Key Takeaways

- The Supreme Court struck down IEEPA tariffs 6-3 on February 20, 2026, making an estimated $175 billion in duties legally refundable

- S.3905 (Tariff Refund Act of 2026) would require CBP to return those payments within 180 days, with interest

- Importers with finally liquidated entries are explicitly covered — a critical protection that doesn't exist without legislation

- CBP's CAPE process launched April 20, 2026 — queue position matters, and early filers hold a real advantage

- Act now — eligibility and queue position aren't contingent on the bill passing

Introduction

On February 20, 2026, the Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that the International Emergency Economic Powers Act does not authorize the President to impose tariffs. That ruling created a refund obligation on an estimated $175 billion in duties collected from U.S. importers since April 2025.

Six days later, Senate Finance Committee Ranking Member Ron Wyden introduced the Tariff Refund Act of 2026 (S.3905): legislation requiring CBP to return those payments within 180 days, with interest, and giving small businesses priority in the refund queue.

This article covers what the bill actually says, who qualifies, how the refund process works through CBP's CAPE system, and what steps importers should take right now, regardless of whether the bill becomes law.

What Is the Tariff Refund Act of 2026?

The Tariff Refund Act of 2026 is Senate bill S.3905, introduced on February 24, 2026. Its central purpose: requiring CBP to refund the estimated $175 billion in IEEPA tariffs the administration collected.

Sen. Ron Wyden (D-OR) is the official sponsor, joined by 26 co-sponsors. A February 26, 2026 Senate Finance press release framed the rollout as a joint effort by Wyden, Sen. Edward Markey (D-MA), and Sen. Jeanne Shaheen (D-NH).

Why a Law Was Necessary

Without legislation, the refund process sits in legal gray area. CBP has no statutory obligation to process refunds on any particular timeline, and without a court order or enacted law, large corporations with dedicated customs counsel are positioned to move first. The Tariff Refund Act is designed to solve three problems:

- Remove timeline uncertainty — mandating 180-day processing instead of indefinite delays

- Protect small businesses — prioritizing them in the refund queue explicitly

- Cover liquidated entries — overriding the normal finality rules that would otherwise block many importers

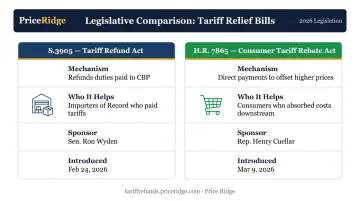

What the Bill Is Not

S.3905 is frequently confused with H.R. 7865, the American Consumer Tariff Rebate Act of 2026, introduced by Rep. Henry Cuellar (D-TX) on March 9, 2026. The two bills target different problems entirely:

| Bill | Mechanism | Who It Helps |

|---|---|---|

| S.3905 — Tariff Refund Act | Refunds duties paid to CBP | Importers of Record who paid the tariffs |

| H.R. 7865 — Consumer Tariff Rebate Act | Direct payments to offset higher prices | Consumers who absorbed the cost downstream |

As of early 2026, S.3905 was introduced by minority-party senators in a Republican-controlled Senate (53 Republican seats), with no floor vote scheduled. The bill may not pass — but its introduction creates public pressure for CBP to define a clear refund process. For importers, that means the window to file CAPE Declarations and secure a position in the processing queue matters now, regardless of how the legislation resolves.

The IEEPA Tariff Background

On April 2, 2025 — branded by the White House as "Liberation Day" — President Trump signed Executive Order 14257, invoking IEEPA to impose sweeping reciprocal tariffs starting at 10%, with higher rates for specific countries listed in Annex I.

Small businesses sued almost immediately, arguing IEEPA was designed for genuine national security emergencies, not broad trade renegotiation. The Supreme Court heard oral arguments on November 5, 2025, and issued its 6-3 ruling on February 20, 2026 in Learning Resources, Inc. v. Trump, holding that IEEPA simply does not authorize tariff imposition.

What Happened After the Ruling

The administration moved quickly. Within 24 hours, it imposed a temporary 10% global import surcharge under Section 122 of the Trade Act of 1974 — which allows temporary surcharges for up to 150 days — while exploring Section 301 and Section 232 as longer-term replacement authorities.

Key CBP guidance followed immediately:

- CSMS #67834313 (February 22, 2026) confirmed IEEPA duties were no longer in effect

- Section 232 and Section 301 tariffs remained fully operative — unaffected by the ruling

- Past IEEPA payments became legally refundable; future tariff exposure shifted to other authority

For importers, that means the refund window is open — but navigating the CBP filing process requires moving quickly to secure your position in the processing queue.

