The stakes are higher now than they've been in decades. Since 2025, IEEPA-based tariffs have added significant duty burdens across dozens of countries of origin. Many importers paid those tariffs faithfully — only to discover they may have a legal right to recover them.

This guide covers everything you need to know: the formal IOR definition, the IOR number requirement, full compliance obligations, who qualifies, how Incoterms assign the role, and what IORs can do if they overpaid.

Key Takeaways

- The IOR is the legally responsible party for customs compliance, documentation, and duty payment on every US import

- Must be a registered entity with a valid EIN, SSN, or CBP-assigned importer ID number

- Core obligations cover tariff classification, entry filings, duty payment, partner agency compliance, and five years of recordkeeping

- Buyer, seller, or a designated third party can serve as IOR — Incoterms determine who takes on that role

- IORs who paid IEEPA tariffs may be eligible to recover those payments through a CBP CAPE Declaration claim

What Is an Importer of Record?

The Importer of Record is the individual, business, or designated representative that takes legal ownership of a shipment during the customs clearance process and assumes full responsibility for compliance with all US import laws enforced by CBP.

The IOR Number

Every customs entry requires an importer number. Per CBP guidance:

- US businesses use their IRS Employer Identification Number (EIN)

- Individuals may use their Social Security Number

- Foreign entities without an EIN or SSN can obtain a CBP-assigned importer ID via Form 5106

That number appears on CBP Form 7501 (Entry Summary), the document CBP uses to determine classification, valuation, and origin. Having your number on that form means CBP can pursue you directly for unpaid duties, penalties, or regulatory violations, up to four years after the shipment clears.

Reasonable Care — The Legal Standard

That legal exposure exists because of what's on the line. Under 19 USC §1484, the IOR is held to a "reasonable care" standard — covering accurate classification, correct valuation, and all information CBP needs to assess duties and determine admissibility.

What this means in practice: "I didn't know" is not a defense. If your customs broker misclassified an HTS code and you didn't verify it, the legal and financial consequences still fall on you as the IOR.

IOR vs. Cargo Owner

One common misconception: the IOR doesn't have to own the goods. A licensed customs broker, for example, can be designated as IOR in specific contractual arrangements — temporarily assuming legal liability during clearance. The key rule: regardless of cargo ownership, the IOR always bears the compliance and financial responsibility.

Key Responsibilities of the Importer of Record

The IOR carries legal accountability for every aspect of a compliant import — from the moment goods are classified to years after they clear customs. These five responsibilities define that obligation in practice.

HTS Classification and Valuation

The IOR must assign the correct Harmonized Tariff Schedule (HTS) code to every imported product. Wrong classifications create two problems:

- Underpayment — CBP can audit entries retroactively and assess additional duties plus interest

- Overpayment — the IOR may be entitled to a refund, but only if they file the appropriate claim within the protest window

Filing Accurate Import Documents

The IOR (or their customs broker acting on their behalf) is responsible for accuracy across all entry documentation:

- CBP Form 7501 (Entry Summary) — the primary record for classification, valuation, and origin

- Commercial Invoice — must meet 19 CFR 141.86 requirements, including detailed merchandise description, purchase price, currency, and country of origin

- Packing List — itemizes contents for CBP review

- ISF (10+2) — governed by 19 CFR Part 149; must be filed at least 24 hours before vessel loading. Inaccurate, incomplete, or late filings carry $5,000 in liquidated damages per violation

Payment of Duties, Taxes, and Tariffs

The IOR is directly liable for all applicable charges at entry, including:

- Standard MFN duties

- Section 301 tariffs (China)

- Section 232 tariffs (steel and aluminum)

- IEEPA-based tariffs (2025 executive orders)

- Antidumping and countervailing duties (ADD/CVD)

Payment obligations follow the liquidation timeline set under 19 USC §1504.

PGA Compliance

For regulated goods, customs clearance alone isn't enough. The IOR must also satisfy requirements from relevant Participating Government Agencies:

- FDA — food, pharmaceuticals, and medical devices

- EPA — vehicles, engines, and emissions-regulated products

- FCC — radio frequency devices under 47 CFR 2.1204

- USDA APHIS — agricultural products and natural resources

FDA-regulated shipments face an additional risk: detention without examination, which can delay clearance even when the customs entry is complete. PGA holds from any agency can block release entirely.

