Introduction

U.S. importers paid billions of dollars in IEEPA tariffs between 2025 and 2026 — tariffs that the Supreme Court later ruled unconstitutional. On February 20, 2026, in Learning Resources, Inc. v. Trump, the Court held that IEEPA does not authorize the President to impose tariffs. CBP subsequently launched a formal refund process, and every dollar of those duties is now legally recoverable.

The problem? CBP won't automatically identify eligible companies or issue checks. Importers must file a CAPE Declaration themselves — a multi-step customs process that most companies have never encountered.

Most importers paid these tariffs and moved on. Without customs counsel on retainer or any prior experience filing reliquidation requests, many don't even know recovery is an option. That gap between legal entitlement and practical execution is where refunds go unclaimed.

This guide covers what you need to act: eligibility criteria, how the CBP CAPE Declaration process works, tactics for maximizing your recovery amount, and how to secure your position before the filing window tightens.

Key Takeaways

- IEEPA tariffs on imports from China, Canada, Mexico, and other countries were ruled unconstitutional by the Supreme Court in February 2026

- CBP's CAPE Declaration system is the official mechanism for claiming refunds — filing is not automatic

- Phase 1 claims must include at least one IEEPA HTS provision and fall within 80 days of liquidation

- CBP generally issues refunds within 60–90 days of CAPE Declaration acceptance

- Claim financing options exist at 75–85 cents on the dollar for importers who need cash now

Understanding IEEPA Tariffs and Why Refunds Are Now Available

What IEEPA Tariffs Are and Which Imports Were Affected

IEEPA tariffs were imposed by executive order under the International Emergency Economic Powers Act, beginning in early 2025. The key orders and their surcharges:

| Executive Order | Signed | Country/Scope | Surcharge |

|---|---|---|---|

| EO 14193 | Feb. 1, 2025 | Canada (most products) | 25% |

| EO 14193 | Feb. 1, 2025 | Canadian energy | 10% |

| EO 14194 | Feb. 1, 2025 | Mexico | 25% |

| EO 14195 | Feb. 1, 2025 | China (synthetic opioid) | 10% |

| EO 14257 | Apr. 2, 2025 | Multiple trading partners | 10% baseline + higher rates |

Affected product categories span electronics, industrial machinery, consumer goods, apparel, automotive parts, chemicals, construction materials, food and agriculture, and medical devices — essentially any goods imported from covered countries during the tariff period.

The Legal Basis for Refunds

Three court decisions created the path to recovery:

- V.O.S. Selections, Inc. v. United States — The U.S. Court of International Trade ruled on May 28, 2025 that the challenged IEEPA tariffs exceeded statutory authority

- V.O.S. Selections, Inc. v. Trump — The Federal Circuit affirmed on August 29, 2025

- Learning Resources, Inc. v. Trump — The Supreme Court's February 20, 2026 ruling settled the matter: IEEPA does not give the President authority to impose tariffs

EO 14389, signed February 20, 2026, formally ended the IEEPA tariff collections. CBP updated its IEEPA Duty Refunds page on June 4, 2026. The CAPE system is now actively accepting refund claims.

What "Claim Acquisition" Means Here

Claim acquisition is the formal process of asserting your legal right to recover unconstitutional tariffs already paid. CBP requires importers to file a CAPE Declaration — a structured submission documenting affected entries and duties paid. Without filing, no refund is issued.

The practical challenge for most importers is CBP's technical requirements. Filing correctly means:

- Retrieving CF7501 entry summaries and duty payment records

- Preparing a compliant CAPE Declaration for each affected entry

- Submitting through CBP's system and tracking reliquidation status

Most companies don't have that process in-house. Claim management partners handle all of it, from document collection through final disbursement.

Who Qualifies: Eligibility Requirements for IEEPA Tariff Refund Claims

Core Eligibility Criteria

The importer of record who paid IEEPA tariffs on qualifying entries is eligible. Price Ridge's minimum threshold is $10,000 in IEEPA duties paid — below that, the administrative effort doesn't justify the process.

Basic eligibility checklist:

- Imported goods subject to IEEPA tariffs between 2025–2026

- Paid duties under one or more of the IEEPA executive orders listed above

- Can obtain CBP entry summaries (Form 7501) and customs broker payment records

- Have not already filed a CAPE Declaration independently

- Entries contain at least one IEEPA Harmonized Tariff Schedule Chapter 99 provision

Liquidation Status: Why It Matters

Liquidation is CBP's finalization of an entry: the point at which duties, classification, and valuation are officially settled. Under 19 U.S.C. 1504, an entry not liquidated within one year is generally deemed liquidated at the importer's asserted rate.

CBP's CAPE Phase 1 covers two categories:

- Certain unliquidated entries — still open and eligible under Phase 1

- Entries no more than 80 days past their liquidation date — time-sensitive, file immediately

Entries beyond 80 days past liquidation fall under Phase 2, which has no announced processing timeline. Protests under 19 U.S.C. 1514 remain available within 180 days of liquidation for entries that miss the CAPE window.

