The ruling is significant. But the refund process isn't automatic, the deadlines are real, and the path forward is genuinely complex for importers without customs expertise.

This article covers what IEEPA is, what the ruling actually held, which tariffs are affected versus still in force, how the refund process works, and what importers should do right now.

TL;DR: Key Takeaways

- The Supreme Court ruled 6-3 on February 20, 2026 that IEEPA does not authorize presidential tariff authority

- All IEEPA-based tariffs—"Reciprocal Tariffs" and "Trafficking and Immigration Tariffs"—were invalidated

- CBP collected approximately $133.5 billion in IEEPA tariffs through December 14, 2025, with up to $175 billion in potential refunds

- Section 232 and Section 301 tariffs are unaffected and remain in force

- Refunds are not automatic—importers must file through CBP's CAPE system, and deadlines apply

What Is IEEPA and How Was It Used to Impose Tariffs?

IEEPA (50 U.S.C. § 1701 et seq.) was enacted in 1977 to give the President broad authority to regulate economic transactions during declared national emergencies. For nearly 50 years, no President used it to impose tariffs. That changed in 2025.

The 2025 Tariff Actions

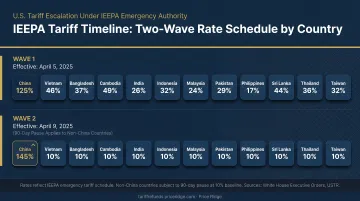

The administration issued two waves of IEEPA tariffs:

Wave 1 — Trafficking and Immigration Tariffs (February 2025):

- Canada: 25% duty on most goods, 10% on energy — citing fentanyl flow across the northern border (EO 14193)

- Mexico: 25% additional duty on imports — citing the southern border situation (EO 14194)

- China: 10% additional tariff — citing the synthetic opioid supply chain (EO 14195)

Wave 2 — Reciprocal Tariffs (April 2025, "Liberation Day"):

- 10% baseline duty on imports from virtually all trading partners, effective April 5, 2025 (EO 14257)

- Country-specific higher rates took effect April 9, 2025

- China's rate escalated to 84%, then 125%, before being suspended at 10% for 90 days (EO 14298)

The Constitutional Tension

Article I, Section 8 of the Constitution gives Congress—not the President—the power to lay and collect duties and regulate foreign commerce. Using IEEPA to impose tariffs without explicit congressional authorization was the constitutional conflict that reached the Supreme Court: whether Congress could delegate its tariff authority to the executive branch through a broad emergency powers statute.

The Supreme Court Ruling That Struck Down IEEPA Tariffs

The Decision

Learning Resources, Inc. v. Trump (No. 24-1287), consolidated with Trump v. V.O.S. Selections, Inc. (No. 25-250), was decided February 20, 2026. Chief Justice Roberts authored the controlling opinion in a 6-3 decision, joined by Justices Sotomayor, Kagan, Gorsuch, Barrett, and Jackson.

The holding was direct: "IEEPA does not authorize the President to impose tariffs."

Two Legal Rationales

1. The Major Questions Doctrine Congress does not delegate "highly consequential power" through ambiguous statutory language. The Court noted that no President in IEEPA's nearly 50-year history had ever used it to impose tariffs—direct evidence that Congress never contemplated such authority residing there.

2. Statutory Text IEEPA authorizes the President to "investigate, block, regulate, direct and compel, nullify, void, prevent, or prohibit" certain transactions. As the Court wrote on slip opinion p. 17: "When Congress grants the power to impose tariffs, it does so clearly and with careful constraints. It did neither here." Tariffs and duties simply aren't in that list.

The Dissent

Justices Kavanaugh, Thomas, and Alito argued that tariffs are "a traditional and common tool to regulate importation" and warned of the practical consequences—including a potentially enormous refund obligation running to hundreds of billions of dollars.

What the Ruling Did Not Decide

That refund concern points directly to what the ruling left open. The Court did not address:

- Whether refunds must be issued

- What mechanism CBP would use to process them

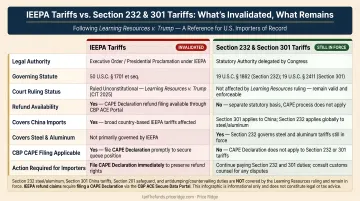

- Tariffs imposed under other statutory authorities (Section 232, Section 301, etc.)

