This guide covers who qualifies for a refund, which entries fall under Phase 1 of CBP's CAPE system, what the filing process looks like step by step, and the mistakes that will delay or kill your claim.

Key Takeaways

- CBP's CAPE system (launched April 20, 2026) is the official filing channel for IEEPA refunds, processed by importer — not entry-by-entry

- Phase 1 covers unliquidated entries and those liquidated within the preceding 80 days — entries outside that window are excluded

- Only the Importer of Record or their licensed customs broker can file a CAPE Declaration — not attorneys or other third parties

- ACE Portal account with ACH bank information must be in place before CBP will issue any payment

- Valid refunds are typically issued within 60–90 days of CAPE Declaration acceptance, with interest included

The Legal Basis for IEEPA Tariff Refunds

On February 20, 2026, the Supreme Court decided Learning Resources, Inc. v. Trump by a 6–3 vote. The majority — Roberts, Sotomayor, Kagan, Gorsuch, Barrett, and Jackson — held that IEEPA does not authorize the President to impose tariffs. The statutory authority to "regulate" importation does not constitute a clear delegation of tariff power, and so the tariffs Trump imposed under IEEPA on most countries were unconstitutional.

That decision set off a chain of legal and administrative steps that determine exactly how importers collect their money back.

The Court Order That Created the Refund Obligation

Following the Supreme Court's decision, the Court of International Trade issued an order on March 4, 2026 in Atmus Filtration, Inc. v. United States (Court No. 26-01259). The order directed CBP to liquidate future and unliquidated affected entries without IEEPA duties and to reliquidate non-final entries.

CBP responded by building the CAPE (Consolidated Automated Processing Engine) system, which launched in ACE on April 20, 2026, specifically to handle the volume of refund claims.

Act Promptly — This Isn't Automatic

The government filed a notice of appeal on June 2, 2026, challenging aspects of the CIT's universal refund order. That appeal creates real uncertainty about how long the refund window stays open. What importers should know right now:

- Appeals can pause or limit refunds — the process may not remain open indefinitely

- CAPE Declarations are processed in order received — your queue position is set at filing

- Waiting costs you nothing except time — but time is the one variable you can't recover

Who Qualifies: Eligibility and Entry Status Requirements

Standing to File

Only two parties can submit a CAPE Declaration:

- The Importer of Record (IOR) — the party legally responsible under 19 U.S.C. § 1484(a)(1) for making entry and paying duties, typically the owner of the goods or their designated agent

- The licensed customs broker who filed those specific entries in ACE

Attorneys, trade consultants, and other third parties cannot file on behalf of importers unless they are also the licensed broker of record for those entries. CBP enforces this requirement strictly.

Entries Covered in CAPE Phase 1

Phase 1 accepts the following entry types:

- Unliquidated entries — where CBP has not yet finalized the duty assessment

- Entries liquidated within the preceding 80 days — CBP uses this window to allow time for reliquidation within the 90-day voluntary period under 19 U.S.C. § 1501

- Entries with suspended, extended, or under-review status — these maintain their status until resolved, with refunds issued at the time of liquidation

Entries Excluded From Phase 1

CBP will not process the following in Phase 1:

- Entries flagged for reconciliation

- Entries on a drawback claim

- Entries with an open protest

- Entries subject to AD/CVD pending liquidation per DOC instructions

- Entries not filed in ACE

- Entries in final liquidation (liquidated more than 80 days ago)

- Certain entry types including TIBs and duty deferral entries

CBP has indicated these categories are being evaluated for future CAPE phases.

The "Finally Liquidated" Problem

Entries liquidated more than 80 days ago are excluded from Phase 1 and have two remaining options:

- Formal protest — filed with CBP within 180 days of the liquidation date under 19 U.S.C. § 1514(c)(3)

- Litigation — at the Court of International Trade

If your entries fall into this category, consult customs counsel promptly. The 180-day protest deadline is a hard cutoff with no exceptions.

The Step-by-Step CAPE Declaration Filing Process

Step 1 — Set Up Your ACE Portal Account

The IOR or their broker needs an established ACE Secure Data Portal account. CBP distinguishes between two application paths:

- Importer Account Application — for a new account with a single IOR number

- ACE Portal Account Application Web Form — for multiple IOR numbers, adding sub-accounts, or updating TAO data

If you have an inactive account, email ACE.Support@cbp.dhs.gov with "reactivation" in the subject line. Don't skip this step — without an active ACE account, you can't file or receive payment.

