Introduction

Both IEEPA and Section 232 have been used to impose tariffs on imported goods entering the United States — but treating them as interchangeable is a costly mistake.

The Supreme Court ruled 6-3 on February 20, 2026 in Learning Resources, Inc. v. Trump that IEEPA does not authorize the president to impose tariffs. CBP stopped collecting IEEPA duties for entries on or after February 24, 2026. Section 232 tariffs, grounded in an entirely different statute, were unaffected by that ruling and are actively expanding.

For importers, this distinction has direct dollar consequences. Duties paid under IEEPA authority may be refundable through CBP's CAPE Declaration process. Duties paid under Section 232 are not. This article breaks down exactly how the two authorities differ — and what those differences mean for your refund eligibility.

Key Takeaways

- The Supreme Court struck down IEEPA tariff authority on February 20, 2026; Section 232 tariffs remain fully in effect.

- Section 232 is product-specific (steel, aluminum, copper, autos, pharmaceuticals); IEEPA tariffs applied country-wide, covering dozens of trading partners.

- IEEPA tariffs on Chinese goods reached 145% — well above most Section 232 rates.

- Importers who paid IEEPA duties on goods outside Section 232 coverage may be eligible for refunds through CBP's CAPE system.

- Section 232 duties are not recoverable through the IEEPA refund process — only IEEPA-specific payments qualify.

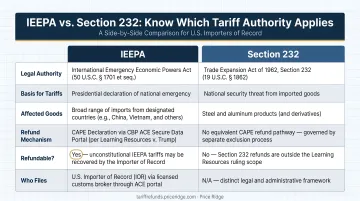

IEEPA vs. Section 232: Quick Comparison

The two authorities differ in legal foundation, scope, and — critically for importers — whether the duties paid are recoverable. Here's how they compare side by side.

| Feature | IEEPA | Section 232 |

|---|---|---|

| Statute | International Emergency Economic Powers Act, 1977 (50 U.S.C. § 1701) | Trade Expansion Act of 1962 (19 U.S.C. § 1862) |

| Trigger | Declared national emergency with "unusual and extraordinary" external threat | Commerce Dept. investigation finding import threat to national security |

| Tariff authority | Not expressly granted — Supreme Court held "regulate importation" insufficient | Explicitly contemplates tariff and import restriction authority |

| Product scope | Country-wide / trade-flow-wide | Product-specific by HTS code |

| Rates reached | Up to 145% on Chinese goods | 10–50% metals; 25% autos; up to 100% pharma |

| Current status | Invalidated — collection stopped Feb. 24, 2026 | Active and expanding |

| Refundable? | Yes — through CBP CAPE Declaration process | No |

The refundability gap is the key takeaway: if your duties were collected under IEEPA, you have a legal basis to recover them. Section 232 duties paid during the same period do not qualify.

What Is IEEPA?

The International Emergency Economic Powers Act (Pub. L. 95-223, enacted December 28, 1977) grants the president authority to regulate economic transactions following a declared national emergency originating outside the United States. Congress enacted IEEPA specifically to limit the executive emergency authority that had existed under the 1917 Trading with the Enemy Act.

Critically, IEEPA does not expressly mention tariffs. No president used it to impose tariffs until the Trump administration beginning in February 2025.

The IEEPA Tariff Actions

The first actions targeted drug trafficking:

- EO 14193 (Feb. 1, 2025) — 25% on Canadian imports

- EO 14194 (Feb. 1, 2025) — 25% on Mexican imports

- EO 14195 (Feb. 1, 2025) — initial 10% on Chinese imports, later raised to 20% under EO 14228

Then came the sweeping "reciprocal" tariffs under EO 14257 (April 2, 2025), applying a 10% baseline to all trading partners with higher country-specific rates for dozens of nations. China's reciprocal rate escalated to 125% under EO 14266. Combined with the fentanyl tariff, most Chinese goods faced a 145% total IEEPA rate.

