The ruling is clear. The process is not. Importers who do nothing risk losing their rights permanently if deadlines pass while they wait to see how the legal battle resolves.

Here's what you need to know.

Key Takeaways

- The Supreme Court ruled 6-3 on February 20, 2026 that IEEPA-based tariffs were unconstitutional, invalidating an estimated $150 billion in collected duties.

- Only IEEPA tariffs qualify — Section 232, Section 301, and Section 122 tariffs remain in effect.

- Eligibility and deadlines hinge on liquidation status; the 180-day protest window is already running.

- The government is contesting broad refund orders; importers who don't act may get nothing.

- File a CAPE Declaration through CBP's ACE portal now to secure your place in the refund queue.

What the Supreme Court Actually Ruled

On February 20, 2026, the Supreme Court decided Learning Resources, Inc. v. Trump (No. 24-1287), consolidated with Trump v. V.O.S. Selections, Inc. (No. 25-250). Chief Justice Roberts delivered the 6-3 majority opinion, with Justices Thomas, Alito, and Kavanaugh dissenting.

The Core Holding

The ruling turned on statutory interpretation: IEEPA's authority to "regulate" importation does not grant the President power to impose sweeping, open-ended tariffs. Congress holds the constitutional authority over tariffs — and IEEPA (50 U.S.C. §§ 1701 et seq.) does not contain the explicit delegation required to override that.

In plain terms: the executive branch taxed imports under a statute that didn't authorize it.

How the Case Got to SCOTUS

The lower court path moved quickly:

- May 28, 2025 — The Court of International Trade (CIT) struck down the IEEPA tariff orders and issued a permanent injunction

- August 29, 2025 — The Federal Circuit affirmed the invalidity ruling, but vacated the universal injunction remedy and remanded for further review

- February 20, 2026 — The Supreme Court affirmed the Federal Circuit's judgment

What the Ruling Does and Doesn't Cover

Invalidated: All tariffs imposed solely under IEEPA authority.

Not affected:

- Section 232 steel and aluminum tariffs (national security authority, 19 U.S.C. § 1862)

- Section 301 China trade-practice tariffs (USTR authority, 19 U.S.C. § 2411)

- Section 122 balance-of-payments tariffs (19 U.S.C. § 2132)

The Supreme Court's opinion did not address refunds of tariffs already collected. That question was left to CBP's administrative process and subsequent court orders — which is where the practical recovery work begins for importers.

Which IEEPA Tariffs Qualify for a Refund

Only duties assessed under IEEPA executive orders qualify. Here's the complete list:

| IEEPA Tariff Program | Executive Order | Rate | Effective Date |

|---|---|---|---|

| Reciprocal tariffs (most countries) | EO 14257 | 10%+ baseline, higher country-specific rates | April 2, 2025 |

| Canada fentanyl/northern border | EO 14193 | 25% (10% on energy) | February 1, 2025 |

| Mexico fentanyl/southern border | EO 14194 | 25% | February 1, 2025 |

| China fentanyl/synthetic opioids | EO 14195 / EO 14228 | 10% rising to 20% | February 1, 2025 |

| Brazil | EO 14323 | 40% additional | July 30, 2025 |

| India | EO 14329 | 25% additional | August 6, 2025 |

Who Can File a Refund Claim

Only the Importer of Record (IOR) — the entity identified in Box 22 of the CF7501 entry summary — can file directly with CBP. If your supplier shipped DDP, a freight forwarder was listed as IOR, or a third party handled the entry, the refund right belongs to that entity, not to you as the buyer.

How to Identify Qualifying Entries

The HTS subheadings on your CF7501 are the key. One code is refundable; the rest are not:

Refundable:

- HTS 9903.01.25 and related IEEPA codes

Not refundable:

- HTS 9903.88.xx (Section 301 China tariffs)

- HTS 9903.80.xx (Section 232 steel)

- HTS 9903.85.xx (Section 232 aluminum)

This distinction matters most for China-origin entries, which frequently carry IEEPA, Section 301, and MFN duties on the same shipment. Calculating the refundable amount requires a line-by-line audit to isolate the IEEPA component. Broker summary invoices alone are frequently insufficient for this calculation.

How the Refund Process Works

CBP does not automatically process refunds. Importers must affirmatively file through CBP's CAPE (Consolidated Administration and Processing of Entries) system, launched on April 20, 2026 in the ACE Secure Data Portal.

The CAPE Declaration

A CAPE Declaration is a CSV-format file — one row per CF7501 entry summary — containing:

- Entry number and port code

- Importer of Record number

- Total entered value

- IEEPA duty amount paid

- HTS subheading and country of origin

- Entry phase (Phase 1 or Phase 2)

CBP's format requirements are strict. Wrong column order, mismatched HTS codes, incorrect date formats, or missing IOR numbers will cause CBP to reject the entire filing, sending the importer to the back of a queue that already had 26,000+ companies registered as of late March 2026.

Phase 1 vs. Phase 2: The Critical Distinction

| Phase 1 (Unliquidated) | Phase 2 (Finally Liquidated) | |

|---|---|---|

| Entry status | Not yet final | Already finalized by CBP |

| Typical entries | 2026 imports | 2025 and earlier imports |

| CBP timeline | 45–90 days after CAPE acceptance | No announced timeline |

| Mechanism | CAPE Declaration | CAPE Declaration |

Important: CBP has explicitly prohibited using Post-Summary Corrections (PSCs) to initiate IEEPA refund requests. CAPE is the required mechanism for all IEEPA duty refunds.