Who Files and Edge Cases

The proper filer is the importer of record on the CBP entry — not the manufacturer, freight forwarder, or foreign supplier. Key considerations:

- If a customs broker filed the original entries, they can also submit the CAPE Declaration on the importer's behalf

- Business ownership changes complicate eligibility: the entity that was importer of record at time of entry matters, not current ownership

- Multiple brokers filing for the same entries create rejection risk — the NCBFAA has flagged this as an active concern

- CBP allows up to 9,999 entries per CAPE Declaration in a single .CSV upload, so large portfolios can be bundled and filed efficiently in one submission

The CBP CAPE Declaration Filing Process, Step by Step

What CAPE Is and How It Works

CAPE stands for Consolidated Administration and Processing for Entries. Declarations are submitted through the ACE Secure Data Portal via the CAPE tab, not through ABI. The filing consists of a .CSV file listing entry numbers for which IEEPA refunds are requested.

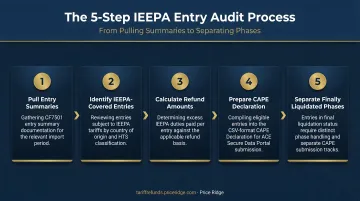

Step 1: Gather Your Documents

Required documentation for each entry:

- CBP Form 7501 (Entry Summary) — shows entry number, HTS codes, duty rates, and amounts paid

- Commercial invoice — confirms shipment value and country of origin

- Packing list — verifies quantity, weight, and shipment contents against the entry summary

- Proof of IEEPA duty payment — confirms the surcharge was actually collected

Your customs broker who filed the original entries has all of this. Contact them immediately and request a complete download of all IEEPA-duty entry records. For importers without an existing broker relationship, CBP's importer query tools can retrieve historical entry data.

Step 2: Prepare the CAPE Declaration

The declaration itself is a .CSV file listing affected entry numbers. CBP validates several things on submission:

- 11-character alphanumeric entry number format — errors here cause immediate rejection

- Importer of record matches the ACE account

- Entry exists in the CBP system

- Entry type is eligible (ineligible types include Duty Deferral/08, Reconciliation/09, Temporary Importation under Bond/23, and Drawback/47)

CBP removes the IEEPA HTS Chapter 99 provision and corresponding duty amounts from accepted entries upon processing, which triggers the refund calculation and ACH credit.

Step 3: Submit and Retain Confirmation

Declarations are submitted electronically through the ACE Portal. Retain all submission confirmation documentation — the filing date and time establish your position in CBP's processing sequence.

Step 4: Monitor and Receive Payment

Per CBP's IEEPA Duty Refunds guidance, valid refunds are generally issued within 60 to 90 days after CAPE Declaration acceptance, unless a compliance review is required. All refunds are paid via Automated Clearing House (ACH) — bank account details must be on file with CBP. Use CBP Form 4811 to designate a refund recipient or agent if needed.

Best Practices for a Successful Claim Acquisition Strategy

File as Soon as Possible

CBP has not published a formal first-come, first-served queue policy, but the processing mechanics favor earlier filers. Phase 1 entries carry hard timing constraints — the 80-day post-liquidation window closes fast. Any delay on eligible entries risks losing access to Phase 1 processing entirely and falling into Phase 2, which has no announced timeline.

With over 26,000 importers already registered as of late March 2026, the practical reality is that speed matters.

Conduct a Full Entry Audit Before Filing

Don't file a declaration before auditing everything. The goal is to identify your maximum recoverable amount — underreporting your claim means leaving money unclaimed.

Audit steps:

- Pull all entry summaries covering the 2025–2026 IEEPA tariff period

- Confirm liquidation status for each entry (check ACE weekly liquidation reports)

- Verify each entry contains at least one IEEPA Chapter 99 HTS provision

- Calculate total IEEPA surcharge paid per entry

- Separate Phase 1-eligible entries (unliquidated or within 80 days of liquidation) from Phase 2 entries

Engage Your Customs Broker Now

Your broker already has the documents you need. A single request for a complete download of all entry summaries tied to IEEPA surcharges is typically all it takes to start the audit. Most importers find their broker has everything ready — the barrier is simply knowing to ask.

Maintain a Claim Log

Create a master tracking spreadsheet with these fields per entry:

| Field | Purpose |

|---|---|

| Entry number | Identifies the specific CBP entry |

| Entry date | Confirms IEEPA tariff period coverage |

| IEEPA HTS provision | Validates eligibility |

| Duty amount paid | Establishes refund basis |

| Liquidation status/date | Confirms filing eligibility |

| CAPE Declaration submission date | Documents queue position |

| CBP acceptance confirmation | Protects against processing disputes |

This log is your protection if CBP records don't match your submission or processing errors occur.

Consider Claim Financing for Immediate Cash

For importers who can't wait 60–90 days — or longer for Phase 2 — claim financing is a legitimate option. Price Ridge purchases IEEPA refund claims outright at 75–85 cents on the dollar, delivering immediate payment instead of waiting for CBP disbursement. You receive less than the full amount, but you receive it now. For businesses absorbing tariff costs on their balance sheet, that liquidity can be worth the discount.

