Introduction

On February 20, 2026, the Supreme Court issued one of the most consequential trade rulings in American history. In a 6-3 decision in Learning Resources, Inc. v. Trump, the Court held that the International Emergency Economic Powers Act (IEEPA) does not authorize the president to impose tariffs — invalidating billions of dollars in duties collected since 2025.

For U.S. importers, the ruling creates both an opportunity and a deadline problem. The CBO estimates roughly $150 billion in IEEPA duties were collected before termination. That money is refundable — but the process is not automatic, deadlines are already running, and replacement tariffs are in place.

This article covers what the ruling actually means, which tariffs were struck down, what tariffs remain, and exactly how to file for your refund before the window closes.

Key Takeaways

- The Supreme Court ruled 6-3 that IEEPA does not grant the executive power to impose tariffs — that authority belongs exclusively to Congress

- All IEEPA-based tariffs ceased collection at 12:00 a.m. ET on February 24, 2026, per CBP guidance

- Refunds are not automatic — importers must file actively through CBP's CAPE system, subject to strict deadlines

- Section 232 (steel, aluminum, autos), Section 301 (China goods), and a new Section 122 replacement tariff all remain in effect

- The 180-day protest deadline for liquidated entries is a hard cutoff; missing it forfeits your claim permanently

What the Supreme Court Actually Ruled — and Why

The Constitutional Foundation

Article I of the U.S. Constitution grants Congress — not the president — the exclusive power to "lay and collect Taxes, Duties, Imposts and Excises." The government conceded at oral argument that the president has no inherent Article II tariff authority. Any tariff power must come from a clear act of Congress.

The central question: does IEEPA's grant of power to "regulate... importation" include the power to impose tariffs?

Chief Justice Roberts, writing for the majority, said no. His reasoning focused on three points:

- Text: IEEPA contains no reference to "tariffs," "duties," or "taxes" — the words Congress uses when it actually means to grant taxing authority

- History: In nearly 50 years of IEEPA's existence, no prior president had read the statute to authorize tariffs

- Stakes: The trillions in trade affected here "dwarf" those of all prior major questions cases

The Major Questions Doctrine

Roberts, joined by Gorsuch and Barrett, applied the major questions doctrine — a principle requiring Congress to speak clearly when it delegates authority over matters of vast economic or political significance. The logic: courts won't assume Congress handed the executive branch sweeping power through vague or general statutory language.

Tariff authority hits this threshold on both counts. It touches a core constitutional power (taxation) and affects trillions in trade. Under that framework, IEEPA's broad "regulate" language simply isn't enough. Congress would need to have explicitly said "tariffs" — and it didn't.

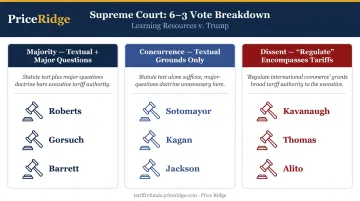

The Vote Breakdown

The 6-3 vote reflected this doctrinal split across the Court.

| Justices | Position |

|---|---|

| Roberts, Gorsuch, Barrett | Majority — textual + major questions doctrine |

| Sotomayor, Kagan, Jackson | Concurred on textual grounds; did not invoke major questions doctrine |

| Kavanaugh, Thomas, Alito | Dissented — argued "regulate" historically encompasses tariffs |

Justice Kavanaugh's dissent flagged the practical consequences directly: the ruling could require the federal government to refund billions in collected duties and introduce uncertainty into trade arrangements with countries from China to the UK to Japan.

Which IEEPA Tariffs Were Struck Down

Following the ruling, the Trump administration issued an executive order terminating IEEPA tariff collection. Per CBP guidance (CSMS #67834313), collection stopped for goods entered or withdrawn from warehouse on or after 12:00 a.m. ET, February 24, 2026.

Terminated programs include:

- Global reciprocal tariffs: minimum 10%, up to 41%, on nearly all trading partners (EO 14257 and subsequent modifications)

- China trafficking tariff: 10% additional ad valorem

- Mexico trafficking tariff: 25% additional ad valorem

- Canada trafficking tariffs: 25% general rate; 10% on energy and minerals

- Brazil additional duties: 40% on certain Brazilian products

- India additional duties: 25% additional rate (the India rate was modified before the ruling — confirm scope for each entry separately)

Two things to know about what the ruling did NOT cover:

- De minimis suspension remains in effect — the $800 threshold exemption stays suspended under a separate executive order (EO 14388, issued February 20, 2026)

- Collection didn't stop automatically — a separate executive order and CBP guidance were required before duty collection actually ceased

What Tariffs Are Still in Effect After the Ruling

The ruling is narrowly limited to IEEPA-based tariffs. A significant tariff structure remains in place.

