This scenario played out tens of thousands of times after April 5, 2025. The confusion is real, it's widespread, and it's expensive.

This guide explains exactly what 9903.01.25 is, which products are excluded from it, how to claim those exclusions correctly in ACE, and how to recover duties you've already paid. One important caveat: reciprocal tariff rules have changed rapidly since April 2025 through multiple executive orders. Filing deadlines and refund windows are time-sensitive, so the sooner you act, the more options you have.

Key Takeaways

- 9903.01.25 is the 10% baseline reciprocal tariff code under Executive Order 14257, effective April 5, 2025

- It stacks on top of existing duties — it does not replace them

- 9903.01.32 excludes specific tech and semiconductor products; eligibility is not automatic — you must declare it in ACE

- Overpaid duties can be recovered via Post Summary Correction (PSC) or formal protest, with strict deadlines

- Price Ridge manages the full CBP CAPE refund process on a contingency basis, with no upfront cost

What Is HTS 9903.01.25? The 10% Baseline Reciprocal Tariff Explained

Executive Order 14257, published at 90 Fed. Reg. 15041 on April 7, 2025, imposed a 10% additional ad valorem duty on virtually all imported goods entered for consumption on or after 12:01 a.m. EDT on April 5, 2025. HTS code 9903.01.25 is the Chapter 99 secondary classification that carries this duty.

How the Secondary Classification Requirement Works

Every affected entry summary filed in ACE must include at least one Chapter 99 code alongside the standard Chapter 1–97 commodity classification. Missing this secondary code creates compliance errors that CBP will reject.

The correct filing sequence in ACE is mandatory:

- Chapter 98 provisions (if applicable)

- Chapter 99 duty codes in this sub-order: Section 301 → IEEPA Fentanyl → IEEPA Reciprocal → Section 232/201 → MTB/quota

- Chapter 1–97 commodity classification

Filing in any other order triggers ACE rejections.

Key Characteristics of 9903.01.25

- Additive, not replacement: The 10% stacks on top of all existing duties, fees, taxes, and charges already applicable — per CBP CSMS #64649265

- Country-specific codes replaced it for most: Effective April 9, 2025, codes 9903.01.43 through 9903.01.76 introduced higher country-specific rates for 83 trading partners under EO 14257 Annex III. For those countries and goods, the country-specific code applies instead of 9903.01.25

- 9903.01.25 still applies to goods from countries not covered by a country-specific code and to certain in-transit shipments

Taken together, these distinctions matter more than they might appear. Just because 9903.01.25 was assessed on your shipment does not mean it was applied correctly. Multiple product categories and country-of-origin situations trigger exceptions — and overpayments can be recovered through a CBP CAPE Declaration filing once identified.

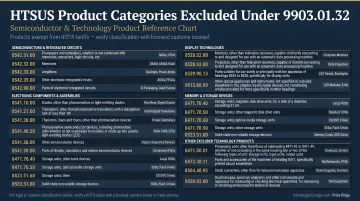

Which Products Are Excluded from 9903.01.25? Understanding 9903.01.32

The single most important exclusion code for technology importers is 9903.01.32. It was established through Section 3(b)(iv) of EO 14257 and clarified by the April 11, 2025 Presidential Memorandum, with CBP operational guidance issued via CSMS #64724565.

Which HTSUS Headings Qualify

The following HTSUS provisions were covered in the original exclusion list per CBP CSMS #64724565:

| Category | HTSUS Headings |

|---|---|

| Computers & parts | 8471, 8473.30 |

| Semiconductor manufacturing equipment | 8486 |

| Communication equipment | 8517.13.00, 8517.62.00 |

| Storage media | 8523.51.00, 8524 |

| Monitors | 8528.52.00 |

| Semiconductors, diodes, transistors | 8541.10.00, 8541.21.00, 8541.29.00, 8541.30.00, 8541.49.10, 8541.49.70, 8541.49.80, 8541.49.95, 8541.51.00, 8541.59.00, 8541.90.00 |

| Integrated circuits | 8542 |

A September 2025 executive order (FR Doc. 2025-17507) updated the scope of 9903.01.32. Cross-reference CBP's IEEPA FAQ page and the current HTSUS to confirm your product's eligibility under the updated list.

