This article explains what Section 232 covers, which products and sectors fall under it now, how the calculation rules changed in April and June 2026, and what importers should be doing in response.

Key Takeaways:

- Section 232 tariffs now apply to steel, aluminum, copper, autos, lumber, and thousands of derivative products

- Rates range from 10% to 50% depending on product type, metal content, and country of origin

- A critical April 2026 rule change shifted tariffs from metal-content value to full customs value — dramatically increasing costs for many importers

- Goods subject to Section 232 are excluded from IEEPA reciprocal tariffs — they are separate legal frameworks

- Active investigations covering semiconductors, pharmaceuticals, and drones signal further expansion ahead

What Is Section 232 of the Trade Expansion Act?

Section 232 is codified at 19 U.S.C. § 1862 as part of the Trade Expansion Act of 1962. It authorizes the President to impose import restrictions — including tariffs or quotas — when the Department of Commerce determines that imported goods threaten to impair U.S. national security.

How Section 232 Differs From Other Tariff Authorities

Three separate tariff authorities are commonly conflated:

- Section 232 — national security authority, Trade Expansion Act of 1962; covers specific product categories like steel, aluminum, autos

- Section 301 — unfair trade practices authority, Trade Act of 1974; administered by USTR; primarily targets China

- IEEPA — emergency economic powers authority, 50 U.S.C. § 1701; used for broader "reciprocal" tariffs in 2025 before being struck down by the Supreme Court in Learning Resources, Inc. v. Trump

One practical consequence of these distinctions: goods already subject to Section 232 duties are excluded from IEEPA reciprocal tariffs under HTSUS 9903.01.33. You don't pay both — but that also means Section 232 tariffs are not affected by the Learning Resources ruling and are not refundable through CBP's CAPE process.

That distinction matters for importers assessing their refund options. Section 232 tariffs on steel and aluminum were first imposed in March 2018, and the framework has since expanded significantly — with major product additions, country-specific rate changes, and quota restructuring continuing through 2026.

What Products Fall Under Section 232 Tariffs?

Section 232 coverage has expanded well beyond the original 2018 steel and aluminum actions. Here's where things stand:

Metals and Metal Derivatives

| Product | Current Rate | Effective Date |

|---|---|---|

| Steel articles | 50% (general) | June 4, 2025 |

| Aluminum articles | 50% (general) | June 4, 2025 |

| Copper (semi-finished + intensive derivatives) | 50% | August 1, 2025 |

| Steel/aluminum derivative products (Annex I-A) | 50% on full customs value | April 6, 2026 |

| Steel/aluminum derivative products (Annex I-B) | 25% on full customs value | April 6, 2026 |

The April 2026 proclamation extended derivative coverage to thousands of downstream manufactured goods — machinery, pipes, appliances, industrial equipment — with tariffs now calculated on the entire customs value, not just the metal content.

Autos, Trucks, and Auto Parts

A 25% tariff applies to imported automobiles (effective April 3, 2025) and covered auto parts (effective May 3, 2025). Medium and heavy-duty vehicles follow at 25%, with buses at 10% (effective November 1, 2025).

2025 U.S. auto imports totaled $208 billion, with Mexico, Japan, the EU, South Korea, and Canada supplying 96% by value. Auto parts imports reached $163.8 billion in 2024, with Mexico alone accounting for $67.4 billion.

USMCA-qualifying vehicles and parts receive preferential treatment — tariffs apply only to non-U.S. content — but CBP scrutiny on U.S. content certifications is high.

Timber, Lumber, and Furniture

- 10% on softwood timber and lumber (effective October 14, 2025)

- 25% on upholstered wooden furniture and kitchen cabinets/vanities (same effective date)

Canada supplies roughly 75% of U.S. softwood lumber imports (~$5.2 billion of the $7 billion total). Vietnam dominates wood furniture, accounting for about $4.5 billion of the approximately $11 billion in 2024 imports of upholstered wood products and cabinetry.

The National Association of Home Builders reported that lumber-related tariff price hikes added an average of $10,900 to the cost of a new home.

Products Under Active Section 232 Investigation

The following sectors face active investigations — no tariffs yet, but formal action could follow. Importers in these industries should track developments closely:

- Pharmaceuticals and pharmaceutical ingredients (investigation initiated April 2025)

- Semiconductors and semiconductor manufacturing equipment (April 2025)

- Commercial aircraft, jet engines, and parts (May 2025)

- Processed critical minerals (April 2025)

- Drones/UAS and parts (July 2025)

- Polysilicon and derivatives (July 2025)

- Wind turbines and components (August 2025)

- PPE, medical consumables, and medical devices (September 2025)

- Robotics and industrial machinery (September 2025)

Key Changes to Section 232 Tariffs in 2025 and 2026

The 2018 baseline rates are now almost unrecognizable. Here's how the structure evolved:

February–June 2025: The Rate Reset

Proclamations 10895 and 10896 (February 2025) reset aluminum from 10% to 25% and applied 25% to steel across most countries, effective March 12, 2025.