Step 2 — Enroll in ACH Refunds

CBP issues refunds via Automated Clearing House (ACH) electronic payment. Paper checks are not the standard method.

Add your U.S. bank account information through the ACH Refund Authorization tab in your ACE Importer sub-account. If ACH information is missing or incorrect when your refund is ready to issue, CBP will hold the payment indefinitely — there's no workaround.

If a third party will receive the refund on your behalf (such as a customs broker or refund service), that party must be designated on CBP Form 4811 and must also have ACE Portal and ACH enrollment in place.

Step 3 — Compile Your Entry List

Gather and verify:

- All entries on which IEEPA duties were paid (entry summaries are retrievable from CBP's ACE system)

- Current liquidation status for each entry in ACE

- Confirmation that no entries are flagged for exclusion (reconciliation, open protest, drawback, etc.)

Submitting excluded entries won't void the whole declaration, but it triggers validation delays that can push your refund timeline back by weeks. Audit this list carefully before moving to Step 4.

Step 4 — Prepare and Submit the CAPE Declaration CSV

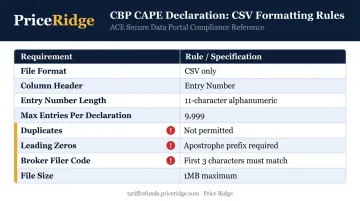

The CAPE Declaration is a CSV file. CBP's formatting rules are strict:

| Requirement | Rule |

|---|---|

| File format | CSV only |

| Column | Single "Entry Number" column with header |

| Entry number format | 11-character alphanumeric |

| Maximum entries per declaration | 9,999 |

| Duplicate entries | Not permitted |

| Leading zeros | Must use apostrophe prefix (e.g., '01234567890) |

| Broker account filer code | First three characters must match the broker's filer code |

| File size | Maximum 1MB |

Multiple declarations may be filed if you have more than 9,999 entries. Once a CAPE Declaration is accepted, it cannot be amended or cancelled. Verify every entry number and format requirement before you submit.

Step 5 — Monitor Acceptance and Track Refund Status

After submission, ACE runs two validation rounds: file-level (format and structure) and entry-level (individual entry eligibility). Invalid entries are removed while valid ones proceed. You receive a CAPE claim number upon acceptance.

Track your refund progress using these ACE reports:

- REV-603 — trade refund status

- REV-613 — ACH rejected refunds

- REV-615 — CAPE refund detail

- ES-022 — links CAPE declarations to entries and refunds

Critical timing constraint: Once a CAPE Declaration is accepted, you cannot file PSCs or protests for included entries until liquidation/reliquidation is complete. If you have open non-IEEPA PSC issues on any entry, resolve them before filing — not after.

Working With a Specialist Service

For importers without in-house customs expertise, Price Ridge manages the entire CAPE Declaration process end-to-end. Three engagement models are available:

- Contingency-based filing — no upfront cost; Price Ridge handles eligibility review, documentation retrieval, CSV preparation, ACE submission, and claim tracking through CBP reliquidation. Fee is 15–30% of the refund, disclosed before engagement. Minimum: $10,000 in IEEPA duties paid.

- Outright claim purchase — for claims of $500,000 or more, Price Ridge buys the refund claim at 75–85 cents on the dollar, with cash wired at closing. No waiting for CBP processing.

- Claim financing — Price Ridge advances 60–80% of estimated refund value against your pending CBP disbursement. You repay from the CBP payment when received and keep any excess.

Contact refunds@priceridge.com to request a free eligibility review with no obligation.

Documentation Requirements, Common Errors, and Compliance Tips

What to Gather

- Entry summaries (CF7501) pulled from ACE, confirming IEEPA duties paid, entry numbers, HTS subheadings, and country of origin

- Proof of IOR status for the relevant entries

- CBP Form 4811 to designate a third party to receive the refund

The CAPE Declaration CSV itself only requires entry numbers. CBP does not require additional documentation within the file.

Common Filing Errors

File-level errors (the entire upload fails):

- Wrong format (not CSV), empty file, or missing "Entry Number" header

- File exceeds 1MB

- More than 9,999 entries in a single declaration

- Duplicate entry numbers in the file

- Entry numbers that aren't 11 characters

- Filer code mismatch for broker accounts

Entry-level errors (specific entries are removed):

- Entry in final liquidation beyond 80 days

- Open protest on the entry

- Entry flagged for reconciliation or drawback

- No IEEPA HTS code on the entry

- Entry not found or archived in ACE

Rejected entries are removed from the declaration while valid entries proceed. You can resubmit corrected entries on a new declaration.