Two Critical Points About Claiming 9903.01.32

Even if your product clearly falls under one of these headings, eligibility is not automatic — you must actively declare 9903.01.32 as a secondary classification on the entry. If your product qualified but wasn't declared that way, CBP may have applied 9903.01.25 to those entries, meaning a refund claim could be warranted.

Country of origin doesn't disqualify you either. Goods from China, the EU, or any other country that classify under the listed HTSUS headings still qualify for the 9903.01.32 exclusion. China-origin goods may still face separate Section 301 duties, but that doesn't affect 9903.01.32 eligibility on its own.

Other Exceptions That Can Override 9903.01.25

Beyond 9903.01.32, several other codes and scenarios can eliminate or reduce your 9903.01.25 liability.

Key Exception Codes

| Code | What It Covers |

|---|---|

| 9903.01.26 | Articles the product of Canada (USMCA) |

| 9903.01.27 | Articles the product of Mexico (USMCA) |

| 9903.01.28 | Goods loaded onto vessels and in transit before 12:01 a.m. EDT April 5, 2025 |

| 9903.01.33 | Goods already subject to Section 232 tariffs (steel, aluminum, passenger vehicles, light trucks, auto parts) |

| 9903.01.34 | Goods with at least 20% U.S.-origin content — only the non-U.S. portion is dutiable |

Chapter 98 and De Minimis Considerations

Chapter 98 provisions are exempt from 9903.01.25, with four exceptions where the duty applies to the value of foreign work:

- 9802.00.40, 9802.00.50, 9802.00.60 — repair and alteration goods

- 9802.00.80 — goods assembled abroad using U.S. components

De minimis treatment has changed significantly. Duty-free treatment under 19 U.S.C. 1321(a)(2)(C) was suspended for all countries effective August 29, 2025 (FR Doc. 2025-14897). China and Hong Kong de minimis was separately eliminated by Executive Order 14256, effective May 2, 2025. Verify current de minimis status with CBP before assuming low-value shipments are exempt.

How to Claim Your Exclusion — or Recover Tariffs You Already Paid

Claiming the Exclusion on New Entries

For entries going forward, the process is straightforward if you follow it precisely:

- Classify your goods under the appropriate Chapter 1–97 heading

- Add 9903.01.32 as the secondary Chapter 99 classification if your product falls within the excluded headings

- Follow the mandatory ACE sequence: Chapter 98 (if applicable) → Chapter 99 codes in sub-order → Chapter 1–97

- Associate duty amounts to the correct HTSUS within each entry summary line — do not combine duties across multiple codes

For goods claiming the 9903.01.34 U.S.-content exception (20%+ domestic value), split the entry into two lines:

- Line 1: U.S. content value with code 9903.01.34, full quantity

- Line 2: Non-U.S. content value with 9903.01.25 (or country-specific code), zero quantity

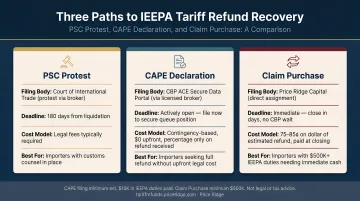

Recovering Tariffs Already Paid on Eligible Entries

If 9903.01.25 was applied to goods that should have been classified under 9903.01.32, you can still recover those duties — but the mechanism depends on where your entry stands in the liquidation process.

