Key Takeaways

- Trump imposed IEEPA-based tariffs starting February 1, 2025, covering imports from Canada, Mexico, China, and eventually most US trading partners

- The Supreme Court ruled 6-3 on February 20, 2026 that IEEPA does not authorize tariffs — invalidating all of them from the start

- CBP stopped collecting IEEPA duties effective February 24, 2026

- Over $170 billion in IEEPA duties were collected — refunds are available but require active filing

- Filing deadlines are already running — importers who miss them forfeit their refunds

What Is IEEPA and Why Did Trump Use It for Tariffs?

The International Emergency Economic Powers Act, enacted in 1977, gives presidents authority to freeze assets, restrict transactions, and impose economic sanctions during declared national emergencies. Before 2025, it had been used against adversaries like Iran, Russia, and North Korea — but never to impose broad import tariffs. The closest historical precedent was Nixon's 1971 use of the Trading with the Enemy Act for a 10% import surcharge, a different statute entirely.

The Trump administration's legal theory rested on IEEPA's language authorizing the President to "regulate the importation" of goods. The argument: that phrase is broad enough to encompass tariffs, allowing the White House to move from emergency declaration to tariff imposition in days rather than the years required under Section 301 or Section 232 investigations.

That legal theory ran into an immediate constitutional problem. Article I, Section 8 of the Constitution assigns Congress — not the President — the exclusive power to "lay and collect Taxes, Duties, Imposts and Excises." Using IEEPA as a tariff vehicle was a direct separation-of-powers challenge from the outset.

The Scope of Trump's 2025 IEEPA Tariffs

The Timeline of Orders

| Executive Order | Date | Target | Rate |

|---|---|---|---|

| EO 14193 | Feb. 1, 2025 | Canada | 25% most goods; 10% energy |

| EO 14194 | Feb. 1, 2025 | Mexico | 25% |

| EO 14195 | Feb. 1, 2025 | China | 10% (raised to 20% in March) |

| EO 14245 | Mar. 24, 2025 | Countries importing Venezuelan oil | 25% |

| EO 14257 | Apr. 2, 2025 | All trading partners | 10% baseline; higher for designated countries |

| EO 14323 | Jul. 30, 2025 | Brazil | 40% additional |

| EO 14329 | Aug. 6, 2025 | India | 25% additional |

The April 2 "Liberation Day" order set a 10% global baseline, with Annex I rates reaching 41% (Falkland Islands, Syria), 46% (Vietnam), 49% (Cambodia), and 50% (Lesotho) for designated countries. Those rates landed on top of existing duties — meaning importers in certain sectors absorbed compounding cost increases almost overnight.

Who Got Hit Hardest

Any product imported from a covered country faced IEEPA tariffs stacked on top of existing duties. The hardest-hit sectors:

- Electronics and technology

- Apparel and textiles

- Automotive parts

- Industrial machinery and equipment

- Consumer goods

- Chemicals and construction materials

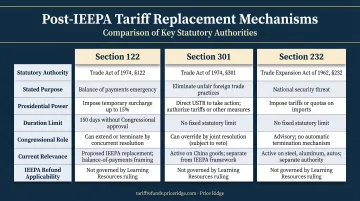

What IEEPA Did NOT Cover

Three separate tariff regimes remained fully in effect throughout — completely unaffected by the IEEPA ruling:

- Section 301 tariffs on goods from China and Nicaragua, imposed under separate statutory authority

- Section 232 tariffs on steel, aluminum, automobiles, copper, timber, and semiconductors

- De minimis suspension for shipments under $800, which continues under a separately issued executive order

The Legal Journey: From Lawsuits to Supreme Court Decision

Early Challenges and the CIT Ruling

Legal challenges began within weeks of the February 2025 orders. Businesses, trade associations, and state governments filed suits in the Court of International Trade and other federal courts. The core arguments:

- Trade deficits and drug trafficking don't constitute the "unusual and extraordinary" foreign threats IEEPA requires

- Tariffs are taxes, and only Congress can impose taxes under Article I

- Even if an emergency existed, the tariff remedy was disproportionate

The CIT agreed. In Slip Op. 25-66 on May 28, 2025, the court vacated the challenged tariff orders and entered a nationwide permanent injunction — explicitly affirming its power to order reliquidation and refunds for unlawfully collected duties.

The Supreme Court's Decision

The Supreme Court granted certiorari before judgment on September 9, 2025, consolidating the cases as Learning Resources, Inc. v. Trump (No. 24-1287) with Trump v. V.O.S. Selections (No. 25-250). Oral arguments were held November 5, 2025.

On February 20, 2026, a 6-3 majority held that IEEPA does not authorize tariffs. Chief Justice Roberts wrote for the majority (joined by Sotomayor, Kagan, Gorsuch, Barrett, and Jackson). Kavanaugh dissented, joined by Thomas and Alito.

The key holding: authority to "regulate importation" does not include authority to impose tariffs. As Roberts wrote, "The Government points to no statute in which Congress used the word 'regulate' to authorize taxation." Tariff authority of this economic magnitude requires explicit Congressional delegation, and IEEPA provides none — making all IEEPA-based tariffs invalid from inception.

The Court deliberately left one question unresolved: the mechanics of refunding previously collected duties. That issue was remanded to the CIT and CBP. Importers have an established legal right to refunds, but collecting them requires a separate claims process — one that CBP is still administering through its CAPE Declaration system.

