That's the legal victory. Here's the catch: refunds are not automatic. Every importer must proactively file a CAPE Declaration through CBP's refund system to recover what they paid — and the processing queue fills on a first-come, first-served basis.

This article breaks down the ruling, what it means for your refund eligibility, how the CBP CAPE system works, and what importers must do now.

Key Takeaways

- The Supreme Court ruled 6-3 that IEEPA does not authorize the President to impose tariffs, invalidating billions in duties collected since 2025.

- Refunds are not automatic — importers must file a CAPE Declaration through CBP's ACE Secure Data Portal.

- Eligible duties include IEEPA tariffs on imports from China, Canada, Mexico, and the Liberation Day reciprocal tariffs.

- Section 232 and Section 301 duties are not refundable under this ruling.

- File early — CBP processes refunds in queue order, and statutes of limitations apply to some entries.

Background: IEEPA and How It Was Used to Impose Tariffs

The International Emergency Economic Powers Act (IEEPA), codified at 50 U.S.C. § 1702, grants the President broad authority to regulate economic transactions during declared national emergencies. Its text authorizes the President to "regulate importation" — but notably contains no reference to tariffs or duties.

No president had ever used IEEPA to impose tariffs — until February 2025. That silence on tariffs in the statute's text became the centerpiece of the legal challenge that followed.

The Tariff Timeline

The Trump administration issued three executive orders on February 1, 2025, invoking IEEPA to impose tariffs framed as responses to fentanyl trafficking:

- Canada — 25% ad valorem (10% on energy products), effective February 4, 2025

- Mexico — 25% ad valorem, effective February 4, 2025

- China — 10% additional ad valorem, effective February 4, 2025

Then on April 2, 2025, Executive Order 14257 imposed sweeping "Liberation Day" reciprocal tariffs on imports from dozens of countries, with a 10% baseline rate taking effect April 5 and country-specific rates effective April 9.

Together, these orders placed billions of dollars in new import costs on U.S. businesses — costs that importers, not foreign exporters, absorb at the border.

The Legal Challenge

Small businesses — including educational toy company Learning Resources, Inc. — filed suit arguing that IEEPA's "regulate importation" language does not include the power to impose taxes. Congress, they argued, never explicitly delegated tariff authority through IEEPA. The cases were consolidated and expedited to the Supreme Court.

The Supreme Court's 6-3 Ruling: What the Court Actually Decided

The Supreme Court's opinion in Learning Resources, Inc. v. Trump, No. 24-1287, decided February 20, 2026, held unambiguously: IEEPA does not authorize the President to impose tariffs.

The Core Holding

Chief Justice Roberts, writing for the majority, found that "regulate importation" does not encompass the power to impose taxes. The statute contains no reference to tariffs or duties — and as the opinion states, the government's argument "cannot bear the weight the Government places on it."

How the Justices Aligned

| Justice(s) | Position |

|---|---|

| Roberts, Sotomayor, Kagan, Gorsuch, Barrett, Jackson | 6-justice majority — IEEPA does not authorize tariffs |

| Roberts, Gorsuch, Barrett | Plurality — also applied the Major Questions Doctrine |

| Kagan, Sotomayor, Jackson | Joined the holding; rejected Major Questions framing as unnecessary |

| Kavanaugh, Thomas, Alito | Dissent — argued IEEPA text conferred tariff authority |

The Major Questions Doctrine plurality (Roberts, Gorsuch, Barrett) held that when the executive claims authority over matters of "vast economic and political significance" — like imposing unlimited tariffs — Congress must speak clearly. IEEPA's language fell far short.

What the Ruling Does NOT Address

The Court vacated and remanded one case and affirmed the other but did not prescribe refund mechanics. It left the implementation entirely to lower courts and CBP. That gap is where the real work for importers begins.

The Post-Ruling Sequence

The three key dates that define what happens to your money:

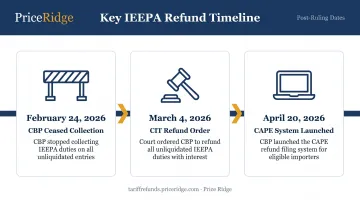

- February 24, 2026 — CBP ceased collecting IEEPA duties per CSMS #67834313

- March 4, 2026 — Judge Richard K. Eaton (Court of International Trade) ordered CBP to refund all unliquidated IEEPA duties with interest, extending relief to all importers — not just named plaintiffs

- April 20, 2026 — CBP launched the CAPE (Consolidated Administration and Processing of Entries) system for refund filings

The Refund Opportunity: Stakes, Eligibility, and Urgency

Estimated IEEPA duties collected range from $166 billion to over $175 billion, paid by more than 330,000 importers across more than 53 million entries. For most importers, this represents a potential recovery of 100% of IEEPA duties paid, plus interest.

