of origin — can result in penalty assessments under 19 U.S.C. § 1592, shipment holds, or years of overpaid duties you may never recover.

This guide exists because those consequences are avoidable. It's written for importers, operations managers, and finance teams who handle or oversee import shipments but don't have deep customs expertise. You'll find plain-language explanations of every major section, a step-by-step walkthrough of the filing process, and a clear breakdown of your options when something goes wrong — including after liquidation.

Key Takeaways

- CBP Form 7501 is the official Entry Summary used to classify, value, and tax imported goods — it's the legal record of every formal import

- File electronically through ACE within 10 working days of goods being released, per 19 CFR 142

- The importer of record is legally responsible for accuracy, even when a broker prepares the form

- Key fields: entry type code, HTS classification, entered value, duty rate, MPF, and HMF

- Errors can be corrected via PSC (before liquidation) or Protest (within 180 days after liquidation); missing both windows forfeits your recovery rights

What Is CBP Form 7501?

CBP Form 7501 is the official Entry Summary document that CBP relies on to determine appraisement, classification, and origin of imported goods — and to calculate the duties, taxes, and fees the importer of record owes.

It's the formal legal record connecting a shipment to its importer, its product classification, and the exact duties paid. That record doesn't disappear after your goods clear. It persists through post-entry review, CBP audits, and compliance checks — sometimes for years.

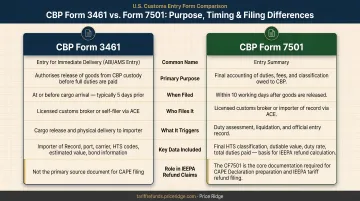

Form 7501 vs. Form 3461: Know the Difference

Importers often confuse these two forms. They serve distinct purposes at different points in the process:

| Form | Name | Purpose | Timing |

|---|---|---|---|

| CBP Form 3461 | Entry/Immediate Delivery | Releases goods from CBP custody | Filed before goods are released |

| CBP Form 7501 | Entry Summary | Declares classification, value; pays duties | Filed within 10 working days of release |

Form 3461 is the release trigger. Form 7501 is where classification and duty payment happen. Both are transmitted electronically through ACE — paper submissions are no longer part of the workflow.

Key Sections of CBP Form 7501 Explained

Every Form 7501 follows the same structure regardless of importer or shipment size. Understanding its major sections lets you review filings for accuracy rather than taking broker-prepared documents on faith.

Entry Type

The two-digit entry type code tells CBP how to process the shipment. Common codes include:

- 01 — Standard consumption entry (most imports)

- 03 — Consumption entry subject to antidumping/countervailing duties (AD/CVD)

- 06 — Foreign Trade Zone consumption entry

- 11 — Informal entry (lower-value shipments)

Selecting the wrong code affects duty rules, documentation requirements, and compliance obligations. A shipment subject to AD/CVD that's filed as a standard 01 entry creates serious compliance exposure.

Line Items and HTS Classification

Each product in a shipment appears as its own line item. Each line shows:

- HTSUS classification number

- Country of origin

- Entered value

- Quantity and units of measure

- Tariff duty rate

- Calculated duty amount

HTS misclassification is one of the most common and consequential errors on Form 7501. The classification number drives the duty rate — and the wrong code can mean years of overpaid duties or, worse, underpaid duties that trigger a CBP penalty review. In October 2024, the DOJ filed suit against an importer for allegedly misclassifying Chinese solar panels as LED lights, seeking nearly $300,000 in unpaid duties and $800,000 in civil penalties.

Duty Rate, MPF, and HMF

Three cost components to verify on every entry:

Tariff duty rate is derived from the HTS code and applied against the entered value. It varies by product, country of origin, and any applicable trade remedies.

Merchandise Processing Fee (MPF) applies to most formal entries. For FY2026, CBP's current MPF figures are:

- Rate: 0.3464% of declared value

- Minimum: $33.58 per entry

- Maximum: $651.50 per entry

Harbor Maintenance Fee (HMF) applies only to ocean shipments. Per 19 CFR 24.24, HMF is 0.125% of the value of commercial cargo loaded or unloaded from a commercial vessel. Air and truck shipments do not incur HMF.

Value Calculations

Those fees are only as accurate as the value they're calculated against. Valuation determines the monetary base for all duties and fees. CBP's primary method is transaction value — the price actually paid or payable for the goods. But the declared value isn't always just the invoice price.

Items that must be included in entered value:

- Assists (tooling, molds, materials supplied free to the manufacturer)

- Packing costs

- Royalties or license fees as a condition of sale

- Commissions paid to selling agents

- Accurate currency conversions

Omitting assists or using the wrong exchange rate are common valuation errors — and both create financial exposure in opposite directions. Undervaluation can trigger penalties; overvaluation means you're leaving duty overpayments on the table.

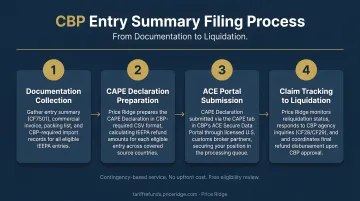

How the Entry Summary Filing Process Works

The modern entry process is entirely electronic, conducted through ACE (Automated Commercial Environment). Here's how it flows from arrival to final duty settlement.

Step 1: Entry Documentation (Form 3461)

Before goods can be released from CBP custody, entry documentation must be filed. Under 19 CFR 142, merchandise must generally be entered within 15 calendar days after landing from a vessel, aircraft, or vehicle. This step triggers release — it doesn't settle duties.

Step 2: Entry Summary Filing (Form 7501)

The entry summary and estimated duty payment must be submitted within 10 working days of the date goods are entered or released, per 19 CFR 142.12. Missing this deadline creates exposure to liquidated damages that can compound across future shipments.