Post Summary Correction (PSC) — for unliquidated entries:

- Must be filed within 300 days of the entry date or 15 days before scheduled liquidation, whichever comes first

- This is the faster, lower-friction path

Formal Protest — for liquidated entries:

- Must be filed within 180 days of the liquidation date

- Once this window closes, recovery becomes nearly impossible without legal intervention

CBP CAPE System — for IEEPA duty refunds:

- CBP built the CAPE (Consolidated Administration and Processing of Entries) system within ACE specifically to process IEEPA refund claims

- CBP generally issues valid refunds within 60–90 days of accepting a CAPE Declaration

- Disbursement requires ACH (Automated Clearinghouse) enrollment

Where Price Ridge Fits In

Each recovery path above comes with tight deadlines, specific filing sequences, and CBP correspondence that can trip up even experienced operations teams. For companies without in-house customs expertise, a missed deadline or an incorrectly prepared declaration can forfeit a legitimate refund claim entirely.

Price Ridge specializes in managing the entire CAPE process on behalf of importers — from free eligibility review through final disbursement — on a contingency basis with no upfront cost.

Price Ridge collects CF7501 entry summaries, duty payment records, and commercial invoices (coordinating directly with your customs broker if needed), prepares the CAPE Declaration, and files it within days of receiving your documents to secure your position in CBP's processing queue.

For importers who need cash now rather than waiting for CBP processing, Price Ridge also offers an outright claim purchase at 75–85¢ on the dollar — immediate payment with no waiting. Minimum claim threshold is $10,000 in IEEPA duties paid. Contact them at refunds@priceridge.com to start a free eligibility review.

Key Filing Rules and Deadlines You Cannot Miss

Three filing rules consistently catch importers off guard — and each one carries real compliance consequences:

1. The 10-day correction window

Per CBP CSMS #64724565, for entries on or after April 5, 2025 where 9903.01.32 was not declared but should have been, filers must correct entries within 10 days of cargo release from CBP custody. Check current CSMS messages for updated correction guidance.

2. What actually controls the tariff date

The applicable tariff is determined by when goods are entered for consumption or withdrawn from warehouse — not the ship date, not the order date. Under 19 CFR 141.68, entry timing is based on release authorization or presentation of the entry summary in proper form.

For Immediate Delivery entries specifically, the entry summary is due within 10 working days of release under 19 CFR 142.23.

3. ACE sequence errors

CBP rejects entries filed in the wrong Chapter 99 sequence. This is not a minor formatting issue — it creates compliance failures that require corrections and can affect the tariff date recorded for the entry.

Frequently Asked Questions

What happens if I use the wrong HTS code?

Using the wrong code means you may overpay or underpay duties. Underpaying can trigger CBP penalties for lack of reasonable care. Corrections require a PSC (for unliquidated entries) or a formal protest (for liquidated entries), each with strict filing deadlines that cannot be extended once missed.

What is the code 9903.01.33?

It's the exception code for goods already subject to Section 232 tariffs — specifically articles of iron or steel, aluminum, derivative articles, passenger vehicles, light trucks, and related parts. These goods are excluded from 9903.01.25 because Section 232 duties already apply to them.

Is 9903.01.25 still in effect?

The code remains the baseline 10% reciprocal tariff, but for most countries with assigned country-specific codes (9903.01.43–9903.01.76), those rates replaced 9903.01.25 effective April 9, 2025. Check CBP's CSMS messages for current status and any subsequent modifications.

How do I know if my products are excluded under 9903.01.32?

Match your Chapter 1–97 classification against the official HTSUS headings listed in Annex II (as updated by the September 2025 executive order). Given the scope change, confirm eligibility against current CBP guidance or consult a trade professional before filing.

Can I still get a refund if my entry has already liquidated?

Yes — a formal protest can be filed within 180 days of the liquidation date. After that window closes, recovery is rarely possible, so prompt action is essential if you believe duties were incorrectly assessed.

What is the CAPE Declaration system?

CAPE (Consolidated Administration and Processing of Entries) is CBP's dedicated ACE module for processing IEEPA tariff refund requests. It requires ACH enrollment for disbursement, and CBP generally issues valid refunds within 60–90 days. Filing instructions are available on CBP's IEEPA Duty Refunds page.