Introduction

U.S. importers paid billions in IEEPA tariffs between 2025 and 2026. On February 20, 2026, the U.S. Supreme Court ended that — ruling in Learning Resources, Inc. v. Trump that IEEPA does not authorize the President to impose tariffs. Those duties are now legally refundable.

Here's the catch: refunds are not automatic. The court ruling created the legal basis for recovery, but CBP will not mail you a check because of it. Importers must file through specific procedural channels — and several of those windows are closing right now.

Reuters estimates total IEEPA refunds could reach up to $182 billion. That money doesn't distribute itself.

What follows covers the main recovery mechanisms available, how CBP's CAPE Declaration process works, and the concrete steps importers need to take now — before filing deadlines close.

Key Takeaways

- The Supreme Court struck down IEEPA tariff authority on Feb. 20, 2026 — making duties paid under IEEPA refundable

- Refunds require active filing through CBP's CAPE system; they are not issued automatically

- Act now: Phase 1 CAPE covers unliquidated entries and entries liquidated within the past 80 days, and this window is closing daily

- Section 301 (China), Section 232 (steel/aluminum), and AD/CVD duties are not affected by this ruling

- Phase 1 refunds issue within 60–90 days of CAPE Declaration acceptance

What Is Customs Duty Recovery?

Customs duty recovery is the process of identifying and reclaiming duties that were overpaid, incorrectly assessed, or are now legally refundable. That can happen for several reasons:

- Classification errors — the wrong HTS code was applied, resulting in a higher duty rate

- Valuation disputes — the declared customs value was overstated

- Trade agreement eligibility — goods qualified for preferential treatment that wasn't claimed

- Legal rulings — a tariff authority is invalidated by a court, as happened with IEEPA

One misconception derails many recovery efforts: importers assume a favorable ruling automatically generates a refund. It doesn't. CBP operates on strict procedural timelines. PSCs, protests, drawback claims, and CAPE Declarations each carry filing deadlines, and missing them permanently forfeits your recovery rights — regardless of what the courts decided.

The current IEEPA situation makes this concrete. Bloomberg reported that refunds for $166 billion in global tariffs declared unlawful have begun moving through CBP. But only importers who actively filed are receiving them.

Types of Customs Duty Recovery Available to U.S. Importers

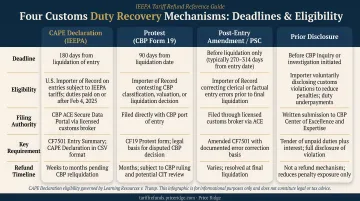

The Four Main Recovery Mechanisms

| Mechanism | When It Applies | Key Deadline |

|---|---|---|

| Post-Summary Correction (PSC) | Unliquidated entries with errors | 300 days from entry; 15 days before liquidation |

| Formal Protest | Liquidated entries within the protest window | 180 days from liquidation |

| Duty Drawback | Goods later exported, destroyed, or used in export manufacturing | Varies by claim type |

| CAPE Declaration | IEEPA-specific refunds via CBP's new system | Rolling 80-day Phase 1 window |

What the IEEPA Ruling Does NOT Cover

Ongoing legal challenges target IEEPA tariff authority specifically — not every tariff regime. These separate regimes remain fully in effect and are not recoverable through CAPE:

- Section 301 — China tariffs (Trade Act of 1974 authority)

- Section 232 — Steel and aluminum tariffs

- Antidumping and countervailing duties — Separate trade-remedy laws

Before filing anything, audit your entry universe to determine which tariff authority applies to each payment. An entry carrying Section 301 duties can look identical to one with IEEPA duties on paper — only the IEEPA duties are refundable through CAPE, so the distinction matters significantly.

Entry Status as a Sorting Tool

Your entry's liquidation status determines which recovery mechanism applies:

- Unliquidated entries → PSC or Phase 1 CAPE (fastest path)

- Liquidated within 180 days → Formal protest (if CAPE doesn't apply)

- Liquidated within 80 days with IEEPA duties → Phase 1 CAPE

- Finally liquidated → Phase 2 CAPE (no announced timeline yet)

Running this sort upfront prevents filing under the wrong mechanism — which wastes time and can forfeit your recovery window entirely.