Step 3: CBP Review and Liquidation

Liquidation is CBP's official closing of the entry, the point at which duties are finalized. Per 19 CFR 159.1, it's defined as the "final computation or ascertainment of duties." Under 19 U.S.C. § 1504, CBP typically liquidates entries within one year of entry date, though 19 CFR 159.12 allows extensions under specified conditions.

The liquidation date creates the legal timestamp that governs your rights for post-entry corrections and protests — so tracking it is non-negotiable.

Step 4: Post-Entry Options

Importers have two distinct windows for addressing errors:

| Option | When | Covers |

|---|---|---|

| Post Summary Correction (PSC) | Before liquidation | Corrects accepted ACE entry summary data |

| Protest (19 U.S.C. § 1514) | Within 180 days of liquidation | Challenges duty assessments, classification, appraised value |

PSC and Protest are not interchangeable — PSC corrects pre-liquidation data, while Protest challenges post-liquidation CBP decisions. Miss both windows and CBP treats the liquidated entry as final — no further amendments, no duty recovery.

Common Mistakes and Misconceptions About Form 7501

"The Broker Is Responsible"

This is wrong, and it's expensive to learn the hard way. Under 19 U.S.C. § 1484, the importer of record holds the reasonable-care obligation — not the broker. A broker or agent may transmit the filing, but the legal responsibility for accuracy and completeness stays with your company. Reviewing broker-prepared filings isn't optional. It's a compliance obligation.

Field-Level Errors That Create Financial Exposure

The three most common problem areas:

- HTS misclassification — Applying a code that under- or overstates the correct duty rate. Even honest mistakes trigger duty discrepancies and can draw CBP scrutiny

- Valuation errors — Omitting assists, using the wrong exchange rate, or excluding required cost components from entered value

- Country-of-origin mistakes — Errors here can affect eligibility for preferential duty treatment or, more seriously, trigger antidumping liability

"Liquidation Is Final"

Not always. Importers have the PSC window before liquidation and the 180-day Protest window after. The critical point is active entry monitoring, because if you're not watching your entries, you won't know when those windows open and close. Missing either deadline means leaving a recoverable amount on the table permanently.

What Your Form 7501 Data Reveals After Liquidation

A liquidated Form 7501 is more than a historical record. It's the authoritative source of exactly which tariffs were assessed and paid on each entry, including any Section 232, Section 301, or IEEPA tariffs applied at the time of import.

The IEEPA Refund Opportunity

On February 20, 2026, the Supreme Court ruled in Learning Resources, Inc. v. Trump that IEEPA does not authorize the President to impose tariffs. For importers who paid IEEPA tariffs during the 2025–2026 period, this means the duties you paid may be recoverable.

The entry summary data — entry numbers, HTS codes, duty amounts, liquidation dates — forms the evidentiary foundation for filing a refund claim through CBP.

The CAPE Declaration Process

CBP has established the CAPE (Customs Automated Processing Engine) Declaration as the current mechanism for pursuing IEEPA tariff refunds. Valid refunds are generally issued within 60–90 days after CAPE acceptance, according to CBP's IEEPA duty refunds page. CBP processes declarations in the order received — position in the queue matters.

Your Form 7501 records are the starting point. If you can identify entries where IEEPA tariffs were assessed, you can quantify the potential refund and initiate the process. For most importers, navigating that process without customs expertise is where claims stall — which is where specialist support makes the difference.

How Price Ridge Can Help

Price Ridge was built specifically for importers who know they paid IEEPA tariffs but aren't sure what to do next. The service handles the entire CAPE Declaration process end-to-end:

- Reviews your import history to identify IEEPA-eligible entries and calculate total refund amount (free, no obligation)

- Retrieves CF7501 entry summaries, duty payment records, and commercial invoices directly from your customs broker

- Prepares and submits your CAPE Declaration to CBP within days of receiving documents

- Claim tracking: monitors the claim through reliquidation and handles CBP inquiries on your behalf

- Coordinates final disbursement per the agreed fee arrangement

Price Ridge operates on a contingency basis: no upfront cost, and no fee unless your refund comes through.

For importers who prefer immediate cash over waiting on CBP processing, there's also a financing option. Price Ridge can purchase your claim outright at 75–85 cents on the dollar. The minimum claim threshold is $10,000 in IEEPA duties paid.

Start with a free eligibility review at refunds@priceridge.com. Price Ridge responds within one business day.

Frequently Asked Questions

What is CBP Form 7501 used for?

CBP Form 7501 is the official Entry Summary document that CBP uses to classify imported goods, determine their value, and calculate duties owed. It serves as the legal record of duties paid for each formal import entry and supports post-entry review and audit.

When must CBP Form 7501 be filed?

The entry summary and estimated duties must be filed within 10 working days of the date goods are entered or released from CBP custody, per 19 CFR 142.12. This is separate from the entry documentation deadline of 15 calendar days from carrier arrival.

Who fills out CBP Form 7501?

A licensed customs broker typically prepares and submits Form 7501 on behalf of the importer. However, under 19 U.S.C. § 1484, the importer of record holds legal responsibility for the form's accuracy and completeness — broker filing doesn't transfer that obligation.

How do I get CBP Form 7501?

The form is available on CBP.gov, but in practice it's transmitted electronically through ACE. Importers typically receive a copy from their broker after filing or can pull entry records directly through ACE reports.

What happens if CBP Form 7501 has an error after filing?

Errors discovered before liquidation can be corrected via a Post Summary Correction (PSC). After liquidation, you must file a formal Protest within 180 days of the liquidation date — missing both windows typically forfeits any ability to amend the entry or recover overpaid duties.