The Legal Challenge and Supreme Court Ruling

Businesses challenged IEEPA tariffs on two grounds: IEEPA doesn't authorize unbounded tariff power, and no genuine "unusual and extraordinary" national emergency existed. The litigation moved quickly:

- May 28, 2025 — Court of International Trade (V.O.S. Selections, Inc. v. Trump) invalidated the IEEPA tariff authority

- August 29, 2025 — Federal Circuit affirmed

- February 20, 2026 — Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that IEEPA's power to "regulate" importation does not include tariff authority

What Happened After the Ruling

CBP acted within days of the ruling. Per CSMS #67834313 (issued February 22, 2026), IEEPA tariffs became inactive in ACE and CBP ceased collecting them for entries on or after February 24, 2026 at 12:00 a.m. ET.

The administration attempted to replace IEEPA authority with Section 122 of the Trade Act of 1974, though that authority was also subsequently challenged. In April 2026, CBP launched the CAPE Declaration refund system — giving importers a formal path to recover IEEPA duties already paid.

What Is Section 232?

Section 232 of the Trade Expansion Act of 1962 (19 U.S.C. § 1862) gives the president authority to restrict imports when the Commerce Department determines they "threaten to impair" U.S. national security. Unlike IEEPA, Section 232 explicitly contemplates tariff authority, a distinction that proved decisive in court.

The Investigative Process

Section 232 requires a structured path before tariffs can be imposed:

- A formal Commerce Department investigation is initiated

- Commerce produces a national security finding

- The president acts on that finding within statutory time limits

This procedural rigor is why Section 232 has survived multiple constitutional challenges.

The Federal Circuit upheld it in American Institute for International Steel (Feb. 28, 2020) and again in Transpacific Steel LLC v. United States (July 13, 2021), both relying on binding Algonquin precedent.

Current Section 232 Tariffs

Section 232 coverage has expanded substantially since 2018:

| Product | Rate | Effective |

|---|---|---|

| Steel, aluminum, copper (most categories) | 25–50% on full customs value | Apr. 6, 2026 (Proclamation 11021) |

| Russian aluminum categories | 200% | Per Proclamation 10522/11021 |

| Automobiles and auto parts | 25% | Apr. 3, 2025 (Proclamation 10908) |

| Pharmaceuticals and APIs | 10–100% (tiered) | Effective Jul.–Sep. 2026 |

A significant 2026 change: the Section 232 metals duties now apply to the full customs value of covered products — not just the metal content — for articles that are entirely or substantially made of steel, aluminum, or copper. This is a major cost shift for manufacturers of complex assemblies.

The scope continues to grow. Active investigations cover semiconductors, timber and lumber, commercial aircraft, and processed critical minerals, with additional categories under review.

IEEPA vs. Section 232: Key Differences for Importers

Legal Durability

Section 232 survived every court challenge because Congress explicitly delegated tariff authority through it. IEEPA never mentioned tariffs at all : the Supreme Court held that a general power to "regulate importation" is insufficient to impose duties. That gap is why Section 232 tariffs are expanding while IEEPA tariffs are being refunded.

Who Owes What — and Who Can Get Refunds

The financial split breaks down by product category:

- IEEPA tariffs were imposed on broad country-based trade flows. Goods in consumer electronics, apparel, medical devices, food and agriculture, industrial machinery, and hundreds of other categories were subject to these duties.

- Section 232 tariffs were imposed on specific products (steel, aluminum, copper, autos, pharmaceuticals) defined by HTS code.

Critically, goods already subject to Section 232 were explicitly excluded from the IEEPA reciprocal tariff framework under EO 14257. This means:

- Importers of steel, aluminum, and auto parts generally did not pay IEEPA tariffs on those products and cannot claim IEEPA refunds for them.

- Importers across a wide range of non-Section 232 goods — consumer products, apparel, electronics, food, medical devices — may have paid significant IEEPA tariffs that are now refundable.

Rate Levels and What's at Stake

The financial scale matters. IEEPA rates on Chinese goods reached 145% — more than double the highest Section 232 metal rates. For importers sourcing from China across 2025 and into early 2026, the cumulative duty exposure could be substantial. A single entry of industrial machinery or electronics components at 145% can translate into a six-figure refund claim.

