The money is there. The refund pathway exists. But the process is not automatic — and for manufacturers, distributors, retailers, and e-commerce sellers without in-house customs expertise, the path forward is far from obvious.

Missing key deadlines or filing incorrectly could mean losing refund rights entirely. This guide explains what the IEEPA refund process is, how CBP's CAPE system works, which entries qualify, what legal factors are affecting timelines, and the most common mistakes importers make.

Key Takeaways

- The Supreme Court ruled in February 2026 that IEEPA tariffs were unlawful — importers are entitled to refunds plus interest

- Importers must actively file a CAPE Declaration to secure their position in CBP's refund queue

- Entry eligibility turns on liquidation status — unliquidated, recently liquidated, or finally liquidated

- The DOJ has appealed the universal refund order, creating real uncertainty for finally liquidated entries

- Two-year filing deadlines are approaching — importers with early-2025 entries should not wait

What Is the IEEPA Tariff Refund Process?

The IEEPA tariff refund process is the administrative and legal pathway through which U.S. importers recover duties collected under IEEPA executive orders — between February 4, 2025, when the first orders took effect, and the Supreme Court's February 20, 2026, ruling.

The Legal Trigger

In Learning Resources, Inc. v. Trump (consolidated with Trump v. V.O.S. Selections, Inc.), the Supreme Court held that IEEPA does not authorize the President to impose tariffs — the authority to regulate importation does not encompass the taxing power. The Federal Circuit had affirmed the Court of International Trade's summary judgment for plaintiffs on August 29, 2025; the Supreme Court affirmed that judgment on February 20, 2026.

That ruling opened two parallel refund pathways:

- CBP's CAPE system — the administrative route for most importers

- CIT litigation under 28 U.S.C. § 1581(i) — the court route for importers with finally liquidated entries who cannot access CAPE

How This Differs from a Standard Customs Protest

A standard protest under 19 U.S.C. § 1514 challenges a CBP decision. IEEPA refunds are different: CBP was simply enforcing an executive order it had no authority to question.

CBP cannot rule on the constitutionality of a presidential order. That's why the standard protest route doesn't apply here.

The correct paths are:

- CAPE Declaration — for importers with entries still within CBP's processing window

- CIT complaint — for importers with finally liquidated entries who cannot use CAPE

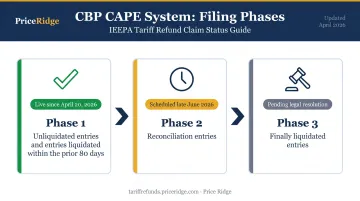

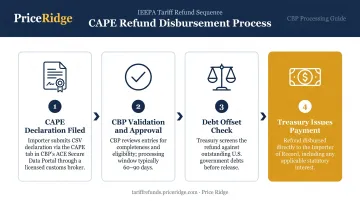

How the CAPE Refund Process Works

CBP built CAPE — Consolidated Administration and Processing of Entries — specifically to handle the unprecedented volume of IEEPA refund claims without processing them entry by entry. The system operates in phases:

| Phase | Status | Scope |

|---|---|---|

| Phase 1 | Live since April 20, 2026 | Unliquidated entries and entries liquidated within the prior 80 days |

| Phase 2 | Scheduled for late June 2026 | Reconciliation entries |

| Phase 3 | Pending legal resolution | Finally liquidated entries |

Filers submit CAPE Declarations through the CAPE tab inside CBP's ACE Secure Data Portal as a CSV file. ABI cannot be used. The filer must be the Importer of Record or an authorized licensed customs broker.

Step 1: Determine Entry Status and Eligibility

Before anything else, identify each entry's liquidation status — this single factor determines which refund path is available:

- Unliquidated: CBP has not yet issued a final duty determination; eligible for Phase 1 CAPE processing directly

- Recently liquidated (within 80 days): Also eligible for Phase 1; CBP retains authority under 19 U.S.C. § 1501 to voluntarily reliquidate within 90 days, with a 10-day operational buffer applied

- Finally liquidated: Beyond the 80-day window; requires Phase 3 CAPE processing or CIT litigation (the most complex category)

For importers without customs expertise, Price Ridge offers a free, no-obligation eligibility review that audits every entry by liquidation status and calculates the estimated refund amount before any engagement is signed.

