The Importer of Record (IOR) and the consignee are two legally distinct roles in U.S. trade. Confusing them creates real consequences: shipment holds, penalties directed at the wrong party, and lost eligibility to recover overpaid duties. According to CBP Trade Statistics, CBP collected $26.21 million from trade penalties and liquidated damages in FY 2024 alone. That number reflects enforcement actions aimed squarely at the party of record — not the party that received the goods.

This guide explains both roles clearly, when they overlap, and why getting the designation right before goods move is one of the most consequential decisions in any import transaction.

Key Takeaways

- The Importer of Record is legally accountable to CBP for customs compliance, duty payment, and recordkeeping (regardless of who physically receives the goods)

- The consignee takes physical custody after clearance; being named on a bill of lading doesn't create compliance liability

- The same party can serve both roles, but this requires an explicit designation, not a default assumption

- Misidentifying the IOR can trigger audits, hold shipments, and directly disqualify valid duty refund claims

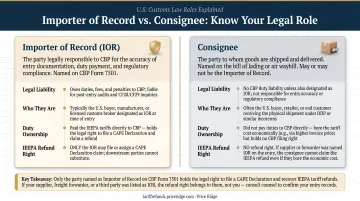

IOR vs Consignee: Quick Comparison

The two roles divide legal accountability from physical delivery. Here's how they compare:

| Category | Importer of Record | Consignee |

|---|---|---|

| Legal liability | Full accountability to CBP for classification, valuation, origin, and recordkeeping | No inherent customs compliance obligation |

| Duty payment | Pays all applicable duties, taxes, and tariffs at entry | Not responsible for duties unless also designated IOR |

| Documentation | Files customs entry documents, declarations, permits | Does not file customs documents |

| Physical receipt | Not required — IOR is a legal designation, not a physical one | Takes physical custody of goods after clearance |

| When role begins | At customs entry filing, through the post-entry audit period | After customs clearance, at point of delivery |

What Is an Importer of Record?

Under 19 CFR 101.1, the importer is defined as the party primarily liable for payment of duties — or their authorized agent. In practice, the IOR is the entity officially on record with U.S. Customs and Border Protection (CBP) for every aspect of a customs entry.

What the IOR Is Responsible For

The IOR's obligations extend well beyond paying duties at the border:

- Accurate HS code classification for every line item on the entry

- Declared country of origin, which determines tariff treatment and trade remedy applicability

- Commercial invoice valuation, which CBP scrutinizes for undervaluation

- Obtaining required import permits or licenses for regulated goods

- Recordkeeping — 19 CFR 163.4 requires records to be retained for five years from the date of entry

The IOR does not have to own the goods or receive them to carry this liability. What matters is who is named on the entry.

Who Can Serve as IOR

- A U.S. company with an EIN registered via CBP Form 5106

- A U.S. individual with a Social Security number

- A non-resident importer (NRI) — though under 19 CFR 141.18, a nonresident corporation must have a resident agent in the state where the port of entry is located, authorized to accept service of process

When CBP finds misclassification, undervaluation, or origin fraud, enforcement actions under 19 U.S.C. 1592 go to the IOR — not the consignee, not the goods owner.

IOR Status and IEEPA Refund Eligibility

IOR designation has financial consequences beyond customs clearance. For the CBP CAPE Declaration process — the mechanism for recovering unconstitutional IEEPA tariff overcharges — only the IOR (or their authorized customs broker) who originally filed the entries may submit refund claims. If you paid IEEPA tariffs as the IOR on those entries, that standing is what makes you eligible to recover them. Price Ridge handles the full CAPE Declaration filing process — document collection, CBP submission, and claim tracking — for importers who qualify.

Common IOR Use Cases

Third-party IOR services are typically used when:

- A foreign company ships into the U.S. with no domestic legal entity

- A supplier ships DDP (Delivered Duty Paid), taking on import responsibility as part of the transaction terms

- A business is entering a new market without established customs infrastructure

The Amazon FBA situation illustrates this clearly. A brand ships inventory from overseas to an Amazon fulfillment center — Amazon is the consignee. But Amazon's Seller Central policy is explicit: Amazon will not serve as IOR. The brand, or a designated third-party IOR service, must be registered with CBP and named on the entry.

What Is a Consignee?

Under UCC 7-102(a)(3), a consignee is the party named in a bill of lading to whom delivery is promised. That definition is narrower than most people assume — it describes physical receipt, nothing more.

CBP's own Directive No. 3530-002A draws a sharper line. A nominal consignee — a party with no ownership interest in the goods beyond what a shipping document conveys — cannot make entry on its own behalf. Being named on a waybill doesn't transfer compliance responsibility.

What the Consignee Actually Does

- Verifies the shipment is complete and undamaged upon receipt

- Coordinates cargo release with the carrier

- Arranges storage or onward distribution

- Resolves post-delivery discrepancies with suppliers

What the Consignee Does NOT Do

- File customs entry documents

- Pay duties (unless also designated as IOR)

- Respond to CBP audits or enforcement actions

- Manage compliance obligations of any kind

Consignee Use Cases

Two scenarios show how the consignee role plays out in practice:

- DDP shipments: When a supplier ships Delivered Duty Paid, they (or their IOR service) handle all customs obligations. The buyer is listed only as the consignee — goods arrive already cleared, with zero compliance obligation on the receiving end.