Section 232 National Security Tariffs

These were not challenged and are fully in effect:

- Steel, aluminum, and copper — adjusted to 50% under a June 2026 presidential action

- Automobiles and parts — 25% duties remain

- Lumber and timber — 25% on covered derivative products

- Semiconductors — Section 232 action is in place; rate subject to ongoing modification

Section 301 China Tariffs

Section 301 tariffs on Chinese goods are unaffected by the ruling. Key rates include 100% on electric vehicles, 50% on semiconductors, and 50% on solar cells. The administration launched new Section 301 investigations in March 2026 to build additional tariff authority beyond IEEPA.

That ongoing Section 301 authority matters because the administration moved quickly to fill the gap left by the ruling.

Section 122 Replacement Tariff

Within hours of the ruling, the administration issued Proclamation 11012 imposing a 10% global import surcharge under Section 122 of the Trade Act of 1974, effective February 24, 2026, for 150 days (through approximately July 24, 2026). The statute caps such surcharges at 15% and 150 days unless Congress extends them.

Section 122 carveouts include: energy products, pharmaceuticals, certain electronics, USMCA-compliant Canadian and Mexican goods, and goods already subject to Section 232 restrictions.

Important update: The Court of International Trade struck down the Section 122 surcharge on May 7, 2026 (CIT Slip Op. 26-47). That decision is under appeal, so the practical status remains in flux. Importers should monitor developments closely.

Are Importers Entitled to IEEPA Tariff Refunds?

The Legal Entitlement Is Clear

Because the Court ruled IEEPA never authorized tariffs, all IEEPA duties paid are subject to reimbursement. The Court of International Trade has affirmed it has the power to order reliquidation and refunds where the government unlawfully collected duties. The obstacle is not entitlement — it's process and timing.

The Two Refund Pathways

Pathway 1 — Post Summary Correction (PSC) — Context Only: PSCs can remove duties before liquidation finalizes, but CBP has since clarified that importers cannot use PSCs to initiate IEEPA duty refunds. This pathway is no longer operative for IEEPA claims. All IEEPA refund claims should go through the CAPE Declaration process described below.

Pathway 2 — CAPE Declaration for all IEEPA refund claims: CBP created the CAPE (Consolidated Administration and Processing of Entries) system specifically for IEEPA refund claims. Phase 1 launched April 20, 2026, covering unliquidated and recently liquidated entries. Valid refunds generally issue within 60-90 days of CAPE Declaration acceptance.

The Protest Deadline for Liquidated Entries

For entries that have already been finally liquidated, importers must act within the 19 U.S.C. § 1514 framework. The 180-day protest deadline from the date of liquidation is a hard cutoff with no exceptions.

Consider the math: an entry that liquidated on August 15, 2025 had a protest deadline of February 11, 2026, before the Supreme Court even ruled. Importers with 2025 entries should check their liquidation dates immediately.

The Scale of the Claims and Refund Delays

The dollar figures at stake are substantial:

- Penn Wharton analysis via Reuters: $175 billion+ potentially subject to refund

- CBO estimate: roughly $150 billion collected

- BEA estimate: approximately $166 billion in federal refund obligation, excluding interest

That volume virtually guarantees delays. With over 26,000 importers already registered in the CAPE queue as of late March 2026, processing is sequential: early filers get processed first. The government has also appealed the CIT's nationwide refund order, with Bloomberg reporting $11.4 billion tied up in that appeal.

One additional complication: refunds interact with transfer pricing, cost allocation between affiliated entities, and how tariff costs were passed through to customers. Both customs counsel and tax advisors should be involved before filing.

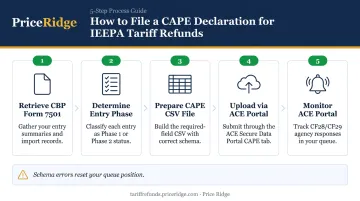

How to Claim Your IEEPA Tariff Refund

Step 1 — Retrieve and Organize Import Records

Pull all import records for entries subject to IEEPA tariffs:

- CBP Form 7501 (Entry Summaries) — the primary document recording duty amounts, entry numbers, HTS codes, and country of origin

- Duty payment records — broker invoices with line-item duty breakdowns

- Commercial invoices — with FOB or CIF values

- Packing lists and bills of lading

- Any prior CBP CF28 or CF29 correspondence

Work with your customs broker to pull this data. If records are unavailable (broker went out of business, switched brokers, records lost), CBP's ACE Importer Query module can retrieve them with a valid Power of Attorney.

Step 2 — Determine Entry Status (Phase 1 vs. Phase 2)

- Phase 1 covers unliquidated entries and entries liquidated within roughly 80 days of the CAPE launch. CBP processes these within 45-90 days of CAPE Declaration acceptance.