Who Qualifies

Eligible for refund:

- IEEPA fentanyl tariffs on Canada, Mexico, and China (February 2025 executive orders)

- Liberation Day reciprocal tariffs (April 2025 executive orders)

Not eligible — unaffected by this ruling:

- Section 232 steel, aluminum, and copper tariffs

- Section 301 China tariffs (the original 2018+ trade war duties)

- Standard MFN duties

The distinction matters on individual entries. Many China-origin shipments carry Section 301 duties (HTS 9903.88.xx) alongside IEEPA duties (HTS 9903.01.25) — only the IEEPA component is refundable.

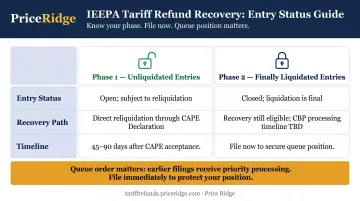

Liquidated vs. Unliquidated Entries

Liquidation is CBP's final accounting determination on an entry, typically occurring on a 314-day liquidation cycle. The status of your entries affects your recovery path:

| Entry Status | Recovery Path | Timeline |

|---|---|---|

| Unliquidated (Phase 1) | Reliquidated directly through CAPE Declaration | 45–90 days after CAPE acceptance |

| Finally liquidated (Phase 2) | Still eligible; CBP processing timeline TBD | File now to secure queue position |

The Pass-Through Complication

Many importers passed tariff costs to customers via surcharges. Whether those importers retain the refund right — or whether downstream customers who bore the economic burden have a claim — remains contested. Consumer class-action lawsuits have already been filed against companies including FedEx, Costco, and UPS, per Bloomberg Law reporting from March 2026.

If you passed tariff costs through to customers, document how you handled them and consult counsel before filing.

Why Speed Matters

- Queue position is first-come, first-served — CBP processes CAPE Declarations strictly in order received

- Over 26,000 importers had already registered by late March 2026

- More than 2,000 tariff-related lawsuits were filed by early March 2026

- Statutes of limitations apply — for finally liquidated entries, importers generally have 180 days to file a protest after a reliquidation notice is issued

The CBP CAPE System: How to File for Your Refund

CBP's CAPE (Consolidated Administration and Processing of Entries) system launched April 20, 2026. Without it, CBP estimated processing refunds manually would require approximately 4.4 million labor hours for 330,000+ importers across 53 million entries.

CAPE consolidates all refund amounts and applicable interest into a single payment per importer, issued in phases. CBP does not charge fees for processing. Once a CAPE Declaration is accepted, CBP generally issues valid refunds within 60–90 days.

What Filing Requires

The CAPE Declaration is a CSV-format file submitted through the CAPE tab in CBP's ACE Secure Data Portal. Each row represents one CF7501 entry summary and must include:

- Entry number and port code

- Importer of Record (IOR) number

- Total entered value

- IEEPA duty amount

- HTS subheading (e.g., 9903.01.25)

- Country of origin

CBP's schema is strict. A single error — wrong column order, incorrect date format, mismatched HTS code, wrong phase classification — causes CBP to reject the entire filing and return the importer to the back of the queue.

Common Filing Errors to Avoid

- Including Section 301 or Section 232 duty amounts in the IEEPA refund calculation

- Misclassifying finally liquidated entries as Phase 1 (unliquidated)

- IOR number in the CSV not matching Box 22 of the CF7501

- Missing CF28/CF29 responses after filing (causes individual entries to be dropped from the refund)

Where Price Ridge Fits

Most U.S. importers — especially small and mid-size businesses — don't have in-house customs counsel or the technical expertise to navigate CAPE filings independently. Customs attorneys typically charge $400–$800 per hour and often won't take smaller claims on contingency. Customs brokers handle entry filing — not refund claim management.