Four months later, Proclamation 10947 doubled both rates to 50%, effective June 4, 2025. The UK received preferential treatment and remained at 25%.

Copper entered the picture in July 2025 — Proclamation 10962 imposed 50% on semi-finished copper products and intensive copper derivatives, effective August 1, 2025.

August 2025: Derivative Product Expansion

The Section 232 inclusions process added 407 HTSUS codes to steel and aluminum derivative coverage, including items like lawn mowers (8433.11.00) and motorcycles (8711.30.00, 8711.50.00, 8711.60.00), effective August 18, 2025.

Note that the prior inclusions process (where importers could petition Commerce to add or remove products from derivative scope) was subsequently replaced. New coverage additions are now determined through an internal government review, with no importer petition pathway.

April 2, 2026: The Full-Value Shift (Proclamation 11021)

This is the structural change with the biggest financial impact. Before April 2026, derivative product tariffs were calculated on the value of the metal content only — so a machine worth $50,000 containing $8,000 of steel was taxed on the $8,000. Starting April 6, 2026 (the effective date), that same machine is taxed on the full $50,000 customs value, reshaping landed cost calculations across industries.

Proclamation 11021 also established the Annex I-A/I-B structure:

- Annex I-A (50%): Articles made almost entirely of covered metal

- Annex I-B (25%): Derivative articles with significant but not dominant metal content

- De minimis exclusion: Products with less than 15% metal content by weight are excluded

June 1, 2026: The Rate Relief Layer (Proclamation 11032)

Under pressure from affected industries, Proclamation 11032 introduced a temporary 15% rate (Annex I-C) for selected agriculture equipment, construction equipment, HVAC systems, and mobile industrial machinery, effective June 8, 2026 through December 31, 2027.

Additional provisions include:

- 10% rate for products manufactured using qualifying U.S.-origin steel, aluminum, or copper

- U.S.-metal threshold relaxed from 95% to 85% of relevant metal weight

- Country blended/minimum structure: For Japan, South Korea, EU, UK, Taiwan, Liechtenstein, and Switzerland, total tariff is capped at a 15% minimum (existing Column 1 duty + additional Section 232 duty)

- USMCA goods from Canada and Mexico: 25% on non-U.S. content, with a 15% minimum effective rate for qualifying goods

How Section 232 Tariffs Are Calculated Today

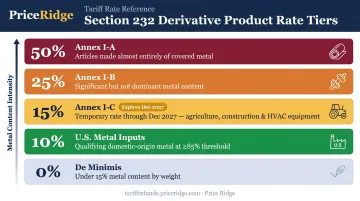

Tariff Rate Tiers

| Tier | Rate | Applies To |

|---|---|---|

| Annex I-A | 50% | Articles made almost entirely of covered metal |

| Annex I-B | 25% | Derivative articles with significant (not dominant) metal content |

| Annex I-C (temporary) | 15% | Selected agriculture, construction, HVAC, mobile industrial machinery (through Dec 31, 2027) |

| U.S. metal inputs | 10% | Products using qualifying U.S.-origin steel, aluminum, or copper (≥85% by weight) |

| De minimis | 0% | Products with less than 15% metal content by weight |

Critical stacking rule: When a product falls under more than one Section 232 action (steel, aluminum, and copper), only the highest applicable rate applies.

Country-Specific Treatment

Rates are not uniform across trading partners. The June 2026 proclamation established a blended approach for several countries:

- UK: Preferential treatment under existing agreement terms

- EU, Japan, South Korea, Taiwan, Liechtenstein, Switzerland: Total tariff (Column 1 duty + Section 232 addition) capped at a 15% minimum where existing rates fall below that threshold

- Canada and Mexico (USMCA): 25% on non-U.S. content, with 15% minimum effective rate for qualifying goods

For USMCA-origin goods, CBP scrutinizes U.S. content certifications closely. Under 19 U.S.C. § 1592, penalties for material false statements can reach the full domestic value of the merchandise in fraud cases.

Origin tracking requirements are specific:

- Steel: melt and pour country

- Aluminum: smelt and cast country

- Copper: smelt and cast country (per April 2026 proclamation)

Business Impacts: What Importers Need to Know

The Full-Value Calculation Shift

The pre-April 2026 approach allowed importers to calculate derivative product tariffs on metal-content value alone. The April 6, 2026 change to full customs value is the most significant financial shift for importers of manufactured goods.

Illustrative example:

- Industrial machine: $100,000 customs value, containing $15,000 of steel

- Pre-April 2026: 25% × $15,000 = $3,750 Section 232 tariff

- Post-April 6, 2026 (Annex I-B): 25% × $100,000 = $25,000 Section 232 tariff

That's a 567% increase in the tariff burden on the same product — without any change in the rate itself.