What Happened After the Ruling

On the same day as the ruling, President Trump signed Executive Order 14389, terminating all additional ad valorem duties imposed under IEEPA — covering EOs 14193, 14194, 14195, 14245, 14257, 14323, 14329, and the Cuba and Iran orders. CBP issued CSMS #67834313 on February 22, halting IEEPA duty collection for entries on or after 12:00 a.m. ET, February 24, 2026.

To replace lost revenue, Trump invoked Section 122 of the Trade Act of 1974 the same day, imposing a temporary 10% import surcharge effective February 24 through July 24, 2026. Section 122 caps such surcharges at 15% and limits them to 150 days without Congressional extension.

Other legal mechanisms — Section 338 of the Tariff Act of 1930 (up to 50% on discriminatory trading partners) and traditional Section 301/232 processes — are still available, but each requires a separate formal investigation to invoke.

The court ruling also created fallout beyond domestic tariff policy. Bilateral trade agreements negotiated around IEEPA tariff rates (the Agreements on Reciprocal Trade) are now in legal limbo: their tariff-rate ceilings no longer rest on a valid IEEPA foundation.

What the IEEPA Ruling Means for Importers: The Refund Opportunity

Who Qualifies

Refunds go to the importer of record — the entity that actually paid IEEPA duties to CBP at the time of import. Third parties (buyers, contract manufacturers) who reimbursed an importer for tariff costs cannot file directly with CBP; they must look to their contracts with the importer.

The first step is auditing which entries carried IEEPA tariffs, the amounts paid, and whether those entries are liquidated or unliquidated. That status determines your filing pathway.

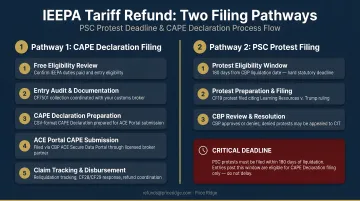

The Two Filing Pathways

- Post-Summary Corrections (PSCs): For entries not yet formally liquidated by CBP. Entries typically liquidate 314 days after filing, so recently filed entries may still be in this window.

- Formal protests: For already-liquidated entries. Protests must be filed within 180 days of the liquidation date under 19 U.S.C. 1514 — meaning some entries may already be approaching their deadline.

CBP launched the CAPE (Customs Automated Processing Engine) Declaration system to consolidate IEEPA refunds. CBP processes CAPE Declarations in order of receipt, with Phase 1 claims (unliquidated entries) targeted for processing within 45 days of acceptance.

Phase 2 (finally liquidated entries) has no announced timeline. Some importers are also filing directly at the CIT, believing litigation may move faster than the administrative queue.

Why Timing Matters

- Protest deadlines run from each entry's liquidation date — some are already close to expiring

- CBP processes claims in queue order — with over 26,000 importers of record already registered as of late March 2026, early filing directly affects when you get paid

- With estimates of ~$175 billion in potential refunds, processing delays of months to years are realistic — Congress is also scrutinizing the total refund liability

Where Price Ridge Fits

Most importers don't have dedicated customs compliance staff who know how to file CAPE Declarations, distinguish IEEPA from Section 301/232 duties in entry documentation, or coordinate with brokers to retrieve CF7501 forms. That gap is exactly what Price Ridge addresses. The service covers:

- Free eligibility review with a response within one business day, no obligation

- Coordinates directly with your customs broker to gather CF7501 entry summaries, duty payment records, and commercial invoices

- Prepares and files your CAPE Declaration within days of receiving documents

- Tracks the claim through CBP review and reliquidation, handling any agency inquiries

- Manages receipt and remittance of your refund share at disbursement

For importers who can't wait for CBP's processing timeline, Price Ridge also purchases refund claims outright at 75–85 cents on the dollar — immediate cash rather than a position in a multi-year queue.

The minimum threshold is $10,000 in IEEPA duties paid. Contact Price Ridge at refunds@priceridge.com to start a no-obligation eligibility review.

Frequently Asked Questions

When did Trump impose tariffs under IEEPA?

Trump began imposing IEEPA tariffs on February 1, 2025 with executive orders targeting Canada, Mexico, and China, followed by a global reciprocal tariff order on April 2, 2025. Additional country-specific orders targeting Brazil and India followed through mid-2025, before the Supreme Court struck them all down on February 20, 2026.

What were the main IEEPA tariff rates?

Rates included 25% on most Canadian and Mexican imports (10% for Canadian energy), 10–20% on Chinese goods, a global baseline of 10% with select countries reaching 50%, plus 40% on Brazil and 25% on India. All were layered on top of existing Section 301 and 232 duties.

What happened to Trump's IEEPA tariffs?

The Supreme Court ruled 6-3 on February 20, 2026 that IEEPA does not authorize tariffs. Trump signed EO 14389 terminating all IEEPA duties the same day. CBP stopped collecting them effective February 24, 2026. The question of refunds for previously paid duties was remanded to the CIT and CBP.

How much revenue did IEEPA tariffs generate?

PwC reported over $170 billion in IEEPA-related tariff revenue collected; Cato estimated approximately $175 billion owed as refunds as of February 2026. No official Treasury or CBP aggregate figure has been published, and the scale of potential refunds means processing is expected to be slow and subject to Congressional scrutiny.

Who is eligible to receive an IEEPA tariff refund?

The importer of record — the company that paid duties directly to CBP at the time of import — is entitled to refunds. Third parties who reimbursed importers for tariff costs must look to their contracts with the importer; they cannot file directly with CBP.

How long will it take to receive a refund?

CBP targets 45 days for Phase 1 claims after CAPE acceptance, but Phase 2 has no announced schedule. Given the volume of claims and likely Congressional involvement, delays of months to years are realistic — filing early secures your position in the processing queue.