Duty drawback has existed in U.S. law since the First Congress in 1789. Despite that history, many importers assume the process is too complex to pursue, or simply don't know it exists. The result: refunds that belong to them go uncollected.

This guide explains exactly how duty drawback works — what triggers eligibility, how claims are filed, what mistakes to avoid, and where IEEPA tariff refunds fit into a separate but related recovery pathway.

Key Takeaways

- Duty drawback refunds up to 99% of duties paid on imported goods that are later exported or destroyed.

- Three types apply to most importers: unused merchandise, manufacturing, and rejected merchandise drawback.

- Claims must be filed within **5 years of the original import date** — missing that deadline forfeits the refund.

- Import entry summaries, export records, and proof of duty payment must all reconcile — missing documents kill the claim.

- IEEPA tariff refunds follow a separate pathway — the CBP CAPE Declaration system — not standard drawback.

What Is Duty Drawback?

Duty drawback is a federal refund program authorized under 19 U.S.C. § 1313 that allows importers, exporters, and manufacturers to recover up to 99% of duties, taxes, and certain fees paid on imported goods — when those goods are subsequently exported from or destroyed within the United States.

Goods that never permanently enter U.S. commerce shouldn't be taxed as if they did. Duty drawback corrects that by returning duties on goods that ultimately leave the country — but it isn't automatic. It's not a challenge to the duty rate, not a credit issued at import, and not a loophole. Recovering it requires active filing, documented proof, and CBP approval.

Understanding who qualifies — and which claim type applies — determines whether a refund is recoverable at all.

Who Can File

Any of the following parties can file a drawback claim, but only one party can claim a given refund:

- The importer of record

- The exporter

- The manufacturer of an exported product that used imported inputs

- A licensed customs broker or authorized agent acting on behalf of any of the above

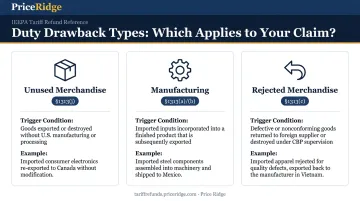

The Three Main Types of Duty Drawback

| Type | Statute | When It Applies |

|---|---|---|

| Unused Merchandise | 19 U.S.C. § 1313(j) | Imported goods exported or destroyed without being manufactured or produced in the U.S. |

| Manufacturing | 19 U.S.C. § 1313(a)/(b) | Imported materials incorporated into a new article that is then exported |

| Rejected Merchandise | 19 U.S.C. § 1313(c) | Defective, nonconforming, or unsuitable goods returned to the supplier or destroyed under CBP supervision |

Unused merchandise example: A retailer imports 10,000 units of a product, sells 7,000 domestically, and re-exports the remaining 3,000 unsold. The duties paid on those 3,000 units are recoverable.

Manufacturing example: A factory imports steel, fabricates it into machinery, and exports the finished equipment. The duties paid on the imported steel component are recoverable.

Rejected merchandise example: An importer receives a shipment that doesn't match the contracted specifications. The goods are returned to the foreign supplier — duties paid on that shipment are eligible for drawback.

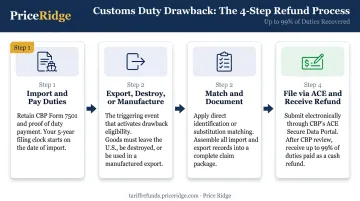

How Does Duty Drawback Work?

Drawback operates as a defined sequence of stages. A breakdown at any stage — missing documentation, missed deadlines, incorrect matching — can result in a rejected claim or zero refund.

Step 1: Import and Pay Duties

The drawback clock starts at importation. When goods enter the U.S. and duties are paid, that event creates the foundation for a future claim. The importer must retain the import entry summary (CBP Form 7501) and proof of duty payment from that point forward.

The 5-year rule is critical: Both the qualifying export or destruction AND the complete drawback claim must occur within 5 years of the original import date. Missing this deadline forfeits the refund with no exceptions for most claim types.

Step 2: Export, Destroy, or Manufacture for Export

The triggering event is the goods leaving U.S. commerce:

- Export to a foreign buyer

- Destruction under CBP supervision

- Incorporation into a manufactured product that is then exported

For unused and rejected merchandise, the goods must not have undergone operations amounting to manufacture or production in the U.S. Certain claim types also require advance notice to CBP via Form 7553 — generally at least 5 working days before export, or 7 working days before destruction.

Step 3: Match Exports to Imports and Gather Documentation

CBP allows two identification methods:

| Method | How It Works |

|---|---|

| Direct Identification | Traces the exact imported item to the exported or destroyed item using serial numbers, lot numbers, or batch codes. Best when inventory systems can track individual units. |

| Substitution Matching | Links exported goods to imports sharing the same 8-digit HTSUS subheading, subject to Part 190 restrictions. The 8-digit HTS match is the central test under modernized drawback rules — not commercial interchangeability. |

Once the matching method is established, you'll need to assemble documentation supporting every link in the chain. Core documents required:

- Import entry summaries (CBP Form 7501)

- Proof of duties paid

- Export bills of lading or air waybills

- Commercial invoices showing goods left the U.S.

- For manufacturing claims: production records or a certificate of manufacture linking imported inputs to the exported product

Step 4: File Your Claim and Receive Your Refund

All drawback claims must be filed electronically through CBP's Automated Commercial Environment (ACE) — paper filings have not been accepted since February 24, 2019.