Protest Rights for Liquidated Entries

For entries already liquidated before you file a CAPE Declaration, an additional protection exists: file a formal protest within 180 days of the liquidation date under 19 U.S.C. § 1514. If CBP denies the protest, you have 180 additional days to file a complaint at the Court of International Trade under 28 U.S.C. § 2636. Missing either deadline forfeits the claim permanently.

Refund Timing and Interest

CBP has stated that valid IEEPA refunds are generally issued within 60–90 days after acceptance of a CAPE Declaration for Phase 1 entries. Phase 2 has no announced processing timeline. CBP also processes refunds including interest under 19 U.S.C. § 1505, meaning the longer CBP holds the money, the more it may owe.

That processing timeline doesn't work for every business. Price Ridge offers two options for importers who need flexibility:

- Claim purchase: Price Ridge buys eligible claims outright at 75–85¢ on the dollar for claims of $500,000 or more, delivering immediate cash at close

- Claim financing: A cash advance of 60–80% of estimated refund value, repaid from the CBP disbursement when it arrives

For importers who prefer full-service management at no upfront cost, Price Ridge's contingency-based filing service covers eligibility review, CAPE Declaration preparation, ACE portal submission through licensed customs broker partners, CF28/CF29 response management, and disbursement coordination. There is no charge until CBP pays. The minimum threshold is $10,000 in IEEPA duties paid.

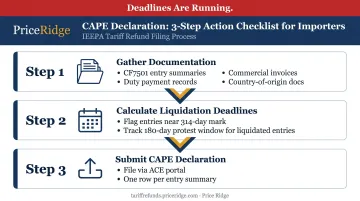

What Importers Need to Do Right Now

Step 1: Gather Documentation Immediately

Contact your customs broker to obtain:

- CF7501 entry summaries for all 2025–2026 IEEPA-period imports

- Duty payment records with line-item breakdowns

- Commercial invoices showing FOB/CIF values

- Country-of-origin documentation

Download and store copies now — don't rely on future access to broker portals or CBP's ACE system.

Step 2: Calculate Your Liquidation Deadlines

Entries typically liquidate 314 days after the entry summary is filed. For entries approaching that threshold, CBP may grant an extension — but these are discretionary, not guaranteed.

Key deadlines to track:

- Not yet liquidated: Flag entries nearing the 314-day mark for potential extension requests

- Already liquidated: The 180-day protest window starts immediately — it does not pause, and missing it forfeits the claim

Step 3: Get a Free Eligibility Review

Price Ridge offers a no-obligation eligibility review with a response within one business day. The review identifies your IEEPA-eligible entries, separates refundable IEEPA duties from non-refundable Section 301 and Section 232 tariffs, and calculates your estimated refund amount.

There's no upfront cost and no commitment to engage. Start at refunds@priceridge.com.

What the Government's Legal Battle Means for Your Refund

Following the Supreme Court ruling, CIT Judge Richard K. Eaton issued an order on March 4, 2026 concerning liquidation and refund treatment for all importers — not just the original plaintiffs. The government subsequently challenged this order, with the Justice Department arguing that the broad refund relief should not extend beyond the named litigants, per reporting by Hogan Lovells and Jackson Walker.

What This Means Practically

The outcome of the government's appeal will determine whether CBP issues refunds automatically to all importers or only to those who individually preserve their rights through the CAPE process.

Either way, waiting for the appeal to resolve is a high-risk strategy. If deadlines pass while the legal fight continues, importers who haven't filed may lose their rights permanently — regardless of how the courts ultimately rule.

The Scale of What's at Stake

According to the Congressional Budget Office, approximately $150 billion in customs duties were collected as a result of IEEPA tariffs before they were removed. Congress has not passed legislation to limit, cap, or delay refund payments — but the dollar amounts involved make that a real possibility worth watching.

What doesn't change with the legal uncertainty: CBP's CAPE queue runs first-come, first-served. Filing now locks in your position — whenever refunds process, earlier queue placement means earlier payment.

Frequently Asked Questions

What is the Supreme Court decision on tariff refunds?

In Learning Resources, Inc. v. Trump, decided February 20, 2026, the Supreme Court ruled 6-3 that the President lacked authority to impose tariffs under IEEPA. The decision invalidated those tariffs and entitles U.S. importers to seek refunds — but only through affirmative filing via CBP's CAPE system.

Which tariffs qualify for a refund?

Only tariffs imposed solely under IEEPA authority qualify — including reciprocal tariffs and the fentanyl-related tariffs on Canada, Mexico, and China. Section 232 (steel/aluminum), Section 301 (China trade practices), and Section 122 tariffs rest on separate legal authority and are not affected by this ruling.

What is the deadline to file a tariff refund claim?

For liquidated entries, you must file a protest within 180 days of the liquidation date — a firm, non-extendable deadline. For unliquidated entries, file a CAPE Declaration as soon as possible. Liquidation deadlines on 2025 entries are already running, so every week of delay narrows your window.

Can I sue the government for a tariff refund?

Yes — if CBP denies a protest, importers can file a complaint at the U.S. Court of International Trade within 180 days of denial under 28 U.S.C. § 2636. Most importers are better served by first completing the administrative CAPE process before pursuing litigation.

How long will it take to receive an IEEPA tariff refund?

Phase 1 (unliquidated) refunds are generally issued within 60–90 days of CAPE Declaration acceptance per CBP guidance; Phase 2 (finally liquidated) has no announced timeline. Importers who need funds sooner can explore claim purchase or financing options for immediate cash.

Do I need a customs broker or lawyer to file a refund claim?

You're not legally required to hire counsel, but CAPE filing requirements are technically precise — format errors reset your queue position entirely. A specialized service handles the end-to-end process, reducing rejection risk and maximizing recovery without requiring in-house expertise.

Price Ridge is not a law firm and does not provide legal or tax advice; consult your own counsel for legal questions.