- Phase 2 covers finally liquidated entries — most 2025 and earlier IEEPA imports. CBP has no announced processing timeline for Phase 2, but filing now establishes your queue position before Phase 2 processing opens.

Many importers have both phases simultaneously and should file a consolidated declaration covering all eligible entries.

Step 3 — File Your CAPE Declaration

The CAPE Declaration is a CSV file uploaded through the CAPE tab in CBP's ACE Secure Data Portal. Each row represents one CF7501 entry summary. Required fields include:

- Entry number and port code

- Importer of Record (IOR) number

- Total entered value

- IEEPA duty amount

- HTS subheading (typically 9903.01.25 and related codes)

- Country of origin

CBP's CAPE schema is strict. Incorrect column order, date formatting errors, mismatched HTS codes, or a missing IOR number will reject the entire filing — placing you at the back of a queue with 26,000+ filers ahead of you.

Step 4 — Monitor and Respond to CBP

After filing, CBP may issue CF28 (Request for Information) or CF29 (Notice of Action) on individual entries. Missing these responses causes affected entries to be dropped from the claim — a direct financial loss. Ongoing monitoring through the ACE portal is essential throughout the life of the claim.

Step 5 — Evaluate Your Options for Immediate Cash

CBP processing can take months. For importers who need capital now, three alternatives exist:

- Contingency filing: Price Ridge manages the entire CAPE process at no upfront cost. A percentage (typically 15-30%) is collected only when CBP disburses the refund. Minimum claim: $10,000 in IEEPA duties paid.

- Outright claim purchase: For claims of $500,000+ in IEEPA duties paid, Price Ridge buys the refund claim at 75-85 cents on the dollar — immediate cash, no CBP wait. The importer permanently assigns the refund right; Price Ridge handles all filing and recovery.

- Claim financing: A cash advance of 60-80% of estimated refund value, repaid from CBP disbursement when received. The importer retains the claim and keeps any upside above the advance.

Price Ridge was built for importers who paid IEEPA tariffs but lack in-house customs expertise. The firm manages every step from eligibility review through final disbursement coordination. Request a free eligibility review at refunds@priceridge.com — response within one business day.

Action Checklist

- Identify all IEEPA-tariff-bearing entries and confirm you were the Importer of Record on each

- Check liquidation status for every entry and calculate remaining protest/filing deadlines

- Separate IEEPA duties from non-refundable Section 301, Section 232, and MFN duties (critical for China-origin imports)

- File your CAPE Declaration — or engage a service to file on your behalf — immediately

- Evaluate whether the immediate cash option (claim purchase or financing) makes more sense than waiting for CBP processing

- Consult tax advisors about how refunds will be treated in your general ledger

Frequently Asked Questions

Have Trump's reciprocal tariffs been struck down?

Yes. The Supreme Court struck down all IEEPA-based reciprocal tariffs on February 20, 2026, and CBP ceased collecting them for goods entered on or after February 24, 2026. However, a 10% replacement surcharge under Section 122 was imposed the same day — though that surcharge has since been challenged and struck down by the Court of International Trade, with the appeal ongoing.

Are all Trump tariffs gone after the Supreme Court ruling?

No. Only IEEPA-based tariffs were invalidated. Section 232 tariffs on steel (50%), aluminum (50%), automobiles (25%), and lumber (25%) remain fully in place, as do Section 301 tariffs on Chinese goods — including 100% on EVs and 50% on semiconductors and solar cells.

What is IEEPA and why did the court rule against it?

IEEPA is a 1977 emergency powers law (50 U.S.C. § 1701 et seq.) that lets the president "regulate" commerce during declared national security emergencies. The Court ruled that "regulate" does not include the power to impose tariffs, duties, or taxes — a power the Constitution assigns exclusively to Congress — and that Congress never clearly delegated tariff authority through IEEPA's language.

How do I get a refund for IEEPA tariffs I already paid?

Refunds require active filing through CBP's CAPE Declaration system — nothing is automatic. Unliquidated entries fall under Phase 1 (60-90 day processing window); finally liquidated entries fall under Phase 2 (no announced timeline). File now rather than waiting for CBP to act on your behalf.

What is the deadline to file for an IEEPA tariff refund?

For finally liquidated entries, the deadline runs from the date of liquidation — entries that liquidated in mid-2025 may already be approaching or past the 180-day protest window under 19 U.S.C. § 1514. Check your liquidation dates immediately. CBP also processes CAPE claims in queue order, so delay costs you position.

What happens to trade deals Trump negotiated using IEEPA tariffs as leverage?

The administration is now relying on Section 301 investigations as its primary negotiating tool — USTR issued findings in June 2026 across 60 investigations. Most trading partners are watching how those proceedings develop before committing to new terms, since the IEEPA-based leverage those earlier deals depended on no longer exists.