Common Mistakes to Avoid When Filing for a Tariff Refund

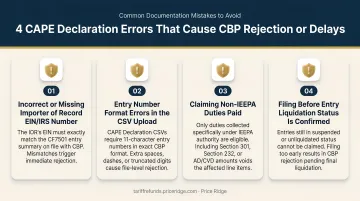

Filing on Ineligible Entry Types

CBP will reject CAPE Declarations that include Duty Deferral (08), Reconciliation (09), Temporary Importation under Bond (23), or Drawback (47) entry types. Screen entry types before building your .CSV — a single ineligible entry doesn't necessarily invalidate the full declaration, but it creates processing complications.

Documentation Errors

The most common reasons for claim delays or rejections:

- Incorrect entry number format — must be exactly 11 alphanumeric characters

- Mismatched importer of record — CBP cross-references the ACE account; any mismatch triggers rejection

- Missing IEEPA HTS provisions — entries without a qualifying Chapter 99 code don't qualify

- Empty or malformed .CSV files — CBP validates file format before processing content

Reconcile your CBP entry records against actual payment records before submission. A dollar amount discrepancy between Form 7501 and payment records will slow the review.

Waiting for More Certainty

Some importers are holding off, waiting for additional court rulings or definitive CBP guidance before filing. That delay has a direct cost: the 80-day post-liquidation window for Phase 1 entries doesn't pause while you wait.

Once eligible entries age out of Phase 1, they move to Phase 2 — which carries no timeline guarantee. The practical approach:

- File immediately on all confirmed eligible Phase 1 entries

- Track liquidation dates and queue Phase 2 entries as they become eligible

- Don't let certainty-seeking push recoverable claims past their filing window

How to Choose the Right Claim Management Partner

Most importers don't have the customs expertise to navigate CAPE Declaration filing in-house — and that's not a failure, it's just the reality. The CBP process involves ACE Portal access, .CSV formatting requirements, HTS code verification, liquidation status monitoring, and ACH disbursement setup. That's a different skill set than running an import business.

What to look for in a claim management partner:

- Specializes specifically in IEEPA tariff refunds and the CBP CAPE system — not a general customs firm that added this as a side service

- Offers end-to-end management from document retrieval through ACH disbursement

- Works on contingency (no upfront cost), which aligns the firm's incentive directly with your recovery

- Coordinates directly with your customs broker to retrieve documents, so you don't have to

- Can submit declarations within days of receiving paperwork, not weeks

Price Ridge is built around exactly these criteria. The firm handles the entire CBP process: eligibility review, document collection, CAPE Declaration filing, claim tracking, and disbursement coordination. Fees are contingency-based, vary by claim size and complexity, and are disclosed before engagement. For importers who need cash now, the claim purchase option pays out at 75–85 cents on the dollar immediately.

Contingency vs. flat fee: Contingency pricing eliminates financial risk — you only pay when CBP pays you. For small and mid-size importers uncertain about claim value, this matters. A firm charging flat fees upfront carries no financial consequence if your claim stalls or requires additional work — that cost falls entirely on you.

Price Ridge offers a free eligibility review with a response within one business day. Contact them at refunds@priceridge.com to get started.

Frequently Asked Questions

What are the five types of customs claims importers should know about?

The five main categories are duty drawback (refund when imported goods are re-exported or destroyed), protests (challenging CBP decisions on classification, valuation, or liquidation within 180 days), CAPE Declarations (IEEPA-specific refund filings via the ACE Portal), classification claims (disputing HTS code assignments), and valuation claims (disputing CBP's appraised value). For IEEPA tariff refunds specifically, CAPE Declarations are the relevant mechanism.

Who is eligible to file an IEEPA tariff refund claim?

The importer of record who paid IEEPA tariffs on qualifying entries is eligible, regardless of company size or industry. Entries must include at least one IEEPA HTS Chapter 99 provision, and the importer must have a minimum of $10,000 in IEEPA duties paid to work with a firm like Price Ridge.

How long does it take to receive an IEEPA tariff refund from CBP?

CBP states that valid refunds are generally issued within 60 to 90 days of CAPE Declaration acceptance, unless compliance review is required. Phase 2 claims (finally liquidated entries) have no published timeline. For importers who need funds sooner, claim financing at 75–85 cents on the dollar provides immediate payment.

What documents are needed to file a CBP CAPE Declaration?

The core documents are CBP Form 7501 (Entry Summary), commercial invoices, packing lists, and proof of IEEPA duty payment. Your customs broker who filed the original entries typically holds all of these and can provide them on request.

What happens if my import entries have not yet been liquidated?

Certain unliquidated entries are eligible under CAPE Phase 1 — unliquidated status doesn't automatically disqualify an entry. However, entries more than 80 days past their liquidation date fall into Phase 2, which has no announced processing timeline. Your customs broker or a claim management firm can track liquidation status on your behalf and file promptly once entries qualify.

Can I sell or assign my IEEPA tariff refund claim?

Yes. Firms like Price Ridge purchase refund claims outright, paying 75–85 cents on the dollar immediately rather than waiting for CBP processing. You receive less than the full amount, but get cash now — which may suit your cash flow needs.