The administration's response came the same day: President Trump signed an executive order directing agencies to end IEEPA tariff collection "as soon as practicable," while simultaneously invoking Section 122 of the Trade Act of 1974 to impose a new 10% temporary surcharge.

Which Tariffs Are Affected—and Which Ones Remain

Tariffs Invalidated by the Ruling

The February 20, 2026 White House executive order formally wound down duties imposed under the following executive orders: EO 14193, 14194, 14195, 14245, 14257, 14323, 14329, 14380, and 14382.

This covers two categories:

| Category | Rates | Imposed |

|---|---|---|

| Trafficking & Immigration Tariffs | 25% (Canada/Mexico); 10% (Canadian energy); 10%+ (China) | February 2025 |

| Reciprocal Tariffs | 10% baseline (all partners); higher country-specific rates | April 2025 |

Duties paid under these orders while they were in effect are the subject of potential refund claims.

Tariffs That Remain in Effect

Two major tariff regimes were not affected by the ruling:

- Section 232 tariffs (Trade Expansion Act of 1962) — covering steel, aluminum, copper, autos and auto parts, and semiconductors. The February 20 EO explicitly states these are untouched.

- Section 301 tariffs (Trade Act of 1974) — primarily targeting China for unfair trade practices, maintained by USTR. These statutes expressly authorize tariff adjustment following formal investigative processes, which is why they're on stronger legal footing.

"Unstacking" affects refund eligibility: Some goods subject to Section 232 tariffs had specific exemptions from IEEPA tariffs under EO 14257 and EO 14289. This directly affects which paid duties qualify for refunds—professional review before filing is recommended to avoid leaving recoverable amounts on the table.

The IEEPA Tariff Refund Landscape

The Scale of What's at Stake

Penn Wharton Budget Model economists estimate up to $175 billion in potential refunds, with approximately $133.5 billion collected through December 14, 2025 and receipts running at roughly $500 million per day under the then-active tariff schedule. Reuters later reported separate estimates suggesting refunds could total up to $182 billion. Over 26,000 importers of record are eligible. There is no clear historical parallel for a refund situation of this scale.

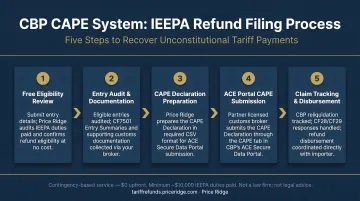

How the CBP CAPE System Works

CBP is not automatically issuing refunds. Importers must file through CAPE (Consolidated Administration and Processing of Entries)—a dedicated system within CBP's Automated Commercial Environment (ACE). Key mechanics:

- CAPE Declarations and bank information must be submitted through the ACE Secure Data Portal

- Only the importer of record or an authorized customs broker may submit

- CBP processes declarations in the order received—queue position matters

- Valid IEEPA refunds are generally issued within 60–90 days after CAPE acceptance (for Phase 1 unliquidated entries)

Critical Deadlines

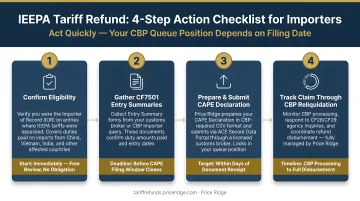

Your refund eligibility hinges on entry liquidation status:

- Unliquidated entries: File a Post Summary Correction (PSC) within 300 days of entry, and at least 15 days before scheduled liquidation

- Liquidated entries: File a protest within 180 days of liquidation under 19 U.S.C. § 1514 and 19 CFR Part 174

The U.S. Court of International Trade's December 2025 ruling in AGS Company Automotive Solutions v. United States (Slip Op. 25-154) found that importers are not required to file suit preemptively to preserve refund rights—meaning a broader universe of importers may qualify than initially feared.

Remaining Uncertainties

The refund process is not without friction. The administration has indicated it expects refunds to be contested in litigation. Treasury Secretary Bessent has stated Treasury "can easily cover" the refunds if ordered, but whether CBP will process them administratively or whether court-ordered relief will be required for some claimants remains unresolved.

