For U.S. importers, this isn't just a constitutional headline. The Penn Wharton Budget Model estimated up to $175 billion in potential refunds from reversed IEEPA tariffs — meaning many companies that paid these duties between 2025 and 2026 may be entitled to significant cash recoveries.

The catch: refunds don't happen automatically. There are procedural deadlines, a finite processing queue, and real consequences for waiting.

This article covers what the Court decided, which tariffs were struck down, how large the refund opportunity is, how the recovery process works, and what you should do right now.

TL;DR: Key Takeaways

- The Supreme Court ruled 6-3 that IEEPA does not grant presidential tariff authority, citing the Constitution's Taxing Clause and the Major Questions Doctrine

- All IEEPA-based tariffs ceased collection on February 24, 2026 following EO 14389

- Importers can recover paid duties; refunds require a filed claim and are not issued automatically

- The 180-day protest deadline for finally liquidated entries is a hard cutoff — confirm your entry's liquidation date and act before the window closes

- Section 232 and Section 301 tariffs are unaffected — do not confuse these with IEEPA duties

- CBP processes CAPE Declarations in order received, so earlier filing means an earlier position in the queue

What the Supreme Court Decided

The Constitutional Question

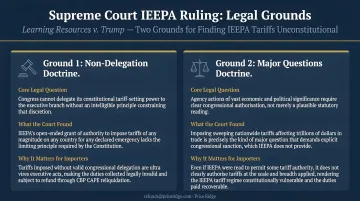

The Taxing Clause of Article I assigns Congress — not the executive branch — the power to impose duties and tariffs. The President has no inherent tariff authority and can only act through explicit congressional delegation. The question in Learning Resources was whether IEEPA provided that delegation.

The Court said no, on two grounds:

- Major Questions Doctrine: An authority of this "vast economic and political significance" requires clear congressional authorization. IEEPA contains no such clear grant.

- Statutory Text: IEEPA's authorization to "regulate…importation" does not encompass the power to tax or impose tariffs. Regulating commerce and levying revenue are legally distinct functions.

The Historical Context

The Court placed significant weight on one fact: in IEEPA's roughly 50-year history since its 1977 enactment, no President prior to Trump had ever invoked the statute to impose tariffs. The Congressional Research Service has confirmed this, and the Court treated that unbroken record as meaningful evidence that Congress never intended to grant such power.

The Dissent

Justices Kavanaugh, Thomas, and Alito dissented, arguing that "regulate importation" could reasonably include tariffs and that the Major Questions Doctrine should not apply so strictly in emergency or foreign-affairs contexts. The 6–3 split suggests the core holding is durable, though the dissent's foreign-affairs argument may resurface in future challenges.

What the Ruling Did Not Decide

Winning on the merits doesn't automatically put money back in importers' pockets. The Court left two critical questions open:

- No refund mechanism prescribed: CBP is not required to automatically issue refunds.

- Remanded to lower courts: Refund procedures go back to the Court of International Trade, meaning importers must take affirmative steps to recover what they paid.

Which Tariffs Were Struck Down — and Which Still Apply

Tariffs Terminated by EO 14389

Executive Order 14389, signed February 20, 2026, terminated the following IEEPA-based tariff actions:

| Tariff Action | Rate |

|---|---|

| China synthetic-opioid / fentanyl tariff (EO 14195) | 10% |

| Canada northern border / drug-trafficking tariff (EO 14193, amended) | Up to 35% |

| Mexico southern border / drug-trafficking tariff (EO 14194) | 25% |

| Global reciprocal tariffs (EO 14257, modified by EO 14326) | 10%–41% |

| Brazil country-specific IEEPA tariff (EO 14323) | 40% |

| India/Russia-related IEEPA tariff (EO 14329) | 25% |

While the plaintiffs only challenged certain tariffs, the Trump administration chose to terminate all listed IEEPA tariff actions in EO 14389 — extending the ruling's practical reach beyond the original case.

Tariffs That Remain in Effect

The following are entirely unaffected by the Learning Resources ruling:

- Section 232 tariffs — steel, aluminum, autos, copper, lumber, semiconductors

- Section 301 tariffs — existing China and Nicaragua actions

CBP's CSMS #67834313 confirmed that the termination applied to IEEPA duties only. Don't mix up these programs when assessing refund eligibility.