- Dual-role situations: A U.S. business that imports goods and receives them at its own facility commonly serves as both IOR and consignee. This is practical and legitimate, but it should be documented explicitly rather than assumed.

Common consignees include 3PLs, distribution centers, warehouse operators, retail chain receiving facilities, and end-buyers.

Why Getting This Distinction Right Actually Matters

When CBP enforces a compliance issue, it doesn't contact whoever received the goods — it contacts whoever filed the entry. Legal liability attaches to the IOR from the moment the customs entry process begins. The consignee's role starts only after clearance.

Consider this scenario: a warehouse receives a shipment that CBP flags during a post-entry review. The warehouse — the consignee — faces no audit liability. CBP's enforcement notice goes to the IOR. If the IOR designation on that entry was incorrect or ambiguous, every downstream enforcement step becomes harder to resolve.

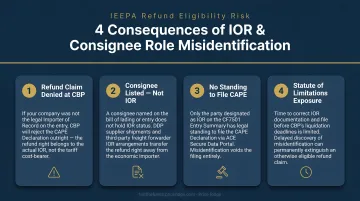

How Role Confusion Creates Operational Problems

- Shipments held at customs when CBP cannot identify a legally responsible party on the entry

- Refund claims rejected because the filing party wasn't the IOR of record — under CAPE, CBP specifically requires the original IOR to submit the declaration

- Audit exposure when the consignee is incorrectly listed as IOR across multiple inconsistent entries

- Corrections are not simple — CBP's Post Summary Correction process does not allow changes to the Importer of Record; corrections require submission of CBP Form 3347

The "Owner of Goods" Is a Third, Separate Concept

Ownership — determined by Incoterms and title transfer agreements — is legally distinct from both IOR status and consignee status. The three roles can land on three different companies in the same shipment:

- A party can own the goods without being the IOR

- A party can be the IOR without owning the goods

- Incoterms establish title transfer; CBP records establish compliance accountability — and these don't automatically align

How to Decide Which Role Applies to Your Shipment

Ask these questions before goods move:

- Are you registered with CBP as the importer? If you've filed CBP Form 5106, you have an importer number and can be designated IOR.

- Are you filing the entry (or hiring a broker to file in your name)? If yes, you are the IOR — even if you later reimburse someone else for the duties.

- Are you paying the duties? Whoever bears primary liability for duty payment is, by definition, the importer of record.

When to Designate Yourself as IOR

- You have a U.S. legal entity registered with CBP

- You're familiar with the goods' classification and trade compliance obligations

- You want full control over the import record and refund eligibility

When to Use a Third-Party IOR Service

- You have no U.S. legal presence

- You're shipping into a new market without customs infrastructure

- You lack in-house compliance expertise to manage entry accuracy and recordkeeping

Document the IOR designation explicitly before the shipment moves. For IEEPA refund purposes, your standing as the original IOR on those entries determines your eligibility to recover overpaid tariffs. Retroactive corrections to customs entries are limited, so getting this right upfront matters.

If you paid IEEPA tariffs as the IOR, you may be eligible for a refund. Price Ridge offers a free eligibility review with no obligation and a response within one business day. Contact refunds@priceridge.com to get started.

Conclusion

The Importer of Record carries legal accountability to CBP from customs entry through the post-entry audit window. The consignee carries physical responsibility for the goods after clearance. These aren't interchangeable — they're separate legal designations with separate consequences.

Getting the designation right determines:

- Who responds to CBP audits and post-entry inquiries

- Who faces penalties for classification or valuation errors

- Who holds the legal right to file for duty refunds

The right IOR depends on your business structure, trade expertise, and the specific terms of each shipment. Document that designation — before goods move — and you preserve both your compliance standing and your refund rights.

Frequently Asked Questions

Can a consignee be the importer of record?

Yes, but it must be an explicit designation — not an assumption. When a consignee is also registered as the IOR with CBP, they take on full customs compliance liability, including duty payment, recordkeeping, and audit response.

Who should be the importer of record?

The IOR should be the party with a U.S. legal presence, a customs broker relationship, and the ability to maintain records and respond to CBP inquiries. Companies without a domestic entity or customs infrastructure should use a licensed third-party IOR service.

What happens if the importer of record is misidentified on customs documents?

CBP may hold the shipment until a responsible party is confirmed. The IOR cannot be changed via Post Summary Correction — it requires CBP Form 3347. Misidentification also increases audit risk and can void duty refund claims if the filing party lacks standing.

Does the consignee have to pay import duties?

No — the consignee is not automatically responsible for duties. Only the IOR is. If the consignee and IOR are the same entity, that party carries both the compliance obligation and the duty payment.

Can a foreign company serve as importer of record in the United States?

Yes. Under 19 CFR 141.18, a nonresident corporation must have a resident agent in the port state authorized to accept service of process. Most non-resident importers work through a licensed customs broker to satisfy this requirement.

Is the importer of record the same as the owner of the goods?

No. The IOR is the party legally on record with CBP for the customs entry. The goods owner is determined by Incoterms and title transfer agreements. A party can be IOR without owning the goods, and can own goods without being designated as IOR.