Step 2: Prepare and File the CAPE Declaration

Once eligibility is confirmed, the CAPE Declaration — a CSV file with one row per CF7501 entry summary — is submitted through the ACE Secure Data Portal. Each row must include:

- Entry number and port code

- Importer of Record (IOR) number

- Total entered value

- IEEPA duty amount

- HTS subheading and country of origin

Queue position depends on when the declaration is submitted. With 26,000+ importers already registered as of late March 2026, every day of delay means a later position. CBP rejects any filing with a formatting error (wrong column order, missing IOR number, mismatched HTS code), sending the importer to the back of that queue.

Given these stakes, Price Ridge prepares and submits CAPE Declarations within days of receiving required documents — running pre-submission schema validation through its licensed customs broker partners before the file ever reaches CBP.

Step 3: Refund Approval and Disbursement

Once CBP validates and approves a claim, the U.S. Department of Treasury — not CBP — issues the actual payment. CBP states refunds are generally issued within 60–90 days after the CAPE Declaration is accepted. Two important cautions:

- If the importer owes outstanding debts to the U.S. government, refunds may be offset before disbursement

- Approved refunds include interest, calculated under 19 U.S.C. § 1505 using the rate framework in 26 U.S.C. § 6621

Which Import Entries Qualify for a Refund

Unliquidated Entries

CBP processes these through Phase 1 without requiring additional legal action. The entry is liquidated without the IEEPA duties applied, and the importer receives the difference.

Recently Liquidated Entries (Within 80 Days)

Entries liquidated within 80 days of the CAPE filing date are also Phase 1 eligible. The legal authority is 19 U.S.C. § 1501, which allows CBP to voluntarily reliquidate within 90 days of original liquidation. CBP applies a 10-day buffer, making the practical window 80 days.

Finally Liquidated Entries

An entry becomes finally liquidated when CBP's assessment is final and the 180-day protest window under 19 U.S.C. § 1514 has expired. These entries are the most legally complex:

- CBP has stated it cannot process them through CAPE without a court order specific to each importer

- The DOJ's appeal directly targets this category (more on that below)

- Importers with significant finally liquidated entries should evaluate filing a CIT complaint to preserve refund rights before the two-year limitation period under 28 U.S.C. § 2636(i) expires

Current CAPE Exclusions

Phase 1 excludes several entry categories regardless of liquidation status:

- Entries not in CBP's ACE system (including certain postal service entries)

- Drawback entry type 47 entries (though CBP encourages placing eligible entry summaries on a CAPE Declaration before filing a drawback claim)

- Entries with open protests

- Certain AD/CVD entries pending liquidation

- Reconciliation entries where the reconciliation entry has already been filed (addressed in Phase 2)

Key Legal Factors Affecting Your Refund Timeline

The DOJ Appeal

Holland & Knight reports that DOJ filed notices of appeal in the Federal Circuit on June 3, 2026 related to the CIT's IEEPA refund orders. The appeal does not halt Phase 1 CAPE refunds already in progress.

Its primary effect is on finally liquidated entries. The DOJ has indicated it will seek a stay for this category — if granted, that stay would halt refunds for importers who have not filed their own CIT lawsuit. For importers whose exposure is concentrated in early-2025 entries that are now finally liquidated, the appeal forces a practical choice: wait and see, or file a protective CIT complaint.

The Two-Year Filing Deadline

Under 28 U.S.C. § 2636(i), a civil action under 28 U.S.C. § 1581(i) at the CIT is barred unless commenced within two years after the cause of action first accrues. The precise accrual date requires legal confirmation — the statute says "first accrues," not expressly from liquidation. For importers with early-2025 entries, the implication is clear: a "wait and see" approach carries real deadline risk.

Consult independent legal counsel on whether filing a protective CIT complaint makes sense before that window closes.