The Refund Opportunity: Scale and Eligibility

How Big Is This?

The Penn Wharton Budget Model projected up to $175 billion in potential refunds from reversing IEEPA tariffs. For individual importers, the stakes vary considerably:

- Retailers and e-commerce sellers with moderate import volumes can recover tens of thousands of dollars

- Industrial and equipment importers handling high-value goods can see six-figure recoveries from a single shipment's worth of entries

The minimum threshold for a recoverable claim worth pursuing is $10,000 or more in IEEPA duties paid.

Unliquidated vs. Finally Liquidated Entries

Your entries fall into one of two categories, and the pathway differs for each:

Unliquidated entries are those CBP has not yet finalized. The recovery path is more straightforward — a Post-Summary Correction (PSC) filed within 300 days from entry and at least 15 days before scheduled liquidation, whichever comes first.

Finally liquidated entries have a finalized duty assessment and require a formal protest filed within 180 days of liquidation. That deadline is absolute. If your entries liquidated between August and October 2025, you may already be approaching — or past — your window.

Why You Cannot Wait

The 180-day protest clock does not pause, and CBP's CAPE system processes declarations in the order received. Over 26,000 importers of record have already been identified as eligible — the queue grows daily. Every week of delay means a longer wait for processing and, for finally liquidated entries, real risk of missing the deadline entirely.

How the IEEPA Tariff Refund Process Works

Two Pathways, One Queue

For finally liquidated entries: File a protest under 19 U.S.C. § 1514 within 180 days of liquidation. This formally disputes the duty assessment and is the standard mechanism for recovering incorrectly assessed duties.

For unliquidated entries: File a Post-Summary Correction through CBP's ACE system. This corrects the duty amount before CBP finalizes the entry.

Both pathways feed into CBP's CAPE system — Consolidated Administration and Processing of Entries — which CBP launched in Phase 1 on April 20, 2026, to streamline IEEPA duty refunds including interest.

How CAPE Works

CAPE Declarations are filed through the ACE Secure Data Portal using a CSV file of entry numbers. Key mechanics:

- Each declaration is capped at 9,999 entries

- Declarations are processed in order of receipt

- Valid IEEPA refunds are generally issued within 60–90 days after CAPE Declaration acceptance, unless compliance review is needed

What Documentation You Need

To support a CAPE filing, importers typically need:

- CBP Form 7501 entry summaries

- Duty payment records

- Commercial invoices

- The IEEPA-specific HTSUS Chapter 99 line from each entry

Most importers don't have these documents on hand — they're held by customs brokers. Retrieving them is usually the first operational bottleneck, particularly for companies without in-house customs staff.

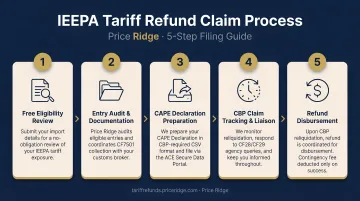

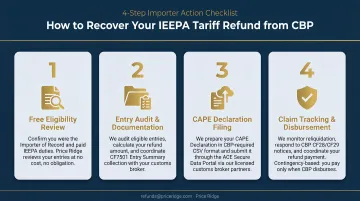

Where Price Ridge Fits

Most importers have a clear problem: they know they overpaid on IEEPA tariffs, but the CBP refund process — protests, CAPE Declarations, reliquidation — sits well outside normal business operations. Price Ridge handles that gap end-to-end.

The service covers the entire claim lifecycle:

- Eligibility review (free): Price Ridge analyzes your import history, identifies IEEPA-eligible entries, and calculates your refund amount — no obligation, response within one business day

- Document collection: Price Ridge coordinates directly with your customs broker to retrieve CF7501s, duty payment records, and commercial invoices; if you don't have a broker, Price Ridge can pull records through CBP importer query tools

- CAPE Declaration filing: Price Ridge prepares and submits your declaration within days of receiving documents, securing your position in the processing queue

- Claim tracking: Price Ridge monitors progress through CBP's review and reliquidation process, handling any agency inquiries on your behalf

- Disbursement coordination: Price Ridge manages the final payout and remits your share per the agreed fee arrangement

The fee structure matches the service model: contingency-based, with no upfront cost. Price Ridge's fee comes as a percentage of the recovered amount. For importers who need cash before CBP processing completes, Price Ridge also purchases claims outright at 75–85¢ on the dollar.