Price Ridge handles the entire CAPE process end-to-end for importers without that in-house capacity:

- Free eligibility review — confirms whether you qualify and estimates your refund amount

- Document collection — coordinates directly with your customs broker to retrieve CF7501 entry summaries, duty payment records, and supporting documents

- CAPE Declaration preparation — builds the CSV in CBP's exact required format, validated line by line before submission

- ACE Portal submission — filed through licensed customs broker partners with established ACE credentials (you don't need your own ACE account)

- Claim tracking — monitors queue position, CBP validation status, and reliquidation actions throughout

- CBP liaison — responds to all CF28 and CF29 agency requests within required deadlines

- Disbursement coordination — reconciles the final refund amount and remits your share

Price Ridge offers three ways to work together, depending on your timeline and cash needs:

- Contingency filing — $0 upfront; Price Ridge takes 15–30% only when CBP disburses your refund

- Outright claim purchase — for claims of $500,000+, Price Ridge buys your refund right at 75–85 cents on the dollar and wires payment within weeks

- Claim financing — a 60–80% cash advance against your pending refund, repaid when CBP disburses

Reach Price Ridge at refunds@priceridge.com for a free eligibility review — response within one business day.

Tariffs Going Forward: What's Still in Play

The Learning Resources ruling eliminates IEEPA as a tariff authority. It does not eliminate tariffs.

The administration moved immediately. On February 24, 2026 — the same day IEEPA collection ceased — a 10% global import surcharge took effect under Section 122 of the Trade Act of 1974 (Proclamation 11012).

However, on May 7, 2026, the Court of International Trade invalidated those Section 122 tariffs. The government appealed, and the tariffs were set to expire around late July 2026 absent Congressional extension.

The Three Alternative Tariff Authorities

Section 232 (National Security) — Already in use for steel, aluminum, and copper. Requires a Commerce Department assessment. Unaffected by Learning Resources and actively expanding.

Section 301 (Unfair Trade Practices) — USTR initiated Section 301 investigations on March 11, 2026, published in the Federal Register on March 17, 2026, targeting 16 economies including China, the EU, Vietnam, India, Mexico, Japan, Taiwan, and others for structural excess manufacturing capacity. These investigations can produce new tariffs — potentially significant ones.

Section 122 (Balance of Payments) — Limited to 15% ad valorem for a maximum of 150 days without Congressional approval. Currently under legal challenge.

The practical implication: your IEEPA tariff burden is refundable, but your overall tariff environment has not returned to a pre-2025 baseline. Section 232 and Section 301 remain live — and Section 301 investigations targeting 16 economies are actively building toward new tariff actions. Recovering what you're owed on IEEPA is one step; tracking what comes next is another.

Frequently Asked Questions

Who wrote the majority opinion in Learning Resources v. Trump?

Chief Justice John Roberts authored the controlling opinion, joined by Justices Sotomayor, Kagan, Gorsuch, Barrett, and Jackson in a 6-3 majority. Roberts also wrote a separate plurality section applying the Major Questions Doctrine, joined only by Gorsuch and Barrett — the other three majority justices rejected that additional analysis as unnecessary.

Are all IEEPA tariffs eligible for refunds after the ruling?

Tariffs imposed under IEEPA — including the fentanyl tariffs on Canada, Mexico, and China, and the Liberation Day reciprocal tariffs — are eligible for refund. Section 232 tariffs on steel, aluminum, and copper and Section 301 China tariffs are unaffected by this ruling and are not refundable under it.

How long will it take to receive an IEEPA tariff refund through the CAPE system?

CBP's CAPE system launched April 20, 2026. For Phase 1 (unliquidated) entries, CBP generally processes valid refunds within 60–90 days of CAPE Declaration acceptance. Phase 2 (finally liquidated) entries have no announced CBP processing timeline. Earlier filers secure a better queue position, so filing promptly matters.

What is a CAPE Declaration and do I need to file one to get my refund?

A CAPE Declaration is the formal filing required to initiate CBP's refund process. It is a CSV-format document submitted through the CAPE tab in CBP's ACE Secure Data Portal by importers or their authorized representatives, with supporting entry data. Refunds are not distributed automatically; action is required to receive anything.

Can importers who passed tariff costs to customers still file for refunds?

This is a contested legal question — consumer class actions against companies like FedEx and Costco are actively testing it. If you passed tariff costs downstream, document how you handled them and consult counsel before filing a CAPE Declaration.

Do any tariffs remain in place after the Learning Resources ruling?

Yes. Section 232 tariffs on steel, aluminum, and copper remain in force, as do existing Section 301 China tariffs. A 10% global replacement tariff under Section 122 is currently under legal challenge, and USTR's March 2026 Section 301 investigations may produce new tariffs on 16 trading partners. The ruling eliminated IEEPA tariffs only.