The IEEPA Tariff Refund: A Major Recovery Opportunity Right Now

The Legal Foundation

The controlling case is Learning Resources, Inc. v. Trump (No. 24-1287), decided February 20, 2026. The Supreme Court held that IEEPA does not authorize the President to impose tariffs. Executive Order 14389, signed the same day, terminated the affected tariff actions.

CBP responded by building the Consolidated Administration and Processing of Entries (CAPE) system, launched April 20, 2026. Reuters estimates total IEEPA tariff revenue through February 19 at $168 billion, with potential refunds reaching $182 billion.

Phase 1 Eligibility: Who Qualifies Now

Phase 1 CAPE covers the most straightforward cases:

- Entry must be unliquidated or liquidated within the preceding 80 days

- Entry summary must include at least one dutiable IEEPA HTS Chapter 99 code

- Entry must not have an open protest, drawback claim, or reconciliation flag

- Entry Types 09 (reconciliation) and 47 (drawback) are excluded

The 80-day window is rolling. Every day that passes without a filing pushes more entries out of Phase 1 eligibility and into the slower, timeline-unknown Phase 2 process.

The Tax Dimension

Duty refunds come with real accounting consequences. According to KPMG's analysis and CBIZ commentary on tariff refund treatment:

- If duties were capitalized into inventory, the refund reverses into cost of goods sold

- If duties were expensed, recovery creates taxable income in the year received

- Financial statement disclosure obligations may arise while claims are pending (see Deloitte's guidance on ASC 450 gain-contingency accounting)

Loop in your CFO and tax team before refunds arrive. The IRS general recovery rule under Publication 525 applies, but no IEEPA-specific guidance has been issued — so model the book-to-tax impact now, using conservative assumptions.

Fraud Warning

CBP issued CSMS #68569567 warning that scammers are targeting importers with phishing attempts via social media, email, and phone. Three things to know:

- CBP does not charge fees to process IEEPA refunds

- CBP will not email CAPE refund status updates independently

- All legitimate CAPE filing and communications go through the ACE Secure Data Portal at accounts ending in @cbp.dhs.gov

If someone contacts you offering to "fast-track" your refund for an upfront fee, it's a scam.

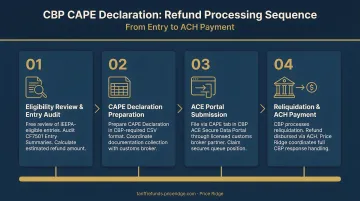

How to Recover IEEPA Customs Duties: The CAPE Declaration Process Step by Step

Step 1: Set Up Your ACE Portal Account

The Importer of Record (IOR) must have an active ACE Secure Data Portal account with an Importer sub-account. The IOR's U.S. bank account must also be enrolled for ACH refund payments in ACE. If ACH information isn't current, CBP will process the reliquidation but cannot disburse the refund.

One important constraint: only the IOR or the licensed customs broker who originally filed the entries can submit a CAPE Declaration. Attorneys can advise, but they cannot file on an importer's behalf.

Step 2: Compile Your Entry List

Pull every import entry on which IEEPA duties were paid. For Phase 1, each entry in your CSV must:

- Exist in ACE with accepted status

- Carry at least one IEEPA HTS Chapter 99 provision

- Have no open protest or drawback claim attached

- Not be Entry Type 09 or 47

- Fall within the 80-day liquidation window (or be unliquidated)

Before compiling this list, file any PSCs for non-IEEPA issues on those entries. Once a CAPE Declaration is accepted, it cannot be amended and entries cannot be removed.

Step 3: File the CAPE Declaration

Submit the CSV through the ACE Portal CAPE tab. Each Declaration supports up to 9,999 entries; you can file multiple Declarations to cover larger entry universes.

Once validated, CBP issues a CAPE claim number confirming acceptance. That timestamp matters — CBP processes declarations in the order received. Early filing means an earlier position in the queue.

Step 4: CBP Processes and Issues the Refund

After acceptance, CBP:

- Removes the IEEPA HTS Chapter 99 provisions from each entry

- Reliquidates the entry without IEEPA duties

- Issues a consolidated refund (inclusive of interest) via ACH to the IOR or designated 4811 notify party

- Nets any outstanding CBP debts before disbursing

Valid Phase 1 refunds issue 60–90 days after CAPE Declaration acceptance. Track your claim status using ACE Reports REV-603 (Trade Refund Report) and REV-615 (CAPE tracking).