Recordkeeping and CBP Inquiries

Under 19 CFR Part 163, the IOR must retain all import-related records — entry documents, invoices, payment records, correspondence — for five years from entry.

CBP can audit those records at any time, through two main channels:

- CBP Form 28 (Request for Information) — requires a timely, complete response

- CBP Form 29 (Notice of Action) — notifies the IOR of proposed or completed CBP action; inadequate responses can result in additional duty assessments, liquidated damages, or entry rejection

Who Can Act as an Importer of Record?

Not everyone qualifies. The IOR must be the owner, purchaser, or a licensed customs broker designated by the owner, purchaser, or consignee — as defined in 19 USC §1484.

Eligibility requirements:

- US businesses: valid EIN

- Individuals: SSN

- Foreign entities: CBP-assigned importer ID obtained via Form 5106

- A customs bond is also required for commercial shipments (governed by 19 CFR Part 113), serving as CBP's financial guarantee that duties and penalties will be paid

Can a Foreign Company Be the US IOR?

Yes, but it requires extra steps. A foreign entity without a US presence must:

- File CBP Form 5106 to obtain an importer ID

- Designate a licensed US customs broker to manage filings and bond requirements

This arrangement is common in DDP transactions but carries real risk for the foreign seller, who assumes full US customs liability without a domestic legal infrastructure behind them.

What Customs Brokers Can and Cannot Do as IOR

That foreign-seller liability often falls to a customs broker — which raises an important distinction about what brokers will and won't take on.

A licensed customs broker can act as IOR when explicitly designated under 19 USC §1484. In practice, most choose not to:

- Customs brokers: Can legally serve as IOR but rarely do, since accepting the designation transfers full customs liability to them

- Freight forwarders: Typically avoid the IOR role entirely — they have no financial interest in the cargo and no appetite for the regulatory exposure

- NVOCCs: Same logic applies; coordinating transport is their function, not absorbing import liability

IOR vs. Other Roles in the Supply Chain

| Role | What They Do | Bears IOR Liability? |

|---|---|---|

| Importer of Record | Files entry, pays duties, ensures compliance | Yes — always |

| Consignee | Receives the goods | Only if also acting as IOR |

| Customs Broker | Prepares and files entry docs as agent | Only if explicitly designated as IOR |

| Exporter of Record (EOR) | Handles export-side compliance in origin country | No — separate legal role |

The IOR/EOR distinction matters in cross-border transactions: the EOR manages export control compliance under U.S. Export Administration Regulations on the origin side, while the IOR handles import compliance on the destination side. One company can hold both roles simultaneously — which means carrying both sets of compliance exposure.

The most common confusion is between the IOR and the customs broker. The broker prepares and files documentation on the IOR's behalf — but unless they've been contracted to serve as IOR, the legal and financial liability stays with the importer. Misunderstanding this distinction is a frequent source of customs penalties — and one that brokers themselves often don't volunteer to clarify.

How Incoterms Determine Who Is the Importer of Record

Incoterms 2020 define when risk and cost transfer between seller and buyer — and that transfer point determines who takes on the IOR role. One critical caveat: Incoterms don't override customs law. Whoever becomes the IOR still faces full CBP obligations regardless of what the commercial contract says.

Incoterm IOR Assignment at a Glance

| Incoterm | Typical US IOR |

|---|---|

| DDP (Delivered Duty Paid) | Seller |

| DAP (Delivered At Place) | Buyer |

| DPU (Delivered at Place Unloaded) | Buyer |

| EXW, FCA, FOB, CFR, CIF, CPT, CIP | Buyer |

Either party can designate a third-party agent (such as a licensed customs broker) to fulfill the IOR role — the Incoterm determines the default, not the final arrangement.

The DDP Risk for Foreign Sellers

DDP looks straightforward on paper: the seller handles everything, the buyer just receives the goods. In practice, a foreign seller using DDP takes on significant US compliance exposure, including:

- Obtaining a US importer ID

- Securing a customs bond

- Establishing a licensed broker relationship

- Meeting full CBP and PGA requirements

One misclassification or missed PGA requirement falls entirely on the seller. For foreign sellers shipping DDP to the US regularly, a third-party IOR service or experienced customs broker is the practical way to stay compliant without turning a sale into a liability.