Key Provisions of the Tariff Refund Act of 2026

The bill's operative language in Section 3 of S.3905 establishes five specific mandates:

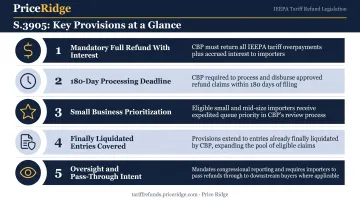

Provision 1: Mandatory Full Refund With Interest

Section 3(a) requires CBP to refund — with interest — all IEEPA tariffs collected from importers, "notwithstanding 19 U.S.C. 1514 or any other law." The interest component is meaningful: it compensates importers for the time-value of funds held by the government, which for large claims over a year-plus period can represent significant additional recovery.

Provision 2: 180-Day Processing Deadline

CBP must complete all refund payments within 180 days of enactment. Without this deadline, the administration could process refunds at its own pace indefinitely, and no voluntary refund timeline was announced following the Supreme Court ruling.

Provision 3: Small Business Prioritization

Section 3(c) directs CBP to prioritize small business concerns when disbursing refunds, and Section 3(d) requires CBP to coordinate with the SBA to give small importers information about documentation requirements and expected timelines. Without explicit prioritization, large corporations with established customs counsel would reach the front of the queue first — leaving smaller importers waiting longest for money they're owed.

Provision 4: Finally Liquidated Entries Are Covered

This is the provision most importers overlook — and for companies with entries from early-to-mid 2025, it's the one that determines whether any refund is possible at all.

Under standard customs law, once CBP liquidates an import entry (formally finalizing the duty assessment, typically within one year of entry), that determination becomes final under 19 U.S.C. 1514. Importers generally have only 180 days after liquidation to file a protest.

Many IEEPA duties from early-to-mid 2025 have already been liquidated. Under normal rules, those importers would have no path to a refund.

Section 3(b) directly overrides this. It requires CBP to reliquidate entries that were already closed before the bill's enactment (at the rate applicable without IEEPA tariffs) and issue the corresponding refund. The practical effect:

- Entries already liquidated are reopened and recalculated at pre-IEEPA duty rates

- Importers who missed the standard protest window are still eligible for a full refund

Without this provision, much of the $175 billion in duties paid would be unrecoverable through any administrative mechanism.

Provision 5: Oversight and Pass-Through Intent

Section 3(e) requires CBP to report to relevant congressional committees every 30 days until all refunds are paid. Section 3(f) requires guidance on duty drawback claims within 60 days. Section 2 expresses the Sense of Congress that importers, wholesalers, and corporations should pass savings downstream to their customers.

Who Qualifies for a Tariff Refund

Primary Eligibility

Any U.S. Importer of Record that paid IEEPA tariffs between April 2, 2025 and the Supreme Court ruling on February 20, 2026 is eligible. The importer of record (the legal entity identified in Box 22 of CBP Form 7501) is the party with the refund right.

If a DDP supplier, freight forwarder, or third party was listed as the IOR on your entries, the refund right belongs to them, not you.

According to Cato Institute analysis, as of mid-December 2025, the government had collected IEEPA duties from approximately 34 million entries filed by more than 301,000 U.S. importers — the scope of affected businesses is broad.

Industries With Significant Exposure

Because IEEPA tariffs applied broadly across nearly all trading partners and product categories, qualifying importers span most of the economy:

- Electronics and technology components

- Industrial machinery and capital equipment

- Consumer goods and retail inventory

- Apparel, textiles, and footwear

- Automotive parts and assemblies

- Chemicals, materials, and pharmaceuticals

- Construction products and building materials

- Food, agriculture, and processed goods

- Medical devices and healthcare equipment

What Is NOT Covered

S.3905 covers only IEEPA-classified duties. The following are outside the bill's scope:

- Section 301 China tariffs (HTS 9903.88.xx) — remain in effect, not refundable under this bill

- Section 232 steel and aluminum tariffs (HTS 9903.80.xx / 9903.85.xx) — not covered

- Section 122 replacement tariffs imposed after the Supreme Court ruling — not covered

For importers with mixed duty exposure — common for China-sourced goods that carried both Section 301 and IEEPA duties simultaneously — only the IEEPA portion is recoverable.

How to File for a Tariff Refund: Steps to Take Now

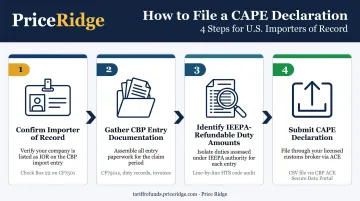

CBP launched its official refund mechanism — the CAPE Declaration (Consolidated Administration and Processing of Entries) — on April 20, 2026. Importers do not need the Tariff Refund Act to pass to begin the process.

Step 1: Confirm You Were the Importer of Record

Pull a sample CF7501 Entry Summary from your customs broker and check Box 22. If your company's name and IOR number appear there, you have a refund right. If a freight forwarder, supplier, or third party is listed instead, the refund right belongs to that entity.