Claims can be filed directly, through a licensed customs broker, or via a service bureau. After filing, CBP reviews the claim and may request additional documentation. Upon approval, CBP issues a refund of up to 99% of eligible duties.

Processing timelines vary significantly:

- Importers with Accelerated Payment (AP) privileges generally receive refunds within 21 days of ACE acceptance

- Full desk reviews can take more than three years

All records must be retained for three years after liquidation.

What Duties and Fees Qualify for Drawback?

Not every import charge is automatically eligible. Here's the breakdown:

| Duty/Fee Type | Eligible for Drawback? |

|---|---|

| Standard customs duties | ✅ Yes |

| Section 301 tariffs (China goods) | ✅ Yes |

| Section 201 safeguard duties | ✅ Yes |

| Merchandise Processing Fee (MPF) | ✅ Yes |

| Harbor Maintenance Fee (HMF) | ✅ Yes |

| Antidumping duties (AD) | ❌ No |

| Countervailing duties (CVD) | ❌ No |

| Section 232 steel/aluminum duties | ❌ No |

Per CBP's Drawback FAQs, AD/CVD duties are excluded under 19 U.S.C. § 1313(l), and Section 232 steel and aluminum duties are also ineligible. CBP guidance on exclusions does shift, so confirm current eligibility before filing a claim.

A Separate Pathway: IEEPA Tariff Refunds

Importers who paid IEEPA tariffs in 2025–2026 have a distinct recovery pathway that operates entirely outside the standard drawback system.

Following federal court rulings invalidating the use of IEEPA to impose broad import tariffs (including Learning Resources, Inc. v. Trump), CBP established the CAPE Declaration process to administer full refunds of those duties. Unlike drawback, IEEPA refunds don't require export or destruction — every dollar paid under a qualifying IEEPA executive order is refundable regardless of what happened to the goods.

Verify current court and CBP guidance before filing, as the legal landscape around IEEPA tariff refunds continues to develop.

IEEPA duties typically appear under HTS subheading 9903.01.25 on CF7501 entry summaries. For importers without in-house customs expertise, Price Ridge manages IEEPA refund claims from eligibility review through CBP filing and disbursement. The service runs on a contingency basis, meaning no upfront cost until CBP disburses the refund.

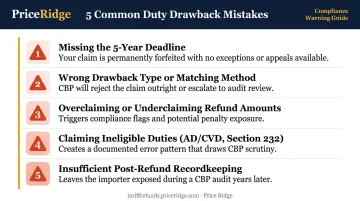

Common Mistakes When Filing a Duty Drawback Claim

CBP's own compliance reminders identify recurring problems that cause claims to be rejected, delayed, or reduced. Avoid these:

1. Missing the 5-year deadline or filing incomplete documentation The most common rejection cause is mismatched records — import entry numbers, HTS codes, or export documents that don't reconcile. CBP will not reconcile gaps for you; unlinked records mean denied claims.

2. Selecting the wrong drawback type or matching method Applying for manufacturing drawback when unused merchandise drawback is more appropriate (or vice versa) routinely draws CBP rejections. Attempting substitution matching without meeting the 8-digit HTS standard creates audit risk.

3. Overclaiming or underclaiming refund amounts Manufacturing claims require precise apportionment — only the duty attributable to the exported portion of production is recoverable. Errors in either direction create compliance issues. CBP compliance reviews have flagged two recurring errors: claiming amounts already refunded by another agency, and failing to reduce claims when later refunds were received.

4. Claiming ineligible duty types Attempting to recover AD/CVD or Section 232 duties through standard drawback is a documented error pattern. Separate the duty components of each entry before calculating your refund potential.

5. Insufficient recordkeeping after the refund Records must be retained for three years after liquidation — not three years after payment. Missing this distinction leaves you exposed if CBP audits a previously liquidated claim.

Frequently Asked Questions

What is duty drawback in simple words?

Duty drawback is a U.S. government refund program that returns up to 99% of the import duties a company paid on goods that are later exported or destroyed, rather than sold in the U.S. market. It is a statutory recovery tool that requires active filing and proper documentation to claim.

What qualifies for duty drawback?

Goods qualify when they are exported, destroyed under CBP supervision, or incorporated into a manufactured product that is then exported. Standard customs duties, Section 301 tariffs, MPF, and HMF are all eligible for drawback. AD/CVD duties and Section 232 steel/aluminum duties are excluded.

What is an example of a duty drawback?

A U.S. electronics company imports components, pays duties, assembles them into finished devices, and exports those devices abroad. The company can then file a manufacturing drawback claim to recover the duties paid on the imported components used in those exported products.

What are common duty drawback mistakes?

The top errors include:

- Missing the 5-year filing window

- Submitting mismatched or incomplete import-export documentation

- Selecting the wrong drawback type

- Claiming ineligible duties like AD/CVD or Section 232

- Failing to maintain audit-ready records for three years after liquidation

How long does it take to receive a duty drawback refund?

Importers with Accelerated Payment privileges generally receive refunds within 21 days of ACE acceptance. Full desk reviews can exceed three years.

Can I claim duty drawback on Section 301 tariffs?

Yes. Section 301 duties are generally eligible for duty drawback when the qualifying goods are exported or destroyed. This makes drawback a viable cost recovery strategy for companies that paid significant Section 301 tariffs on China-origin imports. Note that IEEPA tariffs follow a separate, non-drawback refund pathway through CBP's CAPE system.