The Netting Risk

CAPE processing removes all IEEPA tariff codes and recalculates every duty, tax, and fee on the entry, including Section 232, Section 301, and Column 1 rates. If you underpaid non-IEEPA duties, CBP nets that amount against your IEEPA refund. In some cases, this produces a bill rather than a payment.

For instance: if you paid a combined 15% rate under a Framework Agreement and the Column 1 (MFN) rate is 5%, only the 10% IEEPA portion is refundable. Section 301 and Section 232 duties are not refundable under Learning Resources and remain in place.

Watch for CAPE-Related Scams

CBP has issued a scam alert: fraudsters are impersonating CBP via social media and email to solicit financial information from importers. Key facts:

- CBP charges no fees for processing IEEPA tariff refunds

- CBP will not email you refund updates

- Any request for financial information or fees from someone claiming to be CBP is a scam

Direct legitimate questions to CBP's official contacts: traderelations@cbp.dhs.gov and IEEPARefunds@cbp.dhs.gov.

After You File: Timelines, Interest, and What to Expect

Refund Timeline

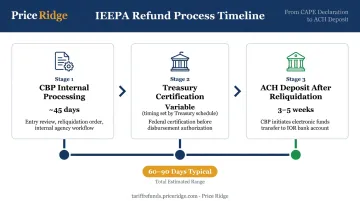

CBP's published guidance puts the typical timeline for valid IEEPA refunds at 60–90 days from CAPE Declaration acceptance. That breaks down roughly as:

- ~45 days for CBP internal processing

- Additional time for Treasury certification

- 3–5 weeks for ACH deposit after reliquidation

Entries with suspended, extended, or under-review status will not be refunded until they liquidate — that timeline is less predictable and depends on the specific hold reason.

Interest Is Included

Under 19 U.S.C. § 1505, interest runs from the date duties were deposited to the date of liquidation or reliquidation. The rate follows the IRS quarterly rate published in the Federal Register:

| Quarter | Non-Corporations | Corporations |

|---|---|---|

| Q1 2026 | 7% | 6% |

| Q2 2026 | 6% | 5% |

Interest is paid as part of the consolidated refund, not as a separate payment.

If the Refund Amount Differs From Expectations

A few things can cause the actual refund to differ from what you calculated:

- Netting of over- and under-payments across the entry (as discussed above)

- Batching by liquidation date — multiple smaller deposits for separate entry groups rather than one lump sum

- Debt offset under 19 CFR § 24.72 — any outstanding debts to CBP will be applied against the refund

If after accounting for these factors the amount still seems wrong, you can file a formal Protest after liquidation/reliquidation.

Frequently Asked Questions

Who handles tariff refunds?

CBP administers IEEPA tariff refunds through its CAPE system within the ACE Portal. Claims must be filed by the Importer of Record or their authorized licensed customs broker — not attorneys or other third parties. CBP processes and disburses refunds directly to the IOR or a designated Form 4811 party.

Can businesses file for tariff refunds?

Yes. Any business that was the Importer of Record on entries subject to IEEPA tariffs can file via the CAPE system. Entries must meet Phase 1 eligibility criteria (unliquidated, or liquidated within the preceding 80 days), and the business must have an ACE Portal account with ACH bank information on file.

What is a CAPE Declaration and how does it work?

A CAPE Declaration is a CSV file listing entry numbers for which IEEPA refunds are requested, submitted through the ACE Portal. CBP validates the entries, removes IEEPA duty codes, recalculates all other duties, and issues a consolidated refund to the IOR via ACH. Invalid entries are removed during validation without affecting the rest of the claim.

How long does it take to receive an IEEPA tariff refund?

Valid refunds are generally issued within 60–90 days of CAPE Declaration acceptance, with ACH deposits arriving 3–5 weeks after the entry liquidates or reliquidates. Entries under suspension or administrative review may take longer depending on when the underlying hold is resolved.

What happens if my entries are already finally liquidated beyond the 80-day window?

Entries in final liquidation beyond 80 days are excluded from CAPE Phase 1. Recovery options include a formal protest (within 180 days of liquidation — a hard deadline) or litigation at the Court of International Trade. Consult customs counsel promptly if your entries fall in this category.

Will I receive interest on my IEEPA tariff refund?

Yes. Interest is included in the refund payment under 19 U.S.C. § 1505, calculated from the date duties were deposited to the date of liquidation or reliquidation at the applicable IRS quarterly rate. CBP includes it in the consolidated refund payment, not as a separate line item.