Step 2: Gather CBP Entry Documentation

Work with your customs broker to collect:

- CF7501 Entry Summaries for all imports from April 2025 through February 2026

- Duty payment records showing IEEPA duty amounts by entry

- Commercial invoices and bills of lading for affected shipments

If your broker relationship has ended or records are incomplete, CBP's ACE Secure Data Portal Importer Query module can retrieve historical entries, but accessing it requires a CBP Power of Attorney.

Step 3: Identify Your IEEPA-Refundable Duty Amounts

Not every dollar on a CF7501 is refundable. A line-by-line audit separates IEEPA-classified HTS codes (primarily 9903.01.25 and related subheadings) from non-refundable Section 301 and Section 232 duties. This audit produces the actual refund amount.

Step 4: File a CAPE Declaration

The CAPE Declaration is a CSV-format file, one row per CF7501 entry, submitted through the CAPE tab in CBP's ACE Secure Data Portal. CBP processes valid refunds within 60–90 days following acceptance, and processes claims in the order received. With 26,000+ importers already in the queue as of late March 2026, filing early directly affects when you get paid.

Price Ridge handles the full CAPE Declaration process for importers without in-house customs expertise, including:

- Eligibility review and entry audit

- CF7501 documentation collection with your broker

- CAPE Declaration preparation and ACE Portal submission

- Claim tracking through CBP reliquidation and disbursement

There's no upfront cost — Price Ridge works on contingency. For importers with $500,000 or more in IEEPA duties paid who need cash now rather than waiting on CBP's timeline, Price Ridge also purchases claims outright at 75–85 cents on the dollar. Start with a free eligibility review at refunds@priceridge.com.

Will the Tariff Refund Act Pass — and What If It Doesn't?

Straightforward assessment: the bill faces a difficult path. With 53 Republican seats in the Senate and minority-party sponsorship, S.3905 is unlikely to pass without broader bipartisan support or administration endorsement — neither of which has materialized.

The legislative track isn't the only one in play, though. The Trump administration acknowledged in court filings its legal obligation to refund unlawfully collected IEEPA tariffs. The Court of International Trade issued a March 4, 2026 nationwide refund order. CIT Slip Op. 26-47 (May 7, 2026) separately confirmed the government's good-faith efforts toward refunding the duties. CBP's CAPE process is already operational.

The Real Risk for Importers Without Help

The problem isn't whether refunds will happen — it's who gets paid first and how completely. An unregulated process without legislated deadlines or small business prioritization will naturally favor:

- Large corporations with customs attorneys already on retainer

- Importers with clean documentation who file early

- Companies that understand CBP's CAPE process and format requirements

Small and mid-size importers without dedicated customs resources face real risk of delays, lost entries from missed CBP inquiries, or claim rejections due to formatting errors.

That's the gap the Tariff Refund Act was designed to close. Whether or not it passes, the window to secure your position in CBP's processing queue is open now — and waiting for legislative certainty means ceding ground to importers who are already filing. Price Ridge offers a free eligibility review to help you understand what you're owed and what filing requires.

Frequently Asked Questions

What is the Tariff Refund Act of 2026?

The Tariff Refund Act of 2026 (S.3905) is a Senate bill introduced by Sen. Ron Wyden and 26 co-sponsors on February 24, 2026. It requires CBP to refund, with interest, the estimated $175 billion in IEEPA tariffs the Supreme Court ruled unconstitutional — within 180 days of enactment.

Who qualifies for tariff refunds under the Tariff Refund Act?

Any U.S. importer of record who paid IEEPA tariffs between April 2, 2025 and February 20, 2026 is potentially eligible. This includes importers with already-liquidated CBP entries: Section 3(b) of the bill explicitly covers these through mandatory reliquidation authority.

How do I file for a tariff refund?

The bill has not been enacted, so no legislated filing process exists yet. Importers can act now by gathering CF7501 entry documentation and submitting a CAPE Declaration through CBP's ACE Secure Data Portal. Formatting errors cause full rejections, so working with a specialist before filing is worth the step.

Will tariff refunds actually be issued?

A refund process is expected regardless of whether the bill passes. The administration acknowledged its legal refund obligation in court, CBP launched the CAPE process, and the Court of International Trade issued a nationwide refund order in March 2026. Timeline and accessibility remain uncertain without legislated deadlines.

What is the difference between the Tariff Refund Act and the American Consumer Tariff Rebate Act?

The Tariff Refund Act (S.3905) reimburses importers who directly paid the unconstitutional IEEPA tariffs. The American Consumer Tariff Rebate Act (H.R. 7865) provides direct payments to consumers to offset higher prices caused by tariffs. They are separate bills with different sponsors and different mechanisms.

What happens to my refund claim if the Tariff Refund Act doesn't pass?

Importers can still pursue refunds through CBP's CAPE process and ongoing litigation. Without legislated deadlines, the process will likely be slower and less structured, which makes early filing more important. Importers with large claims who need cash now can also sell their claim outright rather than waiting for CBP processing.