Getting Help With the Process

For importers without in-house customs expertise, Price Ridge manages the entire CAPE process end-to-end. Services include:

- Eligibility review and claim assessment

- Document collection, working directly with your customs broker to retrieve CF7501 entry summaries and duty payment records

- CAPE Declaration preparation and filing with CBP

- Claim tracking through the review and reliquidation process

- Disbursement coordination once CBP issues payment

The service runs on a contingency basis with no upfront cost. For companies that need cash now, Price Ridge also offers a claim financing option—purchasing refund claims outright at 75–85¢ on the dollar for immediate payment. The free eligibility review takes one business day; minimum claim size is $10,000 in IEEPA duties paid.

What Comes Next: New Tariff Authorities and Importer Action Steps

The Administration's Tariff Pivot

Within hours of the ruling, the administration moved to alternative authorities:

- Section 122 (Trade Act of 1974): Invoked immediately via a February 20 proclamation, imposing a 10% temporary import surcharge. Hard ceiling: 15% maximum, 150-day maximum duration without congressional extension—limiting its value as a long-term replacement

- Section 301: USTR announced accelerated investigations into structural excess capacity in manufacturing sectors in March 2026

- Section 232: Additional national security tariff investigations remain ongoing

- Section 201 and Section 338: Discussed as possible tools; no official post-ruling announcements as of this writing

Importers should monitor these developments. New tariffs under different authorities could effectively replace IEEPA-era duties, and the rates and coverage may differ significantly.

Steps Importers Should Take Now

That uncertainty makes acting on existing claims more urgent, not less. Here's what to prioritize now:

- Compile entry summaries (CF7501s), duty payment records, and internal cost allocation records for all entries subject to IEEPA tariffs

- Identify which entries are unliquidated versus liquidated, and when each one crossed that threshold

- Confirm your PSC window for unliquidated entries (300 days from entry) and your protest window for liquidated entries (180 days from liquidation)

- File as early as possible — CBP processes CAPE Declarations in order received, and over 26,000 importers of record are already in the queue

Engaging help promptly matters. The CAPE filing process, protest procedures, and ACH enrollment requirements are technical work that most import teams haven't handled before. Price Ridge offers a free eligibility review with a response within one business day. Submit an inquiry at refunds@priceridge.com to get started.

Frequently Asked Questions

What does IEEPA say about tariffs?

IEEPA's text authorizes the President to "regulate, direct, compel, nullify, void, prevent or prohibit" certain transactions during a national emergency, but never explicitly mentions tariffs or duties. The Supreme Court found that omission fatal to the administration's tariff authority under the statute.

What is the current status of IEEPA tariffs?

IEEPA tariffs were struck down by the Supreme Court on February 20, 2026, and a White House executive order the same day directed agencies to end collection. The focus has shifted to how refunds will be processed and what replacement tariff authorities will take effect.

What were the IEEPA tariff rates before the ruling?

Rates ranged from 10% (baseline reciprocal) to 25% (Canada/Mexico) to significantly higher rates on Chinese goods—reaching 125% at their peak before being reduced. Those previously paid duties are now the subject of refund claims.

Are IEEPA tariffs the same as reciprocal tariffs?

The "Reciprocal Tariffs" (imposed starting April 2, 2025) were one category of IEEPA tariffs. So all reciprocal tariffs were IEEPA tariffs—but not all IEEPA tariffs were reciprocal tariffs. The earlier Canada/Mexico/China trafficking and immigration tariffs were also IEEPA-based but separate actions under different executive orders.

How do I know if I'm eligible for an IEEPA tariff refund?

Eligibility requires having paid duties on entries subject to IEEPA tariffs between early 2025 and the February 2026 wind-down, with entries either still unliquidated or within the 180-day post-liquidation protest window. Price Ridge offers a free eligibility review with a response within one business day to confirm whether a claim is worth pursuing.

What is the CBP CAPE system and how does it relate to IEEPA refunds?

CAPE (Consolidated Administration and Processing of Entries) is CBP's dedicated system within ACE for submitting and processing IEEPA duty refund requests. Filing a CAPE Declaration is the primary pathway to claim a refund. Because CBP processes declarations in queue order, earlier submission means earlier processing.