Duty drawback is a federal refund program that has been on the books since 1789, making it one of the longest-standing trade incentives in U.S. history. It allows importers and exporters to recover up to 99% of duties, taxes, and certain fees paid on imported goods — provided those goods are later exported, destroyed, or used to manufacture products that are exported.

This guide covers everything a business owner needs to know: the formal definition, the main claim types with real-world examples, who qualifies, how the filing process works, and the most common mistakes that cost companies their refunds. No customs background required.

Key Takeaways

- Eligible businesses can recover up to 99% of duties, taxes, and certain fees paid on imported goods that are later exported or destroyed

- The three most common claim types are manufacturing drawback, unused merchandise drawback, and rejected merchandise drawback

- Claims must be filed within five years of the original importation date — missing this deadline forfeits the refund permanently

- All drawback claims must be filed electronically through CBP's Automated Commercial Environment (ACE) system — so having your import documentation organized before filing is essential

- Section 301 (China) tariffs are eligible for traditional drawback; IEEPA tariffs imposed under executive order are not covered by standard drawback rules and require a separate CBP refund process

What Is Duty Drawback?

Duty drawback is a refund of duties, internal revenue taxes, and fees collected by the U.S. government upon importation. The refund applies when that merchandise — or a qualifying substitute — is subsequently exported, destroyed under CBP supervision, or used to manufacture a product that is then exported or destroyed.

The program is codified under 19 U.S.C. §1313 and administered by U.S. Customs and Border Protection (CBP). It dates to 1789, and was most recently modernized by the Trade Facilitation and Trade Enforcement Act of 2015 (TFTEA), with implementing regulations taking effect in February 2019.

How It Differs from a Standard Customs Refund

A standard customs refund corrects a payment error — for example, an overpayment. Duty drawback is different. It's a policy-based incentive tied to what ultimately happens to the goods after import. Goods that never reach American consumers simply shouldn't bear the full cost of import duties.

This distinction matters practically. You're not correcting a mistake. You're claiming a refund you're entitled to based on your export or destruction activity.

The Recovery Ceiling

In most cases, businesses recover up to 99% of eligible duties and fees — not 100%. Two things to know about that ceiling:

- The 1% retained by CBP is statutory and non-negotiable

- Recovery applies only to goods meeting specific program criteria

Understanding who qualifies — and under which program type — is where most first-time claimants need guidance.

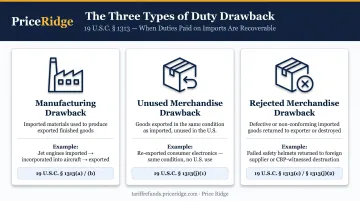

Main Types of Duty Drawback (with Examples)

Manufacturing Drawback

Manufacturing drawback applies when imported materials are incorporated into a finished product that is subsequently exported or destroyed. Two statutes govern it: 19 U.S.C. §1313(a) (direct identification) and §1313(b) (substitution).

Example: An aircraft manufacturer imports jet engines from overseas and pays customs duties on entry. When the finished aircraft is exported to a foreign airline, the manufacturer can file a drawback claim to recover the duties originally paid on those engines.

The substitution version (§1313(b)) removes the traceability burden: companies can match exports of a commercially interchangeable product against imports of a similar one, without linking specific imported goods to specific exported goods.

Unused Merchandise Drawback

Unused merchandise drawback (19 U.S.C. §1313(j)) applies when imported goods are exported or destroyed without ever being used or sold in the United States.

Example: A U.S. retailer imports a shipment of consumer electronics, but the products don't sell domestically and are re-exported to a distributor abroad. Because the goods were never used in the U.S., the retailer can file for unused merchandise drawback on the duties originally paid.

According to GAO's analysis of the drawback program, substitution unused merchandise drawback is the largest category by dollar value. This makes it the primary drawback category for distributors, retailers, and importers who regularly re-export inventory.

Rejected Merchandise Drawback

Rejected merchandise drawback (19 U.S.C. §1313(c)) applies when imported goods are defective, fail to conform to specifications, or are shipped without the buyer's consent — and are returned to the foreign supplier or destroyed.

Example: A sporting goods company imports a large batch of helmets that fail safety inspections. Rather than selling them, the company returns them to the manufacturer overseas or destroys them under CBP supervision, then files a claim to recover the import duties paid.