To start a free eligibility review, contact Price Ridge at refunds@priceridge.com.

What Replaces IEEPA Going Forward

The administration moved quickly after the ruling to maintain tariff coverage under different legal authorities.

New and Continuing Authorities

| Authority | Basis | Key Limitation |

|---|---|---|

| Section 122 | 19 U.S.C. § 2132 — balance-of-payments | 150-day maximum unless Congress extends |

| Section 301 | Unfair trade practices | New investigations announced by USTR post-ruling |

| Section 232 | National security | Already in effect; broad scope |

On February 20, 2026 — the same day as the ruling — President Trump issued a proclamation imposing a temporary import surcharge under Section 122. USTR also announced new Section 301 investigations targeting structural excess capacity in manufacturing sectors.

These replacement actions affect your forward-looking import costs, not your refund eligibility. Only IEEPA duties are within the refund scope.

Beyond refund eligibility, bilateral trade arrangements negotiated using IEEPA tariff leverage face a separate question. Those deals were explicitly tied to IEEPA executive orders — and without that legal foundation, courts may invalidate them or the administration may need to renegotiate their terms.

Action Steps for Importers Right Now

Move through these steps in order:

Pull your entry data — Retrieve entry summary data for the period February 2025 through February 24, 2026. Identify which lines carried IEEPA-specific Chapter 99 HTSUS codes. Separate these clearly from Section 232 and Section 301 lines.

Check liquidation status — Determine which entries are finally liquidated (180-day protest window running now) versus unliquidated (PSC pathway available). Entries with liquidation dates in August–October 2025 are the most time-sensitive category.

Assess your customs infrastructure — Do you have an existing customs broker with records on file? If not, document collection will require additional steps. Budget extra days for broker coordination if records aren't already consolidated.

Start the claim process — The CAPE queue is first-come, first-served. Filing early secures a better position in the processing queue. If navigating CBP's process without in-house customs expertise, consider working with a specialist rather than attempting the filing independently.

For importers with $10,000 or more in IEEPA duties paid, a free eligibility review from Price Ridge takes one business day. Reach the team at refunds@priceridge.com.

Frequently Asked Questions

Did the Supreme Court rule on IEEPA?

Yes. On February 20, 2026, the Supreme Court issued a 6-3 ruling in Learning Resources, Inc. v. Trump holding that IEEPA does not authorize the President to impose tariffs. The Court cited the Constitution's assignment of taxing power to Congress and applied the Major Questions Doctrine to reject the claimed authority.

What happened to the IEEPA tariffs after the ruling?

President Trump signed EO 14389 on February 20, 2026, terminating all listed IEEPA-based tariff actions. CBP ceased collecting IEEPA duties effective February 24, 2026. The case was remanded to lower courts to determine the refund process for duties already paid.

How many times had IEEPA been used to impose tariffs before this?

Never. The Congressional Research Service confirms that no President prior to Trump had invoked IEEPA to impose tariffs in its roughly 50-year history since 1977 enactment. The Supreme Court treated this historical absence as meaningful evidence that Congress did not intend to grant such power.

Are all IEEPA tariffs permanently gone?

All IEEPA-based tariffs from the Trump administration have been terminated. However, Section 232 and Section 301 tariffs remain fully in effect, and the administration has already imposed new actions under Sections 122 and 301 since the ruling.

How do importers get refunds for IEEPA tariffs already paid?

For finally liquidated entries, file a protest with CBP within 180 days of liquidation. For unliquidated entries, file a Post-Summary Correction. In both cases, filing a CAPE Declaration through CBP's ACE Portal secures your place in the refund queue — your customs broker can supply the entry documentation you'll need.

What tariff authorities can the President still use?

Section 232 (national security), Section 301 (unfair trade practices), and Section 122 (balance-of-payments, limited to 150 days) are all unaffected by the Learning Resources ruling. The administration has already announced new actions under Sections 122 and 301 since the Court's decision.