That gap is costly. Unlike fixed claims with deterministic values, contingent claims carry embedded uncertainty that makes systematic valuation the difference between recovering fair value and walking away from money that was legitimately yours.

This guide is for finance professionals, business owners, legal practitioners, and importers who need to know what their contingent claims are actually worth — and why the methodology matters as much as the math.

Key Takeaways

- Contingent claim value comes down to three inputs: triggering-event probability, payout magnitude, and time value of money

- Three valuation approaches exist (market, income/expected value, options-based); the right choice depends on available data

- Probability assessment is the highest-leverage step; a 20-percentage-point shift on a $1M claim moves value by $200,000

- Documentation quality directly affects both assessed probability and negotiating leverage — gaps compress value

- Queue position, filing deadlines, and processing timelines are real economic variables, not just administrative details

What Is Contingent Claim Valuation?

A contingent claim is any financial right or legal entitlement whose realization depends on an uncertain future event. The category is broader than most practitioners assume:

- Stock options (value depends on price exceeding strike)

- Insurance claims (value depends on a covered event occurring)

- Litigation settlements (value depends on court outcome or defendant agreement)

- Warranty liabilities (value depends on product failure rates)

- Government refund claims — such as IEEPA tariff reimbursements awaiting CBP approval

Under ASC 450, a contingency is an existing condition involving uncertainty resolved when future events occur or fail to occur. IAS 37 similarly defines contingent assets and liabilities as dependent on uncertain future events outside the entity's control.

What Valuation Is Designed to Achieve

The goal is to translate an uncertain future payout into a defensible present value — usable for settlement negotiation, financial reporting, or investment decision-making.

This differs from standard asset valuation in one key respect: standard valuation assumes the cash flow exists with certainty. Contingent valuation must first estimate whether the cash flow will occur at all, then apply time-value discounting.

Probability assessment is the additional layer of complexity — and the primary source of valuation error when skipped.

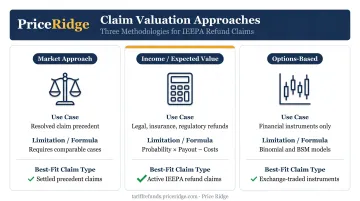

The Three Main Approaches to Valuing Contingent Claims

The correct approach depends on claim type, available data, and the degree of market comparability. No single method fits every situation.

Market Approach

The market approach estimates claim value by comparing it to similar claims that have already been resolved — analogous to comparable sales in real estate.

Best suited for: Personal injury settlements, business disputes in active litigation markets, insurance claims with deep historical databases.

Key limitation: Comparable cases are rarely identical. Adjustments for injury severity, jurisdiction, and defendant profile are always required. When precedent is thin, the adjustments required can outnumber the data points supporting them — meaning analyst judgment drives the result more than the comparables do.

Income (Expected Value) Approach

The income approach calculates claim value as:

(Probability of favorable outcome × Expected payout if outcome occurs) − Transaction costs, discounted to present value

A simplified example: a $500,000 potential recovery with a 60% probability of success and $50,000 in transaction costs yields an expected value of $250,000 before discounting.

This is the most widely used method in legal, insurance, and regulatory claim contexts because it ties directly to decision-making under uncertainty.

Academic work by Robert Rhee demonstrates that legal claim value depends on expected judgment, probability, risk, and time — not the gross face amount alone.

Options-Based (Derivative Pricing) Approach

Financial contingent claims — options, warrants, convertible bonds — are best valued using derivative pricing models:

- Binomial Model: Evaluates claims through a tree of possible price paths over discrete time steps, working backwards to determine present value

- Black-Scholes-Merton (BSM): Assumes continuous price changes and produces a closed-form solution based on underlying asset price, volatility, time to expiration, and risk-free rate

Both rely on the no-arbitrage principle: the claim's price must equal the cost of replicating its payoff using other instruments.

Important caveat: These models are appropriate for financial contingent claims where the underlying is actively traded. They are not appropriate for legal or regulatory claims where no market for the underlying exists.