Other Drawback Types Worth Knowing

Beyond the three main types, two narrower categories apply in specific situations:

- Retail returns: A variation of rejected merchandise drawback covering goods sold at retail and subsequently returned by consumers

- Petroleum derivatives drawback (19 U.S.C. §1313(p)): Applies to crude petroleum or petroleum-derived goods exported within a statutory timeframe — relevant to refiners and energy companies

Who Qualifies for Duty Drawback?

Core Eligibility Requirements

To qualify, a business must meet two conditions:

- Paid duties or fees on imported merchandise

- That merchandise was exported, destroyed under CBP supervision, used in manufacturing an exported product, or returned due to defect

The claimant can be the importer, the exporter, or an intermediate party in the transaction — not just the entity that originally paid the duties.

Industries That Commonly Benefit

Drawback applies across many industries:

- Electronics and technology

- Apparel, footwear, and textiles

- Automotive parts and components

- Industrial equipment and machinery

- Chemicals and materials

- Consumer goods and retail

- Aerospace and defense

- Oil refining and energy

The Five-Year Filing Window

Claims must be filed within five years of the original importation date. This deadline is firm under 19 U.S.C. §1313 — missing it means permanently forfeiting the refund, with no exceptions.

If your company has been importing for years without filing drawback claims, you may have multiple years of recoverable duties still within that window — but each passing year closes off the oldest eligible entries for good.

Quick Eligibility Self-Check

You likely have drawback potential if you can answer yes to two or more of these:

- Does your company import goods into the U.S.?

- Do you export goods, or use imported materials in products you export?

- Have you paid duties, tariffs, or customs fees on imported merchandise?

- Do you maintain import and export documentation?

How the Duty Drawback Process Works

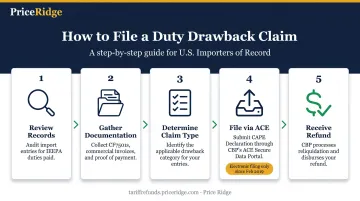

Step-by-Step Overview

- Review records — Identify import and export transactions with potential drawback eligibility across the past five years

- Gather documentation — Import entry summaries (CBP Form 7501), commercial invoices, bills of lading, export proof, and manufacturing records where applicable

- Determine claim type and matching methodology — Manufacturing, unused merchandise, rejected merchandise, or substitution

- File electronically via ACE — All claims must be submitted through CBP's Automated Commercial Environment. Paper claims are no longer accepted; the transition to electronic-only filing occurred in February 2019

- Receive refund — Up to 99% of eligible duties paid, subject to CBP review and liquidation

The Role of Customs Brokers

Most drawback claims are filed through licensed customs brokers, who handle documentation assembly, claim preparation, and ACE submission on behalf of the claimant. CBP confirms that licensed brokers with valid national permits may file on a company's behalf — which means most importers never interact directly with the ACE portal.

The Accelerated Payment Privilege (APP), governed by 19 C.F.R. §190.92, allows qualifying claimants to receive estimated drawback before final liquidation. According to a GAO report, accelerated payments are generally issued within 21 days of claim acceptance in ACE. By contrast, standard processing can exceed three years for full desk reviews.

Recordkeeping Requirements

Under modernized drawback regulations (19 C.F.R. §190.10), claimants must retain import and export documentation for three years from liquidation of the claim. Required records include:

- Commercial invoices

- Bills of lading or air waybills

- Export declarations

- Entry summaries and duty payment records

Incomplete or missing records are the primary reason drawback claims are delayed or denied.

Common Mistakes When Filing Duty Drawback Claims

The Three Costliest Errors

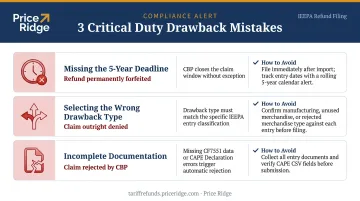

Missing the five-year deadline is the most irreversible error in drawback. Once the window closes, there's no mechanism to file late — the refund is gone for good.

Selecting the wrong drawback type leads to outright denial. Filing an unused merchandise claim when the facts only support a manufacturing claim, or vice versa, fails because the documentation requirements differ significantly between types.

Incomplete documentation is one of the most frequent causes of rejection. A missing bill of lading, a gap in export proof, or an unlinked import entry can all sink a claim. CBP requires that all required data be successfully transmitted electronically as part of a complete claim under 19 C.F.R. §190.51.

The Substitution Matching Problem

For substitution drawback specifically, CBP requires proof of commercial interchangeability between the imported and substituted goods. This is an objective, market-based standard that considers governmental and industry standards, HTS classification, part numbers, and relative value. Companies that treat substitution as a formality routinely get denied — CBP applies this standard strictly, and meeting it requires documented evidence, not assumptions.