Working With a Specialist

Most importers hit a practical barrier somewhere in this process — no ACE Portal access, unfamiliarity with CAPE filing requirements, or simply no bandwidth to manage a CBP claim on top of daily operations. That's where a specialist steps in.

Price Ridge handles the full process for importers without in-house customs resources:

- Retrieves CF7501 entry summaries, duty payment records, and commercial invoices from your broker

- Prepares and files the CAPE Declaration on your behalf

- Tracks the claim through reliquidation and coordinates disbursement

Claims are typically submitted within days of receiving documents, which directly protects your queue position. The eligibility review is free, and the engagement runs on contingency — no fee until CBP pays.

Best Practices to Maximize Your Customs Duty Recovery

Audit Your Entry Universe Before Filing

Map every entry by two dimensions before touching the CAPE system:

- Status — unliquidated, within protest window, finally liquidated

- Tariff authority — IEEPA, Section 301, Section 232, AD/CVD

This prevents wasted effort on ineligible entries and keeps you using the right recovery mechanism for each dollar. CBP's validation rules are strict — entries that fail checks get rejected without refund, and since accepted Declarations can't be amended, errors made before submission can't be fixed afterward.

Align Customs, Tax, and Finance Teams Early

Customs duty recovery isn't a compliance-only event. Before refunds arrive, your team needs to address:

- Income recognition — which tax year does the recovery land in?

- COGS adjustment — do capitalized duties need to unwind?

- ASC 450 may require financial statement disclosure of pending claims

- Transfer pricing — if duties were allocated across entities, refunds need to flow back correctly

Getting customs, tax, and finance on the same page before filing eliminates accounting surprises when CBP pays.

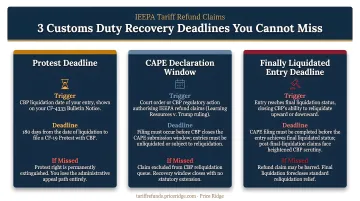

Act on Deadlines — They Are Not Flexible

| Deadline | Trigger | What Happens If Missed |

|---|---|---|

| PSC window | 300 days from entry / 15 days pre-liquidation | Entry liquidates as filed |

| Protest window | 180 days from liquidation | Entry becomes finally liquidated |

| Phase 1 CAPE | 80-day rolling window from liquidation | Entry moves to Phase 2 (no timeline) |

None of these deadlines extend because the underlying tariff was ruled unconstitutional. Missing any one of them forfeits recovery rights permanently.

Deadline pressure is also why some importers can't afford to wait on CBP processing — which is where financing comes in.

Consider Claim Financing for Immediate Cash

For importers who cannot wait 60–90 days for CBP to process their refund, Price Ridge offers a claim financing option — purchasing refund claims outright at 75–85 cents on the dollar with immediate payment, no waiting period required. Smaller importers and businesses with cash flow pressure who paid significant IEEPA tariffs can access working capital now instead of waiting on the government's timeline.

Frequently Asked Questions

How do I claim my customs duty back?

For IEEPA tariffs, you must file a CAPE Declaration through CBP's ACE Portal — either directly as the Importer of Record or through the licensed customs broker who originally filed your entries. Refunds are not automatic; your ACH bank information must be on file in ACE before CBP can disburse payment.

Who has to pay customs duty?

The Importer of Record (IOR) — the party listed on the entry summary at the time of importation — is legally responsible for paying customs duties, regardless of whether those costs were passed on to customers. This is why IEEPA refunds flow back to the IOR, not to downstream buyers or end consumers.

What is the CAPE Declaration and who can file it?

CAPE is CBP's ACE-based system for processing IEEPA duty refund requests, launched April 20, 2026. Only the Importer of Record or the original licensed customs broker can file — attorneys and other third parties are not authorized.

How long does it take to receive an IEEPA tariff refund from CBP?

For valid Phase 1 CAPE claims, CBP generally issues refunds within 60–90 days of accepting the Declaration. Entries that are suspended, flagged for reconciliation, or fall into Phase 2 territory will take longer, as CBP has not announced a Phase 2 processing timeline.

What is the difference between IEEPA duty recovery and duty drawback?

IEEPA recovery refunds unconstitutional tariffs through CBP's CAPE system, regardless of whether the goods were exported. Duty drawback is a separate program refunding up to 99% of duties on goods later exported or destroyed — it has different eligibility rules, a different process, and CAPE specifically excludes entries already covered by a drawback claim.