When to use each:

- Market approach: claims with abundant resolved precedent

- Income/expected-value: legal, insurance, and regulatory refund claims

- Options-based: exchange-traded or structurally comparable financial instruments

How to Value a Contingent Claim: Step-by-Step Process

Valuing a contingent claim requires moving from claim definition through probability assessment, outcome projection, discounting, and transaction cost adjustment — in that order. Skipping or conflating steps is the most common source of valuation error.

Step 1: Define the Claim and Its Trigger Conditions

Identify three things before any calculation begins:

- What event must occur for the claim to be realized (court judgment, CBP approval, insurance event, option expiration)

- What the claimant receives upon that event

- Any conditions that could void or reduce the payout

Ambiguity in trigger definition propagates into every subsequent step. A refund claim whose eligibility is unclear, or a litigation claim whose damages theory is undefined, cannot be reliably valued.

Step 2: Assess the Probability of the Triggering Event

Probability assessment draws on historical data, expert opinion, and statistical modeling. For legal claims, this means evaluating liability strength, jurisdiction, and defendant profile. For regulatory refund claims, it means assessing legal validity of the underlying entitlement and the status of processing queues.

A 2025 NBER working paper on litigation risk frames legal claims as sequential and uncertain, with value affected by litigation stage and outcome uncertainty — reinforcing that probability updates as claims progress, not a fixed input.

Step 3: Project the Expected Financial Outcome

Once probability is established, estimate the magnitude of the payout across scenarios: best-case, base-case, and downside. For damage-based claims, this includes compensatory amounts, interest, and reductions for comparative fault.

For IEEPA tariff refund claims, the expected outcome is the total IEEPA duties paid on finally liquidated entries. That makes documentation of historical payment records central to the calculation.

In practice, this requires an entry-by-entry audit of every CF7501 entry summary — separating refundable IEEPA duties (HTS 9903.01.25 and related codes) from non-refundable Section 301 and Section 232 tariffs charged on the same entries. Price Ridge performs this audit for importers as part of its eligibility review, producing a verified baseline figure ready for CAPE Declaration CSV filing.

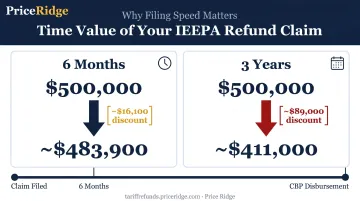

Step 4: Discount Future Cash Flows to Present Value

Because claim resolution takes time, future payouts must be discounted using the present value formula:

PV = FV ÷ (1 + r)ⁿ

The choice of discount rate matters. The Federal Reserve's H.15 release showed a 10-year Treasury yield of 4.47% and bank prime rate of 6.75% as of early June 2026 — useful reference points for selecting a rate appropriate to the claim's risk profile. Legal claims typically use a risk-adjusted rate reflecting resolution timing uncertainty; financial contingent claims use the risk-free rate in conjunction with risk-neutral probabilities.

To make this concrete, consider a $500,000 gross claim at a 6.75% discount rate:

| Timing | Present Value | Discount Applied |

|---|---|---|

| 6 months out | ~$483,900 | ~$16,100 |

| 3 years out | ~$411,000 | ~$89,000 |

The gross claim amount is identical in both scenarios. The present value is not.

Key Factors That Affect Contingent Claim Value

Probability of Outcome

Even small changes in assessed probability have an outsized impact on value. A shift from 50% to 70% likelihood on a $1M claim adds $200,000 in expected value — making probability the highest-leverage variable in the entire calculation. Sensitivity analysis across probability assumptions is standard practice in serious valuations.

Documentation and Evidence Quality

Across every claim type, the strength and completeness of supporting documentation affects both assessed probability and negotiating leverage. For IEEPA refund claims, the most common documentation gaps include:

- Missing or incomplete CF7501 entry summaries (broker went out of business, records not transferred)

- Aggregate duty figures without HTS line-item detail, making it impossible to isolate the refundable IEEPA portion

- IEEPA duty line items buried inside multi-line or consolidated entries

- Importer of Record (IOR) identity uncertainty on DDP shipments where the supplier was actually the IOR

Each gap compresses the assessed refund value because unverified entries cannot be included in the CAPE Declaration filing. Price Ridge addresses this through a dedicated Lost CF7501 Recovery service, retrieving records directly from CBP's ACE Secure Data Portal via power of attorney when importers lack access through their customs broker.