Audit Risk

A 2019 DHS OIG report found that CBP's drawback system lacked adequate automated controls to prevent excessive claims. CBP audits drawback filings, and approved claims can be reversed if the underlying recordkeeping doesn't hold up. Working with a customs specialist and maintaining a systematic documentation process before filing significantly reduces this risk. The implication is straightforward: clean recordkeeping isn't optional — it's the difference between a refund that sticks and one that gets clawed back.

Duty Drawback and Today's Tariff Environment

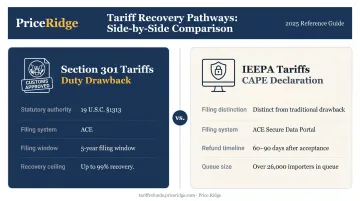

Section 301 Tariffs Are Drawback-Eligible

Companies paying elevated duties under Section 301 of the Trade Act of 1974 — the China tariffs — have a direct drawback opportunity. CBP has confirmed that Section 301 duties are eligible for duty drawback when the underlying merchandise is subsequently exported or used to manufacture exported goods.

For businesses that have absorbed years of elevated import costs on China-origin goods and are now exporting finished products or re-exporting inventory, those duties are directly recoverable through a standard drawback claim.

IEEPA Tariffs: A Separate Recovery Pathway

Importers who paid tariffs imposed under the International Emergency Economic Powers Act (IEEPA) — a more recent and legally distinct category of duties — face a different situation. These tariffs have been challenged in court, and a separate recovery pathway exists through CBP's CAPE (Claims Against Prior Entries) Declaration process, which is distinct from traditional duty drawback under 19 U.S.C. §1313.

The CAPE process involves filing a declaration listing eligible CBP entries through the ACE Secure Data Portal. CBP states that valid IEEPA refunds are generally issued within 60 to 90 days after acceptance of the CAPE Declaration.

For importers who paid IEEPA tariffs and want to pursue this specific recovery pathway, Price Ridge manages the entire CAPE process on a contingency basis with no upfront cost. Their end-to-end service includes:

- Free eligibility review and entry audit

- CF7501 documentation collection coordinated with your customs broker

- CAPE Declaration preparation and ACE Secure Data Portal submission

- CBP liaison and response handling throughout the process

- Refund disbursement coordination

For claims of $500,000 or more in IEEPA duties paid, Price Ridge also offers an outright claim purchase at 75–85¢ on the dollar for immediate cash. Reach them at refunds@priceridge.com.

Timing matters on both fronts. Duty drawback claims under Section 301 carry a five-year filing window from the date of importation. On the IEEPA side, the CAPE queue already had over 26,000 importers registered as of early 2026 — CBP processes claims in order of submission, so earlier filings move to the front of the line.

Frequently Asked Questions

What is duty drawback?

Duty drawback is a U.S. government refund program under 19 U.S.C. §1313 that allows importers, exporters, or intermediate parties to recover up to 99% of duties, taxes, and certain fees paid on imported goods that are subsequently exported, destroyed under CBP supervision, or used to manufacture exported products.

What is the difference between duty drawback and a customs refund?

A standard customs refund corrects a payment error such as an overpayment. Duty drawback is not correcting a mistake — it's a policy-based incentive that rewards exporters by refunding duties on goods that ultimately leave the U.S. market and never reach American consumers.

Who is eligible for duty drawback?

Importers, exporters, or other parties in the transaction may qualify if they paid duties on goods later exported, destroyed under CBP supervision, or used in exported manufactured products. Eligible industries include manufacturing, distribution, retail, and energy.

Is duty drawback still available?

Yes. Drawback remains an active CBP program, modernized by the Trade Facilitation and Trade Enforcement Act of 2015 and now filed electronically through the ACE system. The five-year filing window from the date of importation still applies.

How long do I have to file a duty drawback claim?

Claims must be filed within five years of the date the goods were originally imported. This deadline is strict — missing it forfeits the refund permanently. Companies with older unclaimed imports should assess eligibility as soon as possible.

Can Section 301 or IEEPA tariffs be recovered through duty drawback?

Section 301 duties are generally eligible for duty drawback when merchandise is exported or used in exported manufactured goods. IEEPA tariffs follow a different path: the CBP CAPE Declaration process, which is separate from the traditional drawback program under 19 U.S.C. §1313.