Entry Accuracy Before Filing

CBP's review process means that filing a CAPE claim on entries with underlying errors can invite scrutiny. Common issues Price Ridge identifies during pre-filing audits include:

- Claiming Section 301 China duties (HTS 9903.88.xx) or Section 232 duties as IEEPA refunds — those are not covered

- Filing on entries where another party (supplier or freight forwarder) held the Importer of Record designation, as in DDP shipments

- Submitting broker summary invoices that aggregate duties without isolating the IEEPA component by line item

Resolving these before submission is what keeps a claim moving through CBP's queue rather than bouncing back for correction.

Common Misconceptions About IEEPA Refunds

"Refunds Are Issued Automatically"

This is false. CBP will not identify eligible importers and issue refunds without a claim. Each importer must actively submit a CAPE Declaration to secure a position in the processing queue. Delay in filing means delay in disbursement. If the legal landscape shifts, a later position in the queue creates more exposure.

"A Standard Protest Is the Right First Step"

CBP was enforcing a presidential executive order, not making an independent tariff determination. That distinction matters: CBP has no authority to rule on the constitutionality of that order, so a standard § 1514 protest is not the IEEPA refund path.

CAPE is the dedicated administrative route. Constitutional and statutory challenges belong at the CIT under 28 U.S.C. § 1581(i). Protests may still be relevant to specific liquidation finality and preservation issues depending on entry status, but they are not a substitute for the CAPE process.

"You Have to Wait Months or Years to See Any Money"

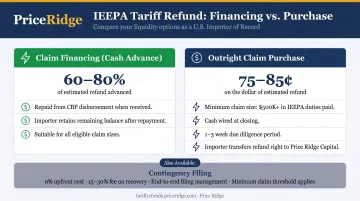

Not necessarily. For importers who need liquidity now, two alternatives exist:

- Claim financing (cash advance): Advances 60–80% of the estimated refund value against a pending CBP refund, repaid from the CBP disbursement when received. The importer retains the balance.

- Outright claim purchase: For claims of $500,000 or more in IEEPA duties paid, Price Ridge buys eligible claims at 75–85 cents on the dollar, wiring cash at closing after 1–3 weeks of due diligence. The importer receives immediate payment and transfers the refund right to Price Ridge.

For importers willing to wait for full CBP processing, Price Ridge's contingency-based filing service charges nothing upfront — a fee of 15–30% of the recovered refund is taken only when CBP disburses payment.

Frequently Asked Questions

How do I get a refund for IEEPA tariffs?

Eligible importers file a CAPE Declaration through the ACE Secure Data Portal through a licensed customs broker or a specialist like Price Ridge, which handles the full process. The declaration identifies affected entries and initiates the refund review. For finally liquidated entries, a complaint at the Court of International Trade may also be required to preserve your rights. Start with a free eligibility review at refunds@priceridge.com.

What would an IEEPA tariff refund mean for my business?

A refund recovers duties unlawfully collected under IEEPA executive orders, returned with statutory interest. For businesses that paid significant tariffs on imports from China, Vietnam, India, or other affected countries, this can be a substantial cash recovery that improves margins or frees up working capital.

What is the CAPE system and how does it work?

CAPE (Consolidated Administration and Processing of Entries) is the CBP platform built to process IEEPA refund claims at scale. Importers submit a CAPE Declaration via the ACE Secure Data Portal; CBP validates eligible claims, and Treasury issues payment — typically within 60–90 days for Phase 1 claims.

What does "finally liquidated" mean, and does it affect my refund eligibility?

An entry is finally liquidated when CBP has issued its formal duty determination and the 180-day protest window has expired, making the assessment final. These entries are currently the most difficult CAPE category because CBP requires a court order specific to each importer before processing them through Phase 3. The DOJ appeal adds further uncertainty, so importers with substantial finally liquidated entries should discuss their options with legal counsel.

What is the deadline to file for an IEEPA tariff refund?

There is no single universal deadline, but a two-year limitation period applies to CIT complaints under 28 U.S.C. § 2636(i) — for importers with finally liquidated early-2025 entries, that window is narrowing. Queue position matters too: CBP processes CAPE Declarations in order of receipt, and the queue already held more than 26,000 registered importers as of late March 2026.