Resolution Timeline and Discount Rate

Longer timelines reduce present value. A claim worth $300,000 in three years is worth approximately $225,000 today at a 10% discount rate, versus $274,000 at 3%. That $49,000 gap widens with both the rate applied and the length of the wait.

For IEEPA refund claims, CBP processes CAPE Declarations in order received. Over 26,000 importers had already registered as of late March 2026. Every day of filing delay pushes queue position further back, which directly extends the timeline and reduces present value.

Legal and Regulatory Enforceability

A claim that is legally sound but procedurally complex carries additional risk that reduces current value. For IEEPA tariff refund claims, the Supreme Court's February 2026 ruling in Learning Resources, Inc. v. Trump established the legal basis for refundability. CBP launched the CAPE process on April 20, 2026 — but procedural timing still matters.

Two statutory deadlines govern refund eligibility:

- Protest rights (19 U.S.C. § 1514): expire 180 days after liquidation

- Voluntary reliquidation (19 U.S.C. § 1501): limited to 90 days from notice of original liquidation

Missing either window can make a CBP decision final and conclusive, eliminating the refund right entirely.

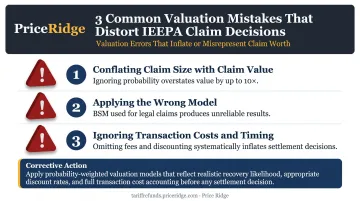

Common Mistakes in Contingent Claim Valuation

Three errors account for the majority of valuation failures — and each one consistently produces the same result: a number that looks right but leads to a bad decision.

- Conflating claim size with claim value. Many claimants treat the maximum possible payout as the claim's value, ignoring probability. A $1M claim with a 10% success probability is worth $100,000 — not $1M. Settling for $150,000 may be economically rational even when it feels like losing.

- Applying the wrong model. Using Black-Scholes-Merton for legal or regulatory claims, or applying settlement comparables to structurally novel claim types, produces unreliable valuations. The model must match the claim's underlying economics. Financial derivatives models require a tradeable underlying asset — something legal claims simply don't have.

- Ignoring transaction costs and timing. Many valuations stop at expected payout without subtracting the cost of reaching resolution — legal fees, filing costs, administrative expenses — and without discounting for time. These omissions systematically overstate claim value and produce settlement decisions that look favorable on paper but aren't economically justified.

Frequently Asked Questions

What are the three types of valuations?

The three main valuation approaches are the market approach (comparing to similar resolved claims), the income/expected value approach (probability-weighted future cash flows discounted to present value), and the cost approach (estimating what it would cost to replace or repair what was lost). The right method depends on claim type and data availability.

What is a contingent claim in simple terms?

A contingent claim is any financial right that only pays out if a specific condition is met — a stock option only has value if the stock price exceeds the strike price; a tariff refund only materializes if the refund is approved by the relevant authority. The payout is uncertain until that condition resolves.

What is the difference between a contingent claim and a standard claim?

A standard claim has a fixed, agreed-upon value (such as a fixed invoice). A contingent claim has an uncertain payout that depends on a future event. Valuing a contingent claim requires estimating the probability of that event; standard claim valuation does not.

How does the time value of money affect contingent claim valuation?

Because contingent claims may take months or years to resolve, the future payout must be discounted to present value. A claim worth $500,000 in three years is worth materially less today, and this discounting effect grows with both the resolution timeline and the discount rate applied.

What models are used to value options as contingent claims?

The two primary models are the Binomial Model, which maps price paths over discrete time periods using a decision tree, and the Black-Scholes-Merton (BSM) Model, which applies continuous-time math to produce a closed-form valuation from asset price, volatility, time to expiration, and the risk-free rate.

When should I get a professional to value a contingent claim?

Professional valuation matters most when a claim involves large dollar amounts, complex documentation, or tight deadlines — all of which affect assessed value and recovery speed. For IEEPA tariff refund claims specifically, Price Ridge offers free eligibility reviews with responses within one business day; reach them at refunds@priceridge.com.