Identifying Your Tariff Type

The way to determine which authority applied is straightforward: review your CBP entry summaries (CF7501) and look at the Chapter 99 HTSUS codes reported at the time of entry.

- IEEPA headings include 9903.01.25 (10% reciprocal), 9903.01.63 (China 125% reciprocal), and drug-trafficking headings such as 9903.01.20, 9903.01.04, and others.

- Section 232 metals headings run 9903.82.02 through 9903.82.17, plus Russian aluminum headings 9903.85.67 and 9903.85.68.

Your customs broker can pull this documentation. If you don't have an established broker relationship, Price Ridge coordinates retrieval directly, working with brokers to gather the records needed to support a claim.

Filing IEEPA Refund Claims

For importers who confirm IEEPA exposure, the refund process runs through CBP's CAPE Declaration system:

- Phase 1 covers unliquidated entries and entries within 80 days past liquidation

- Phase 2 covers finally liquidated entries — CBP hasn't announced a processing timeline, but filing now establishes your position in the queue

Price Ridge manages the entire CAPE Declaration process on a contingency basis with no upfront cost, covering:

- Eligibility review and document collection

- CAPE Declaration preparation and CBP filing

- Claim tracking through reliquidation and disbursement coordination

For importers who'd rather not wait for CBP processing, Price Ridge also offers an outright claim purchase at 75–85 cents on the dollar for immediate payment. The minimum claim size is $10,000 in IEEPA duties paid. A free eligibility review with a one-business-day response is available at refunds@priceridge.com.

Conclusion

IEEPA and Section 232 are not interchangeable. They differ in legal foundation, product scope, durability, and — most practically — refundability. Section 232 tariffs are here to stay and expanding into new product categories. IEEPA tariffs are invalid and recoverable.

For importers across manufacturing, retail, e-commerce, and distribution, this distinction could mean meaningful refunds on duties already paid. The window isn't unlimited, though. Two factors make timing matter:

- Liquidation status: Phase 1 eligibility requires entries to still be unliquidated or within the 80-day protest window

- Queue position: CBP processes claims in the order received — later filings wait longer

Price Ridge reviews entry history at no cost and files CAPE Declarations within days of receiving documents. The sooner you verify what you paid, the more recoverable entries remain on the clock.

Frequently Asked Questions

Does IEEPA apply to Section 232?

No. The two authorities are separate and do not stack. EO 14257, which imposed IEEPA reciprocal tariffs, explicitly excluded goods already subject to Section 232 measures. Importers of steel, aluminum, and auto parts were not subject to additional IEEPA duties on those products.

What is Section 232 of the steel Executive Order?

Section 232 of the Trade Expansion Act of 1962 (19 U.S.C. § 1862) authorizes the president to restrict or adjust imports found to threaten national security. The steel tariff — first imposed at 25% in 2018 via presidential proclamation — remains its most prominent application, though coverage has since expanded significantly.

What products are subject to Section 232 tariffs?

Current Section 232 products include steel, aluminum, copper, automobiles and auto parts (25%), and pharmaceuticals and APIs (rates from 10% to 100% depending on the product and country of origin). Investigations are underway for semiconductors, timber and lumber, commercial aircraft, and processed critical minerals.

Can importers get a refund on IEEPA tariffs already paid?

Yes. CBP launched the CAPE Declaration refund system in April 2026 to process IEEPA duty refunds. Phase 1 covers unliquidated and recently liquidated entries — importers should act promptly, as refund eligibility is tied to liquidation deadlines.

Are Section 232 tariffs still in effect?

Yes. Section 232 tariffs were not affected by the Supreme Court's IEEPA ruling and remain fully in force. Rates and product coverage have continued to expand under proclamations issued in both 2025 and 2026.

How do I know whether I paid IEEPA or Section 232 tariffs?

Review your CBP entry summaries (CF7501) and look at the Chapter 99 HTSUS codes. IEEPA duties appear under headings like 9903.01.25 and 9903.01.63; Section 232 metals appear under 9903.82.xx. A customs broker or a refund specialist like Price Ridge can pull and interpret this documentation for you.