Introduction

Businesses and individuals often hold legal claims that represent real money — insurance disputes, court judgments, bankruptcy distributions, government refunds — but collecting takes time. Sometimes months. Often years. Meanwhile, cash flow doesn't wait.

This creates a genuine problem: you have an asset with measurable value, but it's locked up in a process you don't control.

A claims purchase agreement solves that problem. It lets a claimant convert an uncertain future payment into immediate cash by selling the right to collect to a buyer willing to wait.

This guide covers:

- What a claims purchase agreement is and how it works

- How it differs from a standard purchase agreement

- Key components every agreement should include

- The step-by-step process from evaluation to closing

- Legal issues to watch for before signing

- A practical application for U.S. importers holding IEEPA tariff refund claims

Key Takeaways

- A claims purchase agreement lets a claimant sell their right to collect money — at a discount — for immediate cash

- Sellers get cash now; buyers take on collection risk and chase the full value

- Key components: claim identification, purchase price, seller warranties, assignment mechanics, and recourse terms

- These agreements appear in bankruptcy, insurance, litigation, and government refund contexts

- U.S. importers with IEEPA tariff refund claims can sell those claims now instead of waiting on CBP

What Is a Claims Purchase Agreement?

A claims purchase agreement is a legally binding contract in which a claimant assigns their right to collect on a legal claim to a purchaser, in exchange for a discounted percentage of the claim's face value.

The "asset" being sold isn't physical. It's an intangible legal right: an entitlement to receive money from a debtor, insurer, or government agency. The seller trades a future, uncertain payout for immediate cash. The buyer takes on the collection risk and timeline in exchange for acquiring the claim below face value.

Where These Agreements Appear

Claims purchase agreements are used across several distinct contexts:

- Bankruptcy creditor claims — unsecured creditors sell their right to receive distributions from a bankrupt estate; pricing ranges from roughly 13 cents to over 90 cents on the dollar depending on claim quality and estate solvency

- Insurance receivables — structured settlement payment rights are commonly transferred in a secondary market; NASP data indicates these transactions typically complete at discount rates between 9% and 18%

- Viatical and life settlements — life insurance policies sold by terminally ill policyholders; the NAIC Viatical Settlements Model Regulation sets minimum payouts of 60%–80% of face value based on life expectancy

- Government overpayment and refund claims — documented, quantifiable receivables against agencies like CBP, where the face value is established by payment records

The discount applied to any claim reflects three factors: the strength of the underlying legal right, how long collection will realistically take, and the probability that the obligor pays in full. A near-certain claim against a solvent debtor commands a narrow discount; a contested claim against an insolvent one can trade at a fraction of face value.

Claims Purchase Agreement vs. Standard Purchase Agreement

A standard purchase agreement transfers ownership of something tangible — real estate, goods, a business — at a price both parties know at closing. Value changes hands with certainty.

A claims purchase agreement works differently: what transfers is an intangible legal right whose full value hasn't been collected yet. That pending collection is the defining element of the deal, not a background condition.

The Risk Allocation Difference

With a standard agreement, risk transfers with the asset — but the asset's value is already known. A claims purchase agreement flips that dynamic: risk and uncertainty are the transaction. The buyer prices future collection risk into the purchase price; the seller accepts a discount to exit that risk immediately.

This also affects the governing law framework. Standard goods transactions fall under UCC Article 2. The sale of payment rights — accounts, payment intangibles, promissory notes — falls under UCC Article 9, which has specific rules about when anti-assignment restrictions are effective and when they aren't.

Recourse vs. Non-Recourse

The recourse structure determines what happens if the claim pays less than expected — or nothing at all:

- Non-recourse: The buyer absorbs the full loss if the claim is disallowed, reduced, or uncollectable. The seller walks away with the purchase price regardless

- Recourse: The seller retains some liability — typically if their representations about the claim turn out to be false, or if collection falls short

Most sellers strongly prefer non-recourse structures. Selling a claim is itself an exit from risk — a recourse clause partially reverses that exit by keeping the seller on the hook.

Key Elements of a Claims Purchase Agreement

Claim Identification

The agreement must precisely identify what's being sold: the legal basis of the claim, whether it's been filed, who the obligor is (debtor, insurer, government agency), its current procedural status, and the face value. Vague identification creates disputes about what was actually transferred.

Purchase Price and Payment Terms

This section specifies:

- The lump-sum payment amount, usually expressed as a percentage of face value

- The payment date and mechanics

- Any holdback, escrow, or post-closing adjustment provisions if the claim's value is later revised upward or downward

Per Lowenstein's bankruptcy claims primer, purchase price in claim assignments is typically individually negotiated and kept confidential.

Seller Representations and Warranties

This is the most heavily negotiated section. Standard representations include:

- The seller owns the claim outright and has authority to sell it

- The claim has not been previously assigned or encumbered

- The claim is valid, enforceable, and not subject to offset or reduction

- All material facts about the claim have been disclosed

SEC-filed claim transfer forms confirm this standard language, requiring sellers to warrant the claim is "valid, liquidated, non-contingent, free of transfer restrictions." Misrepresentation here is the most common source of post-closing disputes. It can void the agreement outright or expose the seller to damages, even in a deal structured as non-recourse.

Assignment and Transfer Provisions

The formal transfer mechanism includes:

- A written assignment executed at closing

- Notice to the obligor that the claim has changed hands (required under UCC 9-406: an obligor can discharge by paying the original claimant until it receives authenticated assignment notice)

- Any required consents from courts or agencies

In bankruptcy, the transferee files evidence of transfer with the court; the transferor has 21 days to object before substitution is complete.

Recourse Terms and Indemnification

The agreement must define what happens if the seller's warranties are breached. Even in a non-recourse deal, sellers typically remain on the hook for indemnification when their representations about validity or ownership prove inaccurate. Buyers should confirm the indemnification clause explicitly covers these scenarios — not just outright fraud — before closing.

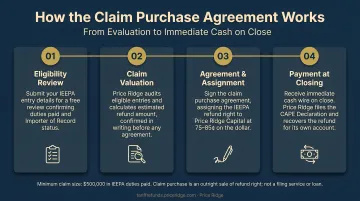

How a Claims Purchase Agreement Works

Step 1: Claim Evaluation and Pricing The buyer reviews all documentation — court filings, agency correspondence, original agreements — assessing the claim's legal merit, the obligor's solvency, collection timeline, and probability of full recovery. That analysis determines the purchase price offer.

Step 2: Agreement Drafting and Negotiation With pricing established, parties negotiate purchase price, warranty scope, recourse structure, and post-closing obligations. Sellers should scrutinize warranty provisions carefully — that language is where post-closing liability concentrates.

Step 3: Execution and Assignment Once terms are agreed, both parties sign the claims purchase agreement and the accompanying assignment document. Depending on claim type, formal notice goes to the obligor. Some transfers require court approval or agency consent before they become effective.

Step 4: Payment and Post-Closing The buyer pays the agreed purchase price. Under a non-recourse structure, the seller's involvement ends at that point. The buyer pursues collection independently and bears full responsibility for timing and outcome.

Non-recourse vs. recourse: In a non-recourse deal, the seller takes no further risk if the claim fails to collect. In a recourse deal, the seller may owe a refund or indemnity if recovery falls short. Which structure applies depends on negotiated warranty terms in Step 2.

Legal Considerations and Enforceability

Assignability

Not every claim can be transferred. The Restatement (Second) of Contracts § 317 allows assignment of contractual rights unless it materially changes the obligor's burden, is forbidden by statute, violates public policy, or is validly precluded by contract.

Common non-assignable categories include:

- Personal injury tort claims — courts generally treat these as personal to the claimant

- ERISA welfare benefit plan rights — anti-assignment clauses are enforceable in nearly all federal circuits

- Contractual restrictions — courts have enforced anti-assignment clauses; in one Delaware bankruptcy case (Woodbridge), an anti-assignment clause was enforced and the purported claim transfer was held null and void

Always confirm assignability before entering any agreement. If a claim turns out to be non-assignable, the buyer may have no recourse — and no valid claim to enforce.

What Can Void the Agreement

Several triggers can unwind or impair a completed claims purchase:

- Seller misrepresentation — false warranties about claim validity or ownership

- Prior undisclosed assignment — seller already transferred the claim to someone else

- Lack of authority — seller didn't have legal power to sell (e.g., claim belonged to an estate or entity)

- Failure to obtain required consents — court approvals or obligor consents not secured

- Underlying claim unenforceable — claim is successfully objected to, disallowed, equitably subordinated, or subject to offsetting defenses

Governing Law and Dispute Resolution

The agreement should specify which state's law governs. Choice of governing law affects how anti-assignment restrictions are interpreted and how warranty claims are adjudicated.

Arbitration clauses are common for speed and confidentiality. Under the Federal Arbitration Act § 2, written arbitration provisions in commercial contracts are generally enforceable in both federal and state courts. Key dispute resolution provisions to address include:

- Choice of governing state law

- Arbitration vs. litigation election

- Venue and jurisdiction for any court proceedings

- Attorneys' fees and cost allocation

Claims Purchase Agreements for IEEPA Tariff Refunds

U.S. importers who paid tariffs imposed under IEEPA authority now hold documented refund claims against CBP. After the Supreme Court invalidated the IEEPA tariffs and the Court of International Trade ordered administrative refunds, CBP launched the CAPE system to process refund declarations. Reuters reported the system launched as thousands of companies filed claims, with an estimated $166 billion in potential refunds at stake.

That scale makes these unusually clean claims for purchase purposes: face value is established by customs entry records, the obligor is the U.S. government, and CBP has an official processing mechanism. A secondary market for outright purchases of IEEPA refund claims is active and growing.

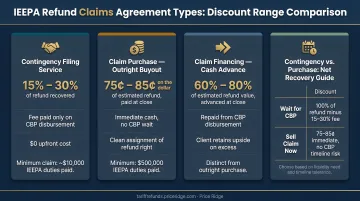

The practical trade-off:

- File through CAPE and wait — CBP targets 60–90 days for Phase 1 claims after declaration acceptance, with no published timeline for Phase 2 claims

- Sell the claim now — receive immediate cash at a discount, with no waiting and no CBP process to manage

Price Ridge offers importers both paths. The contingency-based filing service manages the entire CAPE Declaration process at no upfront cost, taking a percentage only when CBP pays. The claim purchase option buys IEEPA refund claims outright at 75–85 cents on the dollar.

For importers who need working capital now or want to exit the process cleanly, it converts a government receivable into immediate cash. Importers with at least $10,000 in IEEPA duties paid can request a free eligibility review at refunds@priceridge.com.

Frequently Asked Questions

What is a purchase claim?

A purchase claim is a legal right to receive money or assets from a third party — such as a refund, insurance payout, or court judgment — that has a defined or estimated value. In many cases, that right can be assigned or sold to another party through a claims purchase agreement.

How is a claims purchase agreement different from a regular purchase agreement?

A regular purchase agreement transfers a tangible asset at a known value. A claims purchase agreement transfers an intangible legal right whose full value is still pending collection — making risk allocation and assignability the central legal concerns, not just price and delivery.

Do I need a lawyer to write a purchase agreement?

For claims purchase agreements specifically, you should have a lawyer review the agreement. The representations and warranties section carries real post-closing liability, and assignment mechanics vary by claim type. Templates don't account for these deal-specific risks, especially for high-value claims.

What can void a purchase agreement?

Common grounds include:

- Seller misrepresentation about the claim's status or ownership

- Prior undisclosed encumbrances on the claim

- Lack of legal authority to sell or absent required consents

- The underlying claim being non-assignable or successfully challenged after transfer

Can you sell a claim before it's fully resolved?

Yes — selling before resolution is common. The buyer acquires whatever is ultimately recovered, and the purchase price is set at a discount to reflect that uncertainty. The seller trades an unpredictable future payout for immediate, certain cash.