The IOR's Tariff Obligations — and What Happens If You Overpaid

Your Tariff Liability as IOR

Paying all applicable tariffs is a core, non-negotiable obligation. The IOR is personally liable for every duty assessed at entry, including:

- Standard MFN duties

- Section 301 (China) and Section 232 (steel/aluminum) tariffs

- IEEPA-based tariffs imposed by executive order starting in 2025 on imports from Canada, Mexico, China, and dozens of other countries

The IEEPA Tariff Situation

The International Emergency Economic Powers Act (IEEPA) was invoked in 2025 to impose broad tariffs across multiple countries of origin. If you imported goods from affected countries during 2025–2026 and paid those tariffs, you're the party of record — and the party with legal standing to seek a refund.

Legal challenges to the IEEPA tariffs created a potential recovery pathway. The Federal Circuit addressed the legality of these tariffs in V.O.S. Selections, Inc. v. Trump, and CBP subsequently launched the CAPE Declaration system to process IEEPA duty refunds without requiring entry-by-entry protests.

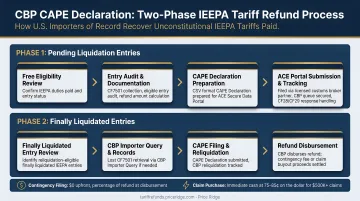

The CAPE Declaration Process

CBP's CAPE (Consolidated Administration and Processing for Entries) system consolidates refund requests across multiple entries rather than processing them one at a time. Key facts:

- Phase 1 (unliquidated entries): CBP processes within 45 days of accepting the declaration

- Phase 2 (finally liquidated entries): No announced timeline yet, but filing now secures your queue position

- Protest rights under 19 USC §1514 provide a 180-day window for liquidated entries — time-sensitive for some IORs

The window is not open indefinitely. CBP processes CAPE Declarations in the order received, and over 26,000 importers had already registered by late March 2026.

Where Price Ridge Fits

Price Ridge was built for importers who paid IEEPA tariffs but don't have customs counsel on retainer and have never filed a reliquidation request. For qualifying companies ($10,000 or more in IEEPA duties paid), Price Ridge manages the entire process:

- Analyzes your import history to identify IEEPA-affected entries and calculate refund amounts

- Works directly with your customs broker to gather CF7501 entry summaries, duty payment records, and commercial invoices

- Prepares and submits the CAPE Declaration to CBP within days of receiving documents

- Monitors progress through CBP review and reliquidation, handling any agency inquiries

- Receives the CBP refund and remits your share

Pricing is contingency-based with no upfront cost — you pay nothing unless the refund is recovered. For IORs who need cash now, Price Ridge also offers a claim financing option that purchases claims outright at 75–85 cents on the dollar.

Reach Price Ridge at refunds@priceridge.com for a free eligibility review with no obligation.

Frequently Asked Questions

Does the importer of record pay the tariff?

Yes. Paying all applicable tariffs, duties, and fees at the time of entry is one of the IOR's core legal obligations under US customs law. The IOR is also the party with standing to seek a refund if tariffs are later determined to have been improperly assessed.

What is the difference between IOR and EOR?

The IOR manages import-side compliance in the destination country: paying duties, filing the customs entry, and meeting regulatory requirements on arrival. The EOR manages export-side compliance in the origin country, ensuring goods are properly licensed and declared before departure. Both are distinct legal roles in the same cross-border transaction.

Can anyone be an IOR?

No. The IOR must be a registered business entity or individual with a valid EIN, SSN, or CBP-issued importer ID, and must be able to assume legal and financial responsibility for the shipment. Foreign entities without a US presence can qualify by obtaining a CBP-assigned number, typically through a licensed customs broker.

What happens if the importer of record fails to comply with customs regulations?

Consequences range from shipment holds and delays to fines, liquidated damages, goods seizure, and loss of import privileges. CBP can also audit entries for up to five years after liquidation, so past compliance failures remain within reach.

Who is the importer of record on a DDP shipment?

Under DDP terms, the seller takes on the IOR role and is responsible for all customs clearance, duties, and compliance in the destination country. Many foreign sellers use a third-party IOR service to manage this responsibility, particularly when they lack a US entity or CBP experience.

Can a foreign company be the importer of record in the US?

Yes. A foreign company can serve as US IOR, but must obtain a CBP-assigned importer ID number via Form 5106 — since they lack a US EIN — and typically must work through a licensed US customs broker to manage filings and bond requirements.