Sectors With Highest Exposure

- Agricultural and construction equipment — temporarily reduced to 15% under Annex I-C through December 2027, but still subject to tariffs on full customs value

- Auto parts and vehicles — 25% on full customs value; Mexico as the largest supplier at $67.4 billion is particularly exposed

- Industrial machinery — Robotics and industrial machinery face an active Section 232 investigation; existing metal-content tariff rules apply in the meantime

- Building products and lumber — NAHB estimates a $10,900 average cost increase per new home

- Pharmaceuticals, semiconductors, medical devices — Under active investigation; importers in these sectors need to monitor developments closely — proclamations can take effect with little lead time

Compliance Complexity

Origin documentation now carries direct financial consequences. Importers must:

- Track the melt and pour country for steel inputs

- Track the smelt and cast country for aluminum and copper inputs

- Correctly classify products under the Annex I-A, I-B, or I-C structure

- Document U.S.-metal content percentages if claiming the 10% preferential rate

- Verify USMCA U.S. content percentages for Canada and Mexico sourced goods

What Should Importers Do Now?

Step 1: Audit Your Product Portfolio

Check every product in your import program against the Annex I-A, I-B, and I-C lists from Proclamations 11021 and 11032. Determine:

- Which products are now subject to tariffs on full customs value

- Which rate tier applies (50%, 25%, 15%, 10%)

- Whether any products qualify for the de minimis exclusion (under 15% metal content by weight)

Your customs broker can assist with HTSUS classification and annex mapping.

Step 2: Evaluate Supply Chain Sourcing

The 10% U.S.-metal input rate (and temporary 15% Annex I-C rate) create a financial incentive to source metals domestically or to recertify existing supply chains. If your products incorporate steel, aluminum, or copper, the math has changed substantially. Run the numbers comparing:

- Current foreign-sourced metal: applicable Annex I-A or I-B rate on full customs value

- U.S.-origin metal substitution at ≥85% threshold: 10% rate on full customs value

On a $100,000 machine, that's the difference between $25,000 and $10,000 in Section 232 tariffs.

Step 3: Separate Your IEEPA Refund Opportunity

Section 232 tariffs are not refundable — they remain fully in effect and were not affected by the Supreme Court's ruling in Learning Resources v. Trump. However, many importers paid both Section 232 duties and IEEPA tariffs on the same shipments. The IEEPA portion is potentially refundable through CBP's CAPE Declaration process.

For importers who brought in goods from China, Vietnam, India, or other IEEPA-affected countries between 2025 and 2026, Price Ridge specializes in isolating and recovering the refundable IEEPA portion from mixed-duty entries, separating it line by line from non-refundable Section 232 and Section 301 amounts.

The service is contingency-based with no upfront cost. Price Ridge offers a free eligibility review with no obligation. For claims of $500,000 or more in IEEPA duties paid, an outright claim purchase at 75–85¢ on the dollar is also available for immediate cash.

Price Ridge Capital LLC is not a law firm and does not provide legal advice. CBP approval of any refund claim is not guaranteed. Consult your own counsel regarding the legal implications of tariff regulations for your specific situation.

Frequently Asked Questions

Are Section 232 tariffs still in effect?

Yes, fully. As of mid-2026, Section 232 tariffs are broader and higher than when first imposed in 2018. No court order has suspended the steel, aluminum, copper, auto, or lumber actions. The Federal Circuit upheld Section 232's constitutionality in American Institute for International Steel v. United States (2020).

What items fall under Section 232 tariffs?

Several product categories are currently covered, with more under active investigation.

Currently covered:

- Steel and aluminum (plus thousands of derivative products)

- Copper semi-finished goods and derivatives

- Automobiles, auto parts, medium and heavy-duty trucks

- Softwood lumber, upholstered wooden furniture, and kitchen cabinets

Under active investigation: semiconductors, pharmaceuticals, drones, medical devices, and robotics.

What is Section 232 of the U.S. Trade Act?

It is a provision of the Trade Expansion Act of 1962 (19 U.S.C. § 1862) that authorizes the President to restrict imports — through tariffs or other means — when the Department of Commerce finds those imports threaten to impair U.S. national security.

What is the difference between Section 232 tariffs and IEEPA tariffs?

Section 232 tariffs target specific product categories under a national security statute; IEEPA tariffs were imposed under emergency economic powers as broad "reciprocal" tariffs before the Supreme Court struck them down in Learning Resources v. Trump. Goods already subject to Section 232 duties are excluded from IEEPA tariffs — but these are entirely separate legal frameworks with separate refund implications.

Are Section 232 tariffs stacked with Section 301 or IEEPA tariffs?

Section 232 tariffs do not stack with IEEPA reciprocal tariffs, and the three Section 232 actions (steel, aluminum, copper) do not stack with each other — only the highest applicable rate applies. Section 301 tariffs on Chinese goods may apply separately, depending on the product and country of origin.

Can importers get exceptions or exclusions from Section 232 tariffs?

The old petition-based product exclusion process through Commerce has been largely eliminated and replaced with an internal government process. Limited exceptions remain for products below the 15% de minimis metal-content threshold. General exclusion requests through the